Considering hiring your actuary to be your OCIO? 5 reasons you may want to re-think that approach

Searching for an OCIO provider can be a daunting task.

Many committees are faced with a decision about whether to conduct a broader OCIO search or to shift their asset management function to an already trusted partner, like their actuary. The decision to keep the investment program in safe hands may seem like an easy one. Committees might be under the impression that the actuarial firm is positioned to be a better manager of asset/liability risk—because of their actuary’s knowledge of the plan’s liabilities. They might also feel that having both services under one roof creates economies of scale and increased interaction between the investing team and the actuarial team—because they are housed within a single firm—ultimately delivering a better holistic solution for their pension plan. But we believe pension plan sponsors gain significant value by having the expertise of both an experienced OCIO specialist and a separate actuary focused on their plan fundamentals.

Russell Investments has worked with the actuarial firms representing over 98% of U.S. corporate defined benefit plans throughout our past four decades of providing OCIO services to pension plans.

Here are five reasons we believe you should view your actuary and your OCIO provider differently:

- There’s a difference between how pension plan actuaries and investment actuaries look at your liabilities.

- Interaction between your OCIO provider and your actuary is coordinated and integrated, regardless of whether they are consolidated in one firm or across two organizations.

- An OCIO can provide an objective check on the economics of risk transfer strategies.

- Actuarial firms are focused on—and good at—things other than investment outsourcing.

- OCIO is a specialty practice. It should be your investment partner’s primary focus.

Every pension plan actuary should have the skills and expertise to collect your cash flows, feed those into their asset/liability tools and model the impact of prospective asset allocation decisions on projected funded status. What not all pension actuaries can do is understand the nuanced interactions between your pension liabilities and your entire portfolio. This includes your return-seeking assets, not just your liability-hedging portfolio. For example, many actuaries create liability-hedging assets with a preponderance of credit bonds, ignoring the high correlation between these securities and equities during periods of market stress, like we’ve recently experienced. Investment actuaries—the types of actuaries we hire at Russell Investments—understand this interplay. They can provide a committee with a more robust and more nuanced look at how these two plan components will work together over time.

This leads us to include Treasury bonds in many of our liability-driven investing (LDI) solutions. They are effective at both extending asset duration to more closely match liability duration and providing protection in flight-to-quality environments when equity and corporate bond correlations rise. We believe this gives committees deeper insight and more data to effectively make investment strategy decisions that will affect their funded status over the long-term. It’s especially helpful when committees are looking to model the financial impact to their companies of key decisions, such as closing or freezing a plan. And, we have found over the years that a deep understanding of the interplay of risk between assets and liabilities is more important to the overall success of the plan than simply understanding and knowing the liability side. We’ve found this to be true across the globe and in multiple interest rate environments, including environments with low-to-negative interest rates.

This partnership, whether between internal divisions of the same firm or between an OCIO and an actuarial firm, is key to delivering on your pension plans goals and objectives. The truth is that there’s rarely regular, ongoing interaction between the pension actuaries and the investment professionals, even within the same firm. They are two distinct groups and departments. An annual refresh of basic actuarial data complemented by a triennial deeper dive through asset/liability modeling is usually sufficient to understand your plan liabilities and their sensitivities to market-related factors. A number of our in-house actuaries came from large actuarial firms prior to working for us. They confirm that the actuarial and investment practices operate autonomously most of the time. From their experience, the level of interaction is consistent, regardless of whether the firm is providing data to another division of the same company or an external OCIO like Russell Investments.

Actuarial firms are equipped to support plan sponsors’ risk-transfer initiatives—such as terminated vested lump sum programs or small benefit annuity purchases—or to facilitate plan terminations. When fashioning the business case, a conflict can arise to bias results in favor of these strategies. Why? Because these firms earn significant fees for managing these projects. In several cases, Russell investments’ actuarial team has provided an objective second set of eyes to ensure that all potential alternatives have been robustly evaluated, using realistic assumptions. In several cases, this has resulted in a plan sponsor deciding their best interests were served by electing not to pursue, or to reduce the scope of, a risk-transfer initiative recommended by their actuary.

When we look to hire asset managers for our clients, we look for specialists. And then we combine complementary specialists together to provide our clients with a comprehensive portfolio—one that keeps them appropriately positioned for the current market environment. We would argue that this same approach can be used when deciding whether to hire an actuary or an OCIO specialist to help manage your pension plan. Hire both. Why? Because actuarial firms and OCIO firms are good at different things.

