Russell Investments 2024 Private Markets Survey: Where do managers see opportunities today?

Executive summary:

- The survey shows that private markets managers see attractive opportunities in several industries, sectors, and assets, including decarbonisation, real estate and infrastructure. In particular, some see European private real estate as an especially compelling opportunity.

- An overwhelming majority of managers surveyed believe there will be an increased demand for impact strategies.

- The results indicate that the democratisation of private markets continues, with increased demand from financial advisors and their clients.

Introduction

Private markets continue to become an even more prevalent component of investor portfolios, providing access to an expanded opportunity set and strong diversification beyond traditional stocks and bonds. We expect this trend will continue as investors seek to find new sources of return and portfolio protection in a challenging market environment.

Given the dynamic nature of the unlisted market, we recently surveyed private markets managers to help provide a clear lens through which to view the changing nature of this growing and increasingly important investment landscape.

In this survey, we focused the questions on the following five perspectives:

- Key investment strategies

- Opportunities and risks

- Value creation

- Impact investing

- Investors and products

We wish to thank the many private markets investment professionals who contributed their time, effort, and insights by responding to the survey. It is our distinct relationship with underlying managers that earns us this unique access to insights and analysis, which we trust proves valuable to your organisation as you continue to develop your private market programs moving forward.

Methodology

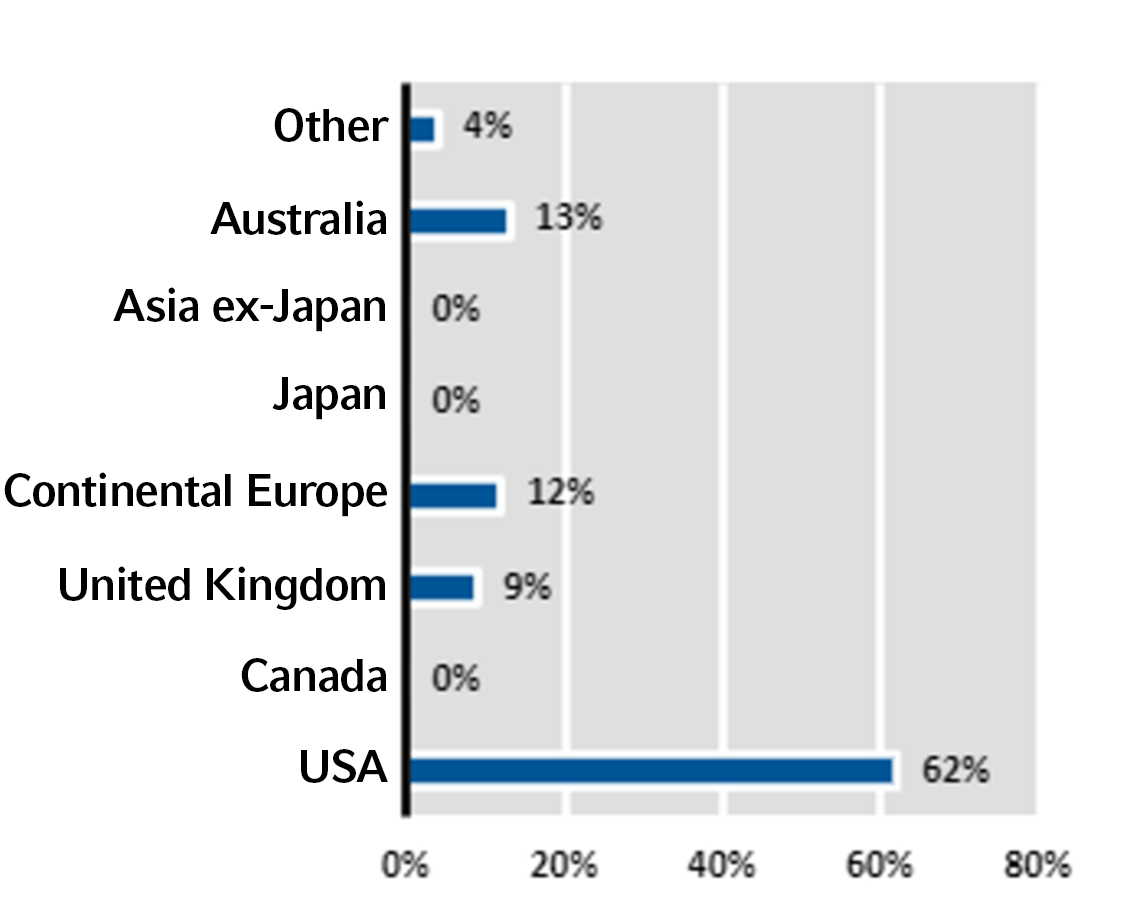

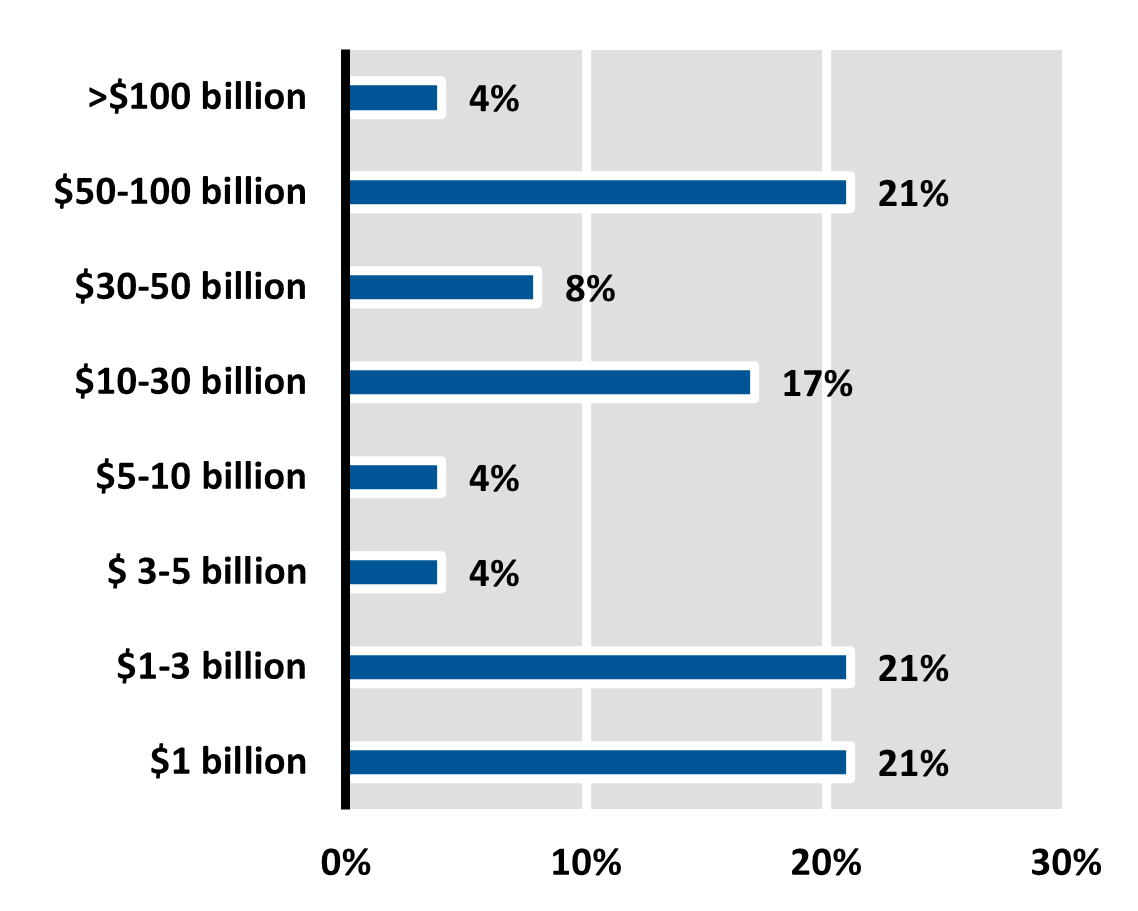

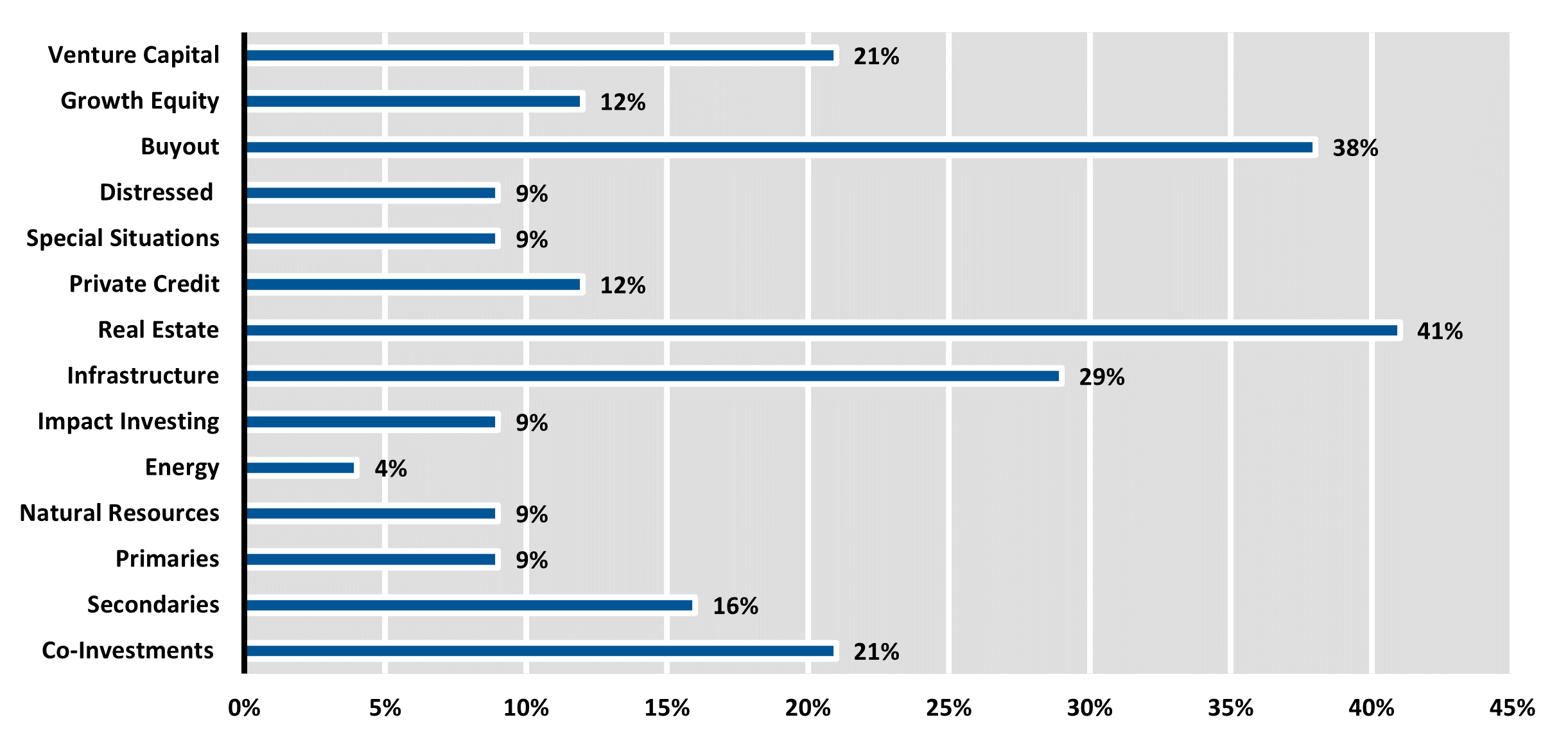

In late 2023, firms representing US$ 1.4 trillion in total assets completed an online survey covering the broad universe of private markets strategies. Tables 1 to 3 provide a breakdown of respondents by domicile, private markets AUM, and private markets strategies offered.

Chart 1: In which country or region is your firm domiciled?

