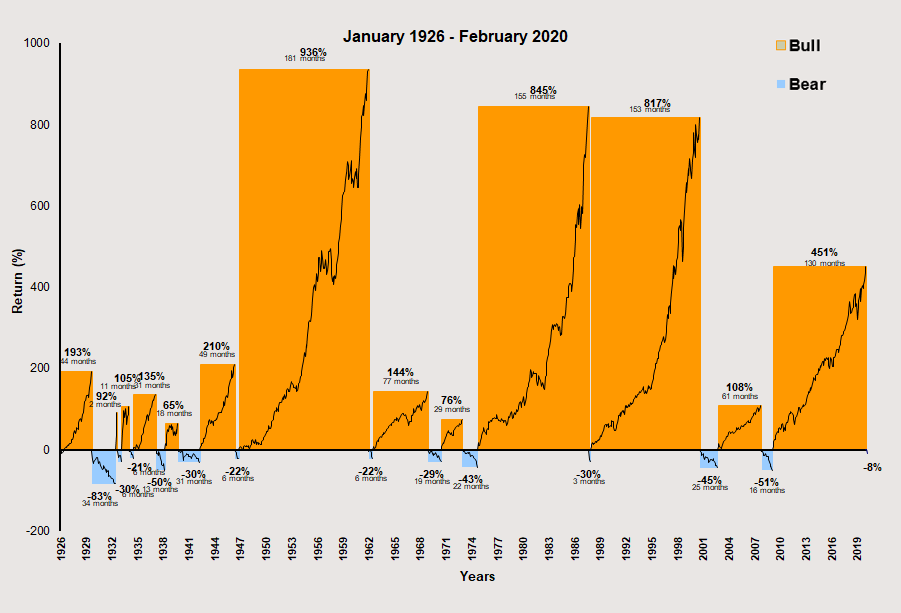

Bulls vs. bears

Editor’s note: This post was originally published on the Russell Investments blog in September 2018. Due to popular demand, we've published an updated version.

Looking back over the last 90-plus years, it is unmistakable that bull markets have, on average, lasted longer than bear markets. In addition, bull markets have historically more than made up for any losses in bear markets. We believe the best approach for long-term investors is to stay invested, and dialed in on their long-term objectives.

Click image to enlarge

Over the past 94 years, as shown in the chart above, we observe 26 bull and bear market cycles, with the average bear market seeing a 36% decline, in contrast to the average bull market increasing by 321%! What’s more, the average bear market has been 15 months in duration while the average bull market has sustained for almost 72 months.

Even after periods of a more considerable downturn, most notably in the 1930s, we see that the market rebounded substantially in the years that followed. So, although exiting the market might feel like the right thing to do when volatility increases and a bear market ensues, history demonstrates this approach typically has not paid off over the long run.

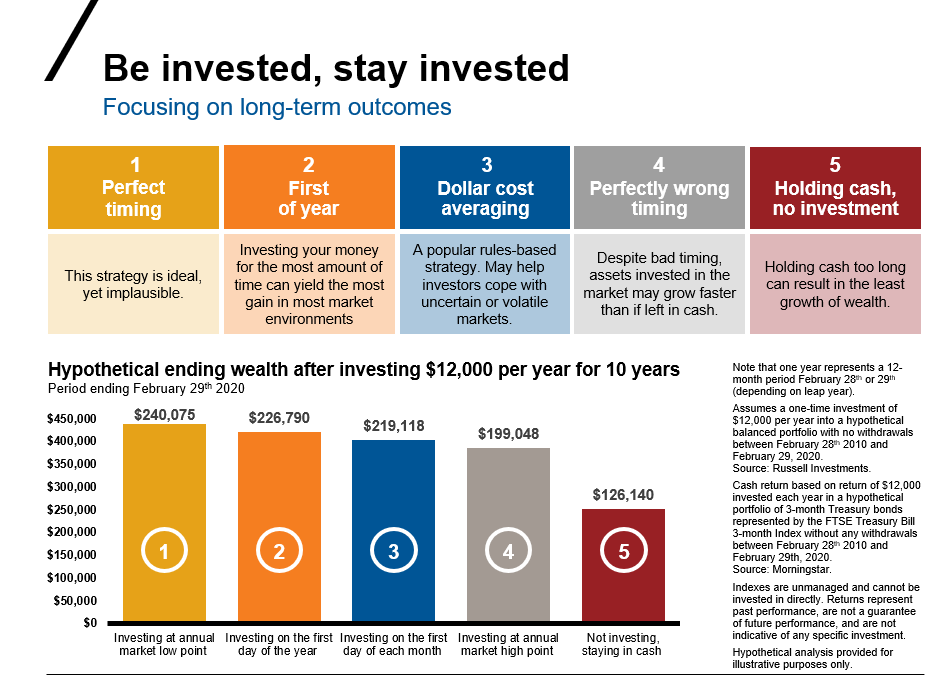

5 hypothetical scenarios reviewed

In the chart below, we lay out five distinct hypothetical accounts, with $12k invested in each account annually over a span of the last 10 years. Short of possessing a magic crystal ball, being invested—and staying invested—would yield the best outcome for the long-term.

- The first scenario, or crystal ball scenario, assumes perfect market timing and invests at each annual market low point. Of course, this is optimal, but pretty much impossible; however, using historical data to calculate this scenario over the past 10 years, an investor would have made $240k with impeccable market timing.

- The second scenario assumes the annual investment is made every year on January 1. It allows for the longest amount of time possible, and would yield the second-best result or next-best strategy of $226k.

- The third strategy, called dollar cost averaging, is based off investing once per month. This strategy is very practical for most investors in the market for several reasons, but the principle reason relates to pay schedules and having cash available to invest. Investing on a monthly basis allows investors to get their money in the market and ride out some of the month-to-month volatility by not putting all their money in the market before a big drop. The difference between strategies two and three is relatively modest, and while the second strategy has been better in nearly all market environments, the third strategy is likely more realistic and easier to implement for most investors because not everyone has large sums of cash to invest at the start of the year.

- The last two scenarios show the negative impact of investing with the absolute worst timing for the last ten years, or of just sitting on the sidelines in cash. While both outcomes would have fallen short of the first three, even the perfectly wrong timing scenario would have yielded a gain of nearly $80k. Unsurprisingly, the holding cash scenario would have resulted in negligible gain.

Click image to enlarge

The bottom line

Time is on your side. By setting long-term objectives and possessing the discipline to stay invested through the ups and downs of the market, we believe a diversified portfolio has the best probability of meeting its goals.