Private markets: Fortune favours the agile

In this blog post, we introduce key characteristics of private markets and discuss how pension schemes can incorporate them into their investment strategy.

Private markets are here to stay

Private markets, a catch-all term for investments that aren’t traded on a public exchange or market, have been used by sophisticated investors for decades. However, for many years they were considered much too niche for smaller pension schemes, given that they seemed opaque and required specialist knowledge before even attempting to conduct due diligence.

In the last decade, increased regulation meant that banks turned their balance sheets upside down and became much less willing to lend. For many companies, private markets became a means of raising capital that they may no longer otherwise be able to obtain. Looking at it from the other side, private markets provide an opportunity for investors to meet this demand, whilst increasing diversification in their portfolios through access to a much wider investment universe.

Typically, pension schemes are well placed to do this. Firstly, their lifespan means that all but the most mature schemes can hold assets for many years, which gives them an advantage compared to other investors, such as banks. With support from their adviser or fiduciary manager, they can also overcome some of the governance constraints that often block investment in private markets such as undertaking robust due diligence, ensuring the correct legal documentation is in place, and dealing with cashflows that frequently come and go.

In Australia and North America, superannuation funds and workplace pension schemes now typically allocate upwards of 30% of their assets to illiquid strategies1, with allocations growing in the UK as well.

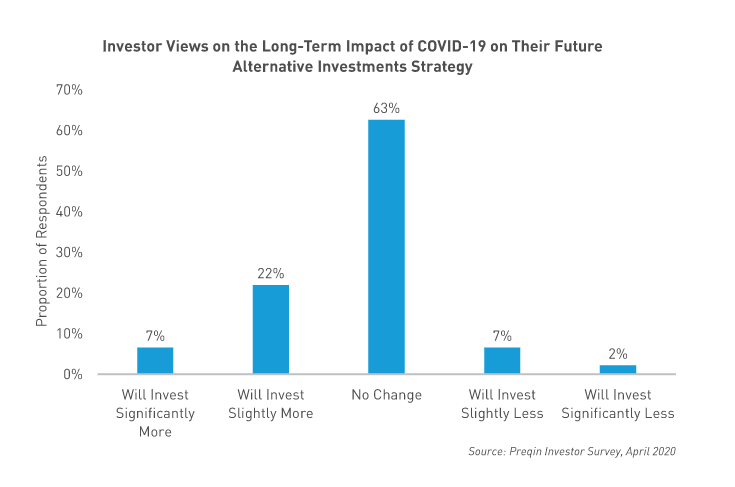

In the current climate, this trend is expected to continue. According to a recent industry survey2 on how investors are responding to COVID-19, almost a third of investors plan to increase their allocation to more illiquid strategies, with less than 10% suggesting they will invest less.

Whether you require growth or income, private markets can help

In the decade that has passed since the global financial crisis, we have seen the majority of pension schemes focus on growth, trying to plug the deficits that ballooned following years of monetary stimulus, and the fall in yields that came with this.

In search of growth

Many schemes retain this focus, searching for a diversified mix of assets that will help them to progress along their journey plan to a point where the assets are either substantial enough to cover all members’ benefits as they fall due, or to transfer to an insurer. For these schemes, a growth-orientated private markets solution can offer the potential for outsized returns (markets tend to be less competitive and less efficient), as well as lower reported volatility relative to listed markets.

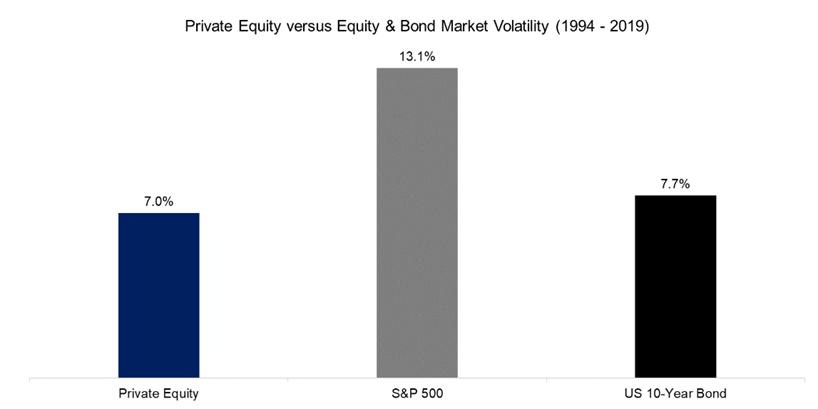

To add some colour here, the chart below shows that between 1994 and 2019, the volatility of the U.S. Private Equity index is almost 50% lower than that of the S&P 500, and, more surprisingly, even below that of the U.S. 10-year government bond.

