RPI Consultation - The mist clears

In February, we wrote a blog article about the consultation between Her Majesty’s Treasury and the UK Statistics Authority (UKSA), a link to that article can be found here. We provided an overview of what inflation is, why it matters and why the UK government was proposing to change the UK’s standard inflation measure from the Retail Price Index (RPI) to the Consumer Price Index including Housing Costs (CPIH) from 2030.

What does this consultation mean for pension schemes? Many schemes increase some or all of their annual pension payments in-line with inflation, this is to ensure that the members retain their purchasing power through time. After all, a pound was able to buy a lot more 10 years ago than it does today and it’s not uncommon for people to enjoy 20-30 years in retirement. The measure of inflation used by each scheme will depend on its individual trust deed and rules. These increases could be based on RPI, CPI, or may even specify that the increases should be based on the generally accepted measure of inflation. Historically this generally accepted measure of inflation has been RPI. As a result, any change to RPI, or the generally accepted measure of inflation will have an impact on these future pension increases and, by extension, the pension payments members receive.

Trustees of defined benefit pension schemes typically meet these future payments by having a portfolio of assets. These investment portfolios are often invested in a wide range of asset classes ranging from government bonds through to private equity and everything in between. UK government bonds are perceived as low risk, their steady stream of payments make them an attractive investment for pension scheme trustees who have to make regular pension payments. Where a scheme has some or all of its benefits linked to inflation, UK government bonds that have payments linked to inflation (referred to as index-linked gilts) have been in high demand. Historically these index-linked gilts have used RPI as the inflation measure when increasing the promised stream of payments.

Our previous blog article noted that there are differences between how RPI and CPI are calculated. Due to these different calculation methodologies, CPI has historically been about 1% p.a. lower than RPI. Changing RPI to CPI or CPIH would not only result in members receiving smaller annual increases going forward, but trustees also finding that the future payments they receive on the index-linked gilts they hold reducing.

Consultation

Prior to the announcement on Wednesday 25 November the Chancellor and the UKSA launched a joint consultation on the 11 March. The consultation noted that from 2030 onwards the UKSA would have the discretion to move the UK’s standard inflation measure to CPIH. The consultation had previously asked for views on bringing forward the date on which this change takes place to sometime between 2025 and 2030. Furthermore, they asked for views to be provided on the technical approach used to align RPI with CPIH. As part of their responses many holders of index-linked gilts requested that some form of compensation be provided to reflect the reduction in the future expected stream of payments.

When it comes to markets, it’s often not what will happens that matters but if the market has accurately priced in what is expected to happen.