Chart 2: What is your firm’s total AUM in private markets?

Chart 3: Which private markets strategies does your firm offer?

Survey details

1. Key investment themes

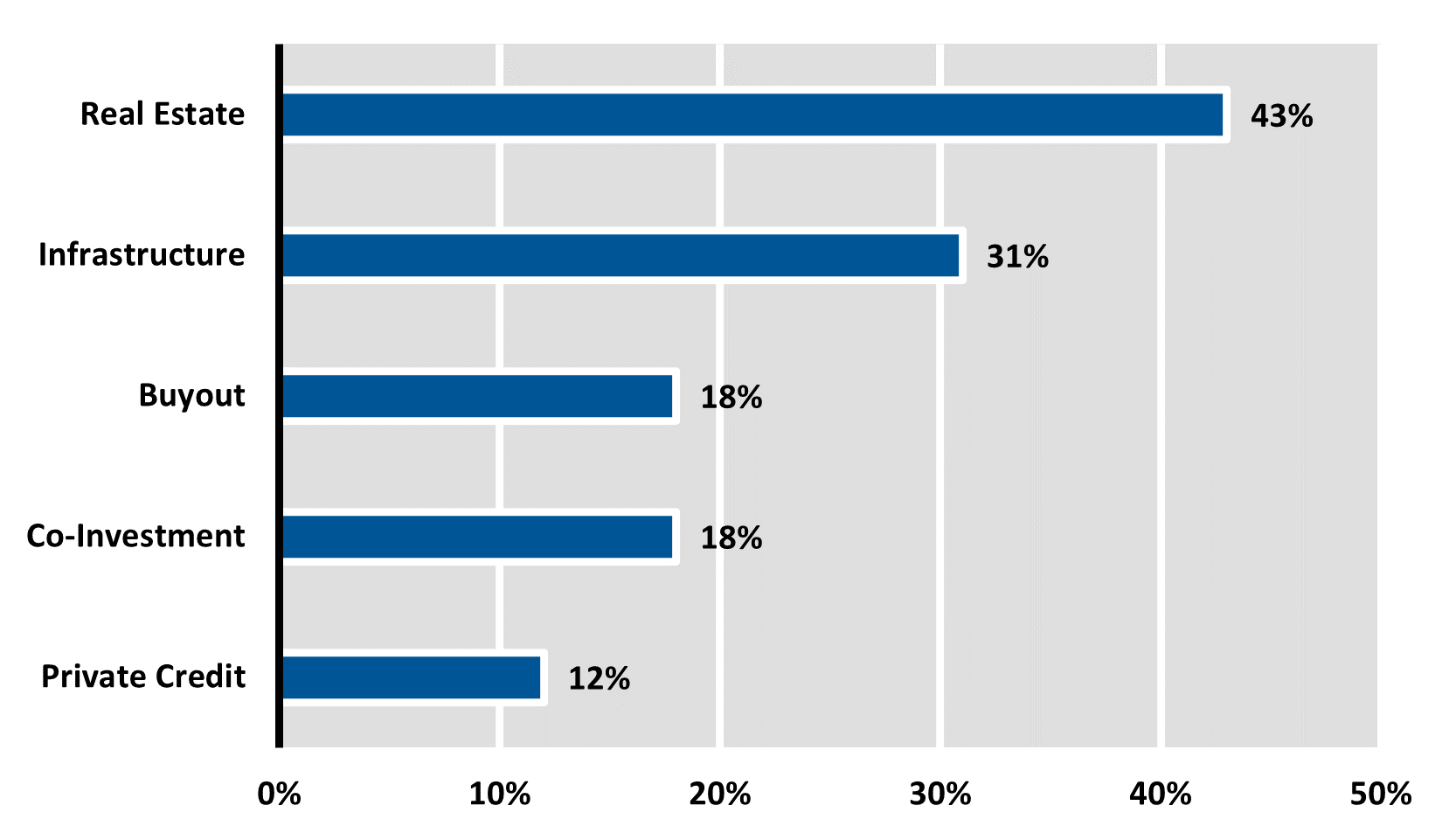

Similar to last year's survey, we wanted to understand the key investment strategies that private markets managers expect to play out over the short term and long term. The top five strategies respondents highlighted were:

Chart 4: Top five strategies respondents highlighted

2. Opportunities and risks

As investors look to build and maintain their desired strategic targets in private markets, they are also focused on exploiting some of the most compelling investment opportunities, while prudently navigating risk. As such, we sought to understand how private markets managers view the opportunities and risks in their day-to-day investment activities, and how this impacts their investment decision-making.