Source: FactorResearch. Calculations based on quarterly data.

It is worth noting that part of the reason for this is that private equity assets are valued less frequently than publicly traded securities. Anything between these valuation dates is an estimate, and behavioural economics teaches us that these are more often than not anchored to, and then adjusted from what was stated previously. This means that assets can often grow predictably - at least until the point of sale. This has the effect of smoothing the return profile, perhaps artificially, and therefore dampening the volatility.

The ‘true’ volatility remains a debated point by theorists, however, whilst these debates continue, Q1 2020 has again shown us how these strategies can further immunise schemes - and sponsor - against sharp market falls, and sudden reductions in scheme asset values that come alongside these.

For those who care more about income

For other schemes which are more mature, or have had more interest rate protection in place in recent years, seeking outsized returns is now less of a focus. They are turning their attention to reducing the one risk that has not yet been solved for: the risk of having to sell assets at depressed prices in order to cover members’ benefit payments as they fall due, or, more critically, being unable to sell them at all.

A private markets solution can again help. Certain private asset classes can provide stable income streams, spitting out more cash than their liquid counterparts without resorting to borrowing, and are well placed to form a core part of a, long-term, low-risk investment portfolio. Such a solution can also keep pace with inflation to help match inflation-linked liabilities, and provide an attractive return on top of this, to help cover scheme running costs and manage pesky unexpected or non-investment risks, for example arising from covenant strength or longevity changes.

There is no time like the present, but choose wisely

If the above tells us one thing, it is that private markets contain a broad spectrum of strategies doing very different things. As you might have expected, the relative attractiveness of each of these asset classes does vary through time. However, in both growth and income-orientated solutions, history has shown us that after a period of market disruption, opportunities tend to be more attractive when compared to both prior years and to publicly listed peers.

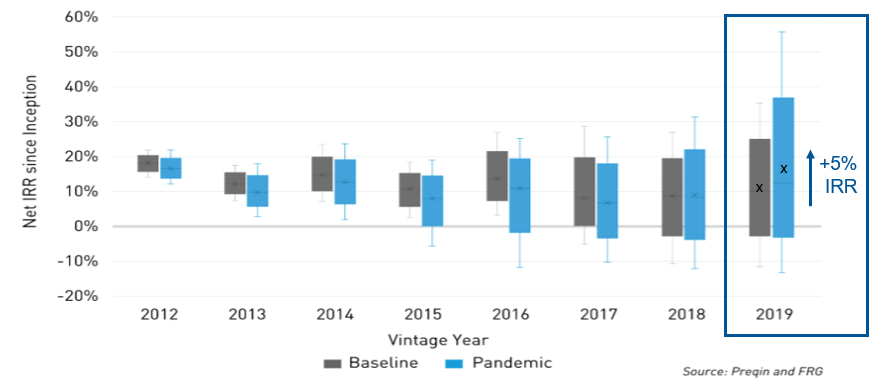

History has also shown us that periods of market disruption can cause the spread of returns - long a defining feature of private equity - to increase. As shown below, the recent market conditions have led private markets specialist Preqin, to increase their return expectations by 5% for funds launched in 2019, as well as raise the expected dispersion amongst these funds to levels certainly not seen in the last decade.

This research helps to reinforce the benefits that a multi-manager solution, along with proactive and continuous manager research, can bring. For schemes that are able to access this, we expect that with the right exposures an investment can be put to good work and, as a result, 2019-2022 vintage funds are likely to stand out as top performers.

Now is not the time to delay.

Up next in series, we will delve into what investors should look for in both growth, and income-based private markets solutions.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.

1 Source: PPI

2 Source: Preqin Investor Survey, April 2020