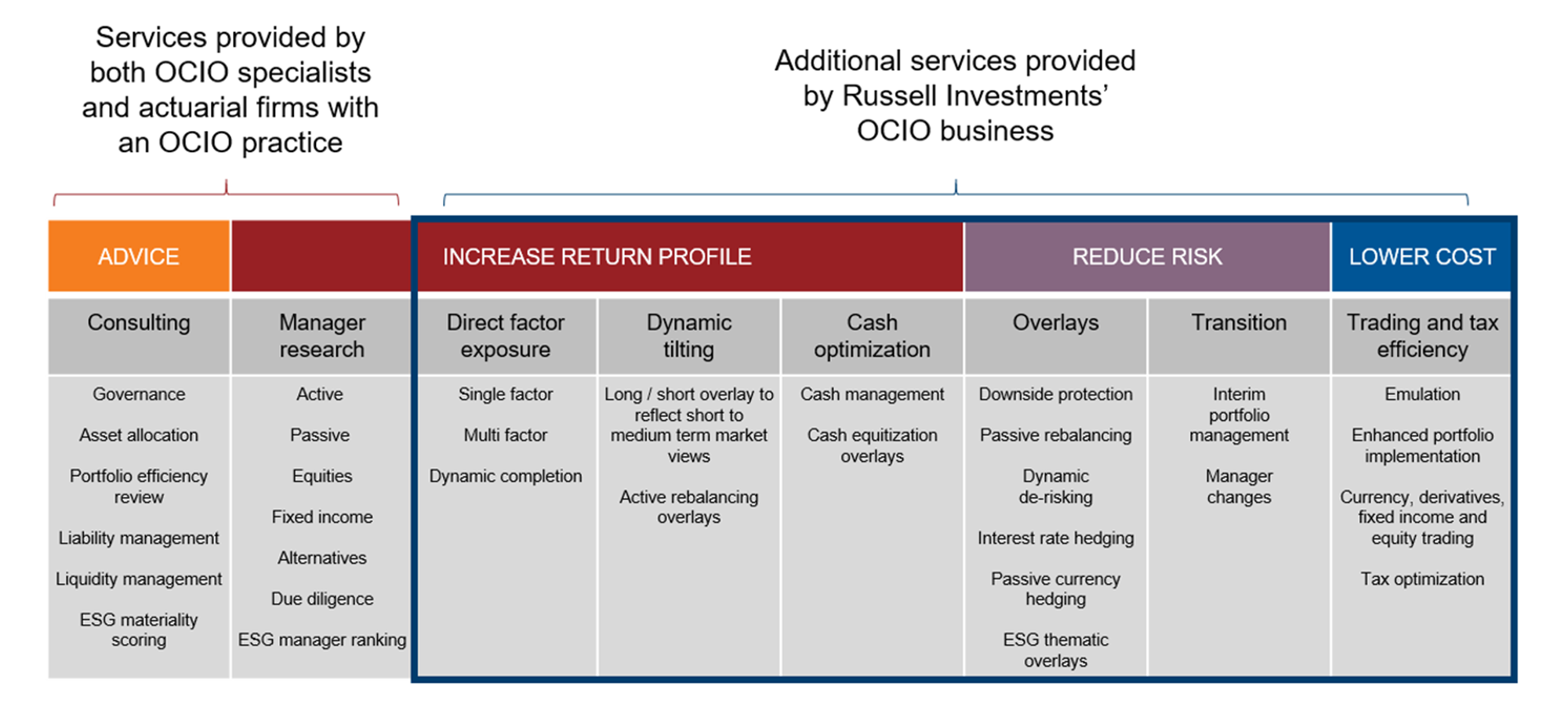

Actuarial firms are focused on the reporting requirements associated with a defined benefit plan. They’re also focused on advising corporate benefits departments on the competitiveness of their total compensation package and on periodic consideration of retirement plan redesign. All of these tasks are important to plan sponsors and are responsible for driving the majority of the actuarial firm’s revenue. But none of these tasks are investment outsourcing. Russell Investments is focused on the overall investment portfolio and how the portfolio helps achieve the overall plan’s benefit security and financial objectives. Compare the services of an actuarial firm that has an outsourcing practice with the services of a dedicated OCIO firm like Russell Investments, and we believe you’ll find that we provide more robust services.

The chart below shows the services that a typical actuarial firm with an outsourcing practice provides to their clients vs. the services that a provider like Russell Investments’ dedicated OCIO business provides.

For example, when a plan sponsor decides to undertake a risk transfer, delivering an in-kind portfolio can often be economically advantageous. In this case, there’s a role for a transition management provider to reshape the existing portfolio to the insurer’s specifications. We’ve done this for both our OCIO clients as well as clients of other investment outsourcing providers. In the latter case, we have often encountered blind spots in managing the risk-transfer process. For example, assumptions for transition costs may have been over- or under-estimated—and we were able to use our real-world experience to help refine these estimates for plan sponsors, giving a truer view of the economics of the transaction.

(Click on image to enlarge)

When outsourcing specific responsibilities, institutional investors want to put decisions into the hands of the organization best placed to make those decisions. We have been in the OCIO business a long time, and we’ve seen a lot of business models come and go. The key difference between what an OCIO provides and what an actuary provides can be summed up in one word: focus. Most actuarial firms have broad-reaching businesses where outsourcing is just a small part of what they bring to the market. Because of this, they often lack the in-house capital market, manager research, and portfolio management capabilities provided by a firm that has OCIO as their core focus. At Russell Investments, we have a unique and broad array of OCIO competencies. Because our success is directly aligned with—and in fact is dependent on—the success of our OCIO clients. We firmly believe that the arrangement which provides the best outcomes for most plan sponsors is to work with both an actuary and an OCIO. This helps fiduciaries in two ways: One, fiduciaries can evaluate the services and performance of both providers separately—which allows for objective evaluation of each firm’s contributions toward achieving the plan’s goals. And two, if it is decided that one provider is to be replaced, fiduciaries aren’t put in the position to search for each of these critical partners at the same time. This type of arrangement allows for a strong partnership between the two organizations—allowing each firm to bring their best to bear to help you achieve your goals.