OPPORTUNITIES

Similar to last year’s survey, the responses show that managers are focusing on industries, sectors, and assets that are expected to survive and prosper in the future, including those that are supported by long-term secular trends, such as reshoring of supply chains, decarbonisation, and increased digitisation.

While the market outlook remains uncertain, managers were of the view there are attractive opportunities to be found across the spectrum of private markets, such as:

- Equity-focused investors searching for value are finding attractive investments in the secondaries space, as overallocated limited partners pursue portfolio sales at buyer-friendly prices.

- In the privately originated credit markets, a combination of shorter duration and floating rate structure is providing an attractive means of mitigating interest rate risk.

- The inflation-linked nature of real estate and infrastructure offering either explicit or implicit protection from inflation – i.e., contracted / regulated revenues and replacement cost.

- In relation to the decarbonisation theme, the clean energy transition is creating significant demand for a large number of base metals.

- The reduced availability of debt and equity capital has created market inefficiencies and may result in assets trading at more attractive valuations, despite solid fundamentals.

Real estate was an area that stood out in terms of the change in tone around prospects that lie ahead, given the decline in valuations over the last 12 months. While there are notable differences in the fundamentals across different property types and markets, the asset class stands poised for a turnaround in the years ahead. One element contributing to the positive sentiment is the outlook for supply, given that construction starts have dropped 67% from their 2022 peak. When looking at the demand side of the equation, fundamentals also look attractive. This is borne out across a range of sectors including demographics driving the demand for senior housing and single-family rentals, industrials being supported by e-commerce and re-shoring of supply chains, and AI / digitisation driving growth in data centers.

In addition, it was highlighted that Europe currently presents an outstanding opportunity in real estate as the market has experienced a large correction (even deeper than what has transpired in the U.S. and UK), which is producing significant deal flow at compelling pricing. Following this dislocation, companies that have suboptimal or broken capital structures have started to sell assets at deep discounts.

RISKS

In the current inflationary environment, a key risk highlighted was that companies have encountered rising costs, putting pressure on working capital budgets. In addition, geopolitical uncertainty was also top of mind for survey respondents, given the risk that should these tensions escalate, the potential for increased energy and agricultural prices could prolong the inflationary environment.

With respect to real estate specifically, there were concerns about the extent to which some investors have not written down the value of certain assets, hence the potential for negative returns remains. Also, distress in the commercial real estate debt markets continues, as evidenced by various indicators such as delinquency rates and special servicing. While predominantly driven by the office sector, distress seems likely over the medium term as assets with longer-term leases roll over.

Other risks noted include:

- Rising interest rates

- Recession fears

- Debt sustainability and liquidity issues

Considering these risks, managers are focusing on (1) working with experienced, operationally focused deal sponsors, (2) mitigating risk through thoughtful portfolio construction that provides investors with an appropriate level of diversification, (3) given interest rate risk, assuming today’s rates in their underwriting and not betting on interest rate declines, (4) buying assets supported by long-term secular trends, and (5) investing in companies / assets that are defensively oriented, provide essential services, enjoy inflation-linked cash-flows and are well managed and governed.

3. Value creation

One of the key benefits of private investment is that general partners (GPs) have a much stronger direct involvement in creating portfolio company value over the medium to long term. GPs can draw on an additional level of tools to support portfolio businesses with direct engagement in personnel and business strategy. As such, we wanted to glean insights into the actions being taken by private markets managers to determine how they are seeking to create value in the current market environment.