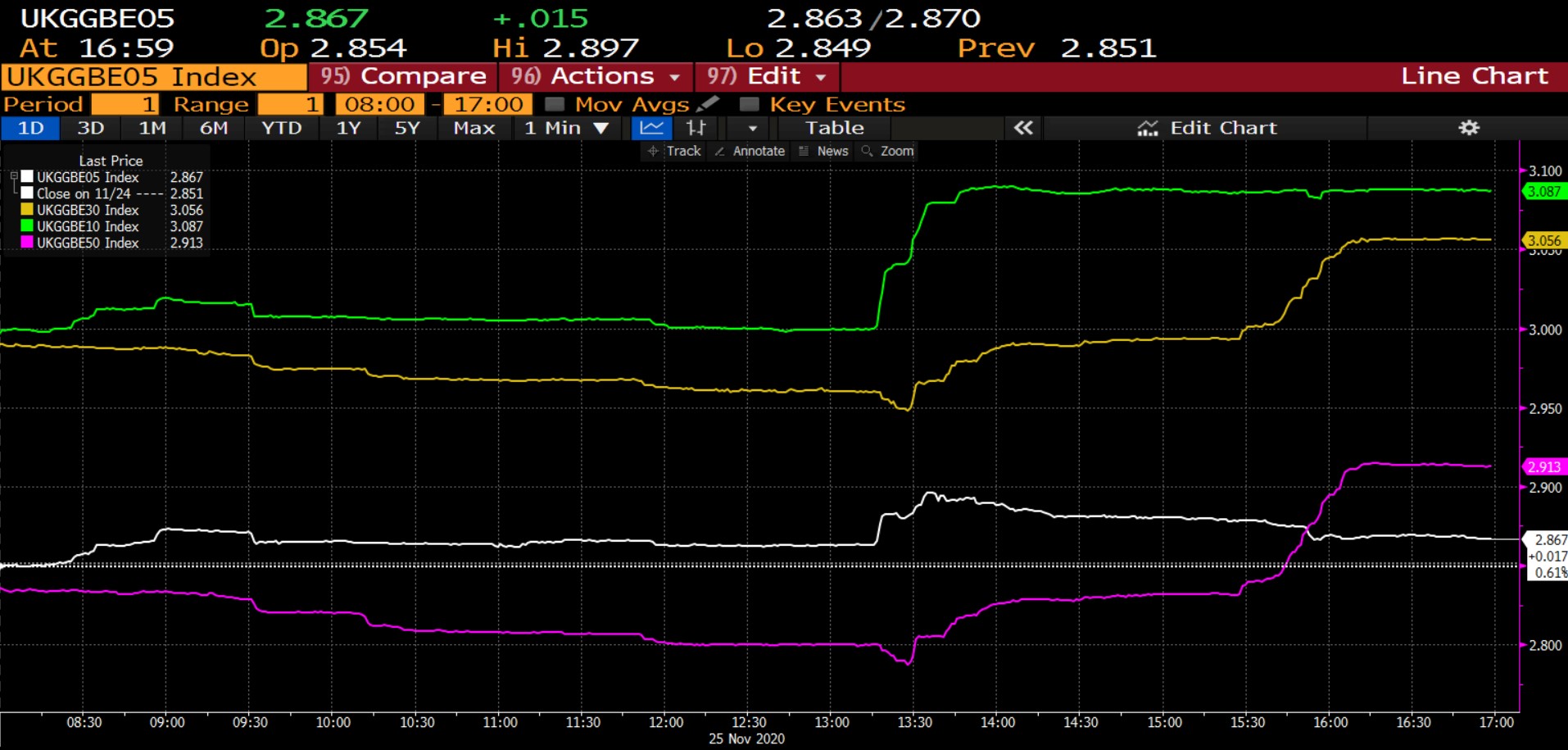

Today’s announcement confirmed that the Chancellor would not bring forward the date to implement the changes to RPI before the previously proposed implementation date in 2030. The consultation also noted that no compensation would be paid to the holders of index-linked gilts. In the chart below we show how the future implied inflation suggested by UK government bonds changed during the day for the next 5 years (white line), 10 years (green line), 30 years (yellow line) and 50 years (purple line).1

Future implied UK inflation expectations

Click to enlarge the image

Source: Bloomberg, Russell Investments. 25 November 2020.

The consultation was released early in the afternoon, at which point there was an immediate reaction in the market. Going into the day inflation expectations were steadily falling, presumably this was the market pricing in that the changes to RPI calculation methodology might actually be made prior to the 2030 date previously set out. However, with the consultation confirming that the RPI calculation methodology would be aligned with CPIH from 2030 onwards (i.e. not brought forward to a date between 2025 and 2030) this gave certainty to investors. This led to increased demand for index-linked gilts and an increase in future inflation expectations as RPI would be based on the current methodology (which results in higher annual increases) between 2025 and 2030. However, this isn’t the whole story as the above implied inflation curves are driven by supply and demand for the underlying index-linked gilts from which these curves are produced from.

How did the market react?

The announcement also gave greater certainty to investors. A cloud has been hanging over the index-linked gilt market since this consultation was originally released in 2019. Would changes to the inflation measure be made prior to 2030, could the changes be more extreme than previously thought? Today the mist cleared, and clarity and certainty were provided. As a result, investors felt a renewed enthusiasm towards the UK index-linked gilt market and aggressively bought these bonds.

In addition to this, whilst the UK government is expected to issue at least £350bn of government bonds this year, only around 5% of the issuance has been in index-linked gilts. This figure is much lower than the proportion of gilts that have been index-linked historically and the Debt Management Office (DMO) today confirmed that the issuance of index-linked gilts for the rest of 2020 will be extremely sparse. That trend could also continue into 2021 if conventional gilts are viewed as a preferable way to manage the Treasury’s balance sheet. The announcement resulted in investors wanting to increase their allocation to index-linked gilts, conscious that future issuance is expected to remain below historical averages.

The chart below shows the change in value of the 2068 index-linked gilt (yellow line) versus the nearest equivalent conventional gilt (using the 2071 nominal gilt for comparison purposes). Whilst the conventional gilt returned less than 0.8% over the day the index-linked gilt increased in value by just under 5%. That is a meaningful one day move for any asset and particularly for a government bond. Investors have reacted positively to the outcome from the consultation and following a modest early morning sell-off, there was then significant demand for long-dated index-linked bonds once the findings from the consultation had been released.

Click to enlarge the image

Source: Bloomberg, Russell Investments. 25 November 2020.

The outperformance of index-linked gilts versus their nominal counterparts was most pronounced for long-dated index-linked gilts but it was a similar story for all index-linked gilts with maturity dates after 2025.

What does this mean for you?

From 2030, RPI will transition to CPIH. The market had already priced that in prior to the announcement (if it hadn’t, the movements would have been much more pronounced than they were). When trustees are going through their next actuarial valuation their Scheme Actuary will likely need to revisit how they calculate the inflation curves used to calculate future expected benefit payments. In prior actuarial valuations, the difference between nominal and index-linked gilts would provide the future expected RPI inflation curve. From 2030 onwards, the index-linked gilt market has priced in the move to CPIH and scheme actuaries will need to adapt to that when they are calculating the inflation curves required to calculate the future benefits which members are due.

For holders of index-linked gilts, the impact of the consultation also appears to have run its course. Today, it has been confirmed that these assets will provide payments that are indexed to CPIH from 2030 onwards. The government has explicitly confirmed that no compensation will be paid to make good the difference between RPI and CPIH after 2030. As a result, the information is now known, and it is safe to assume that this information has been priced into the gilt market. It is also worth saying that the outcome is also not entirely negative for holders of index-linked gilts. Depending on the maturity of the index-linked gilts held you might have seen your holdings increase in value by between 0.5% and 5%. That is a positive return and needless to say much better than if the implementation date for these changes had been brought forward to somewhere between 2025 and 2030.

For investors monitoring their assets and liability values daily we would suggest speaking to your Scheme Actuary and Fiduciary Manager to help ensure that your scheme’s liability benchmark incorporates today’s announcement and, where necessary, refining liability hedging portfolios accordingly.

Is this the end of the story?

With 10 years left until these changes are due to come into effect, it is difficult to know how the story could develop from here. Due to the complexities of explaining this issue, it appears that, to date, this consultation has largely gone unnoticed by the wider population. If the consultation were to receive widespread news coverage it is not inconceivable that it could become a highly charged topic for future elections. With at least two elections between now and 2030, we cannot rule out that a future government might wish to review today’s findings. That being said, it would seem inevitable that future governments will have to manage a large fiscal deficit. Reversing today’s findings and, by extension, increasing future expected borrowing costs would seem an unlikely course of action to take given the current economic backdrop.

1 The implied future inflation rate is calculated by comparing the yield on conventional fixed interest (nominal) gilts and index-linked gilts.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.