At a high level, the focus is on active management and operational excellence, including leveraging operating partners' expertise and the execution of business plans in the face of macroeconomic uncertainty, margin pressures, and heightened borrowing costs.

At the individual portfolio company / asset level, examples of the top initiatives that GPs and management teams are focused on to create value for investors are highlighted below:

REAL ESTATE

- Plugging holes in capital structures for developments with strong underlying real estate.

- New real estate developments where the underwriting works based on today’s interest rates.

- Finding off-market real estate opportunities that can add value prior to closing.

- Bottoms-up, asset-level approach to find optimal entry point in the capital structure.

- Prudent use of leverage where investment decisions are driven by unlevered returns.

- De-risking transactions by negotiating leases and lease extensions with tenants prior to risking equity capital.

- Renovating, repositioning, and rebranding

INFRASTRUCTURE

- Ensuring projects are completed on time and on budget.

- Implementing and monitoring sustainability initiatives.

- Add-on acquisitions to expand platform businesses.

PRIVATE EQUITY

- Margin expansion through cost savings and optimising operations.

- Improving the go-to-market strategy and driving operational efficiency.

- Product expansion, either organically or via M&A.

- Sales excellence programs.

- Capturing opportunities to harness technology for growth.

PRIVATE CREDIT

- Ensuring capital structure resilience.

- Providing portfolio companies with access to cost reduction, revenue generation, and knowledge-sharing opportunities.

- Serving as lead lender / originator to extract larger upfront fees and exert greater control throughout the life of the loan.

- Focusing on loans to strong management teams with significant equity ownership.

4. Impact investing

Given that private markets managers have deep involvement in portfolio company strategy, management, and day-to-day operations, they are uniquely positioned to influence and drive outcomes associated with impact investing. Also, with a heightened global focus on sustainability across society, governments, and investors, it is not surprising that 88% of respondents saw an increasing demand for impact strategies. In addition, 40% of survey respondents indicated they are planning to launch impact strategies in the 12 months ahead.

We also asked participants which three United Nations Sustainable Development Goals (SDGs) private asset firms could make the biggest difference on when it comes to impact investing.

The top five SDGs that managers felt private assets could contribute to were:

5. Investors and products

Given the increased demand for private markets exposure from investors, there are several key trends that are shaping the landscape for private markets product development.

One of those is the continued democratisation of private markets. While still in its infancy, there is increased demand from financial advisors and their clients who are seeking out the benefits of private markets that institutional investors have enjoyed for decades. These include diversification, volatility dampening, inflation protection, and income generation. This is borne out in the percentage of survey respondents’ total assets that are sourced from institutional and retail / high-net-worth investors, respectively.

As a percentage of managers’ total assets, institutional investors accounted for 85% of assets while retail accounted for 15%. Relative to last year’s survey we have seen a 5% increase in assets sourced from the retail channel. In addition, 83% of managers noted they are actively looking to raise more capital from individual investors and 90% of respondents highlighted their plans to expand their offerings to this cohort in the next 12-24 months.

Fund structures also continue to evolve. While closed-end funds remain the primary type of fund structure, evergreen vehicles continue to see investor demand. This is reflected in the 27% of respondents who are planning on bringing evergreen funds to market, given a desire by managers to broaden their product offerings and refine structures to meet the needs of investors.

Summary

The Russell Investments 2024 Private Markets Survey has provided valuable perspectives on the key trends, risks, and opportunities across the private markets investing landscape.

Across the spectrum of private markets, we believe that managers and investors are well-positioned in 2024 and beyond to exploit opportunities across real estate, infrastructure, private equity, and private credit. By working hand-in-hand with engaged and incentivised management teams, GPs are poised to create value for their investors through actively managing businesses and assets, which in turn should serve investors well in an economic environment that is facing a range of risks including geopolitical uncertainty, inflation, and recession fears. Also, we see continued product innovation by GPs, combined with robust demand from retail investors, driving the adoption of private market investments across individual investor portfolios.

As Russell Investments continues its commitment to help our clients achieve their desired investment outcomes, we encourage readers to discuss with us any questions or comments they may have about the survey.

Download the surveyAny opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.