More or fewer clients: Is there a magic number?

Most of us have spent the last 14 months blending together our personal and business lives. Working from home forces you to manage both simultaneously. Your family, friends and clients know you’re not on vacation, stuck in traffic or away at a business conference. This has presented a significant challenge for those of us in financial services because of the sheer number of client relationships that need to be managed along with balancing our personal lives. I experienced several instances when I was overwhelmed by the magnitude of demands: people to call back, emails that needed a reply and friends who were calling me in the middle of the workday because they were taking a break. The tipping point for me was when I didn’t have enough time in my workday to do it all.

Have you ever received a message from a client: “long time no speak?" Even worse, you’ve been meaning to reach out to a client—only to see their accounts transfer without any notice. Most people take it personally or even get offended, but you shouldn’t. It’s not you, it’s the Rule of 150. In Malcolm Gladwell’s book, “The Tipping Point”, Gladwell cites the research of British anthropologist and evolutionary psychologist Robin Dunbar. Gladwell states, “The figure of 150 seems to represent the maximum number of individuals with whom we can have a genuinely social relationship, the kind of relationship that goes with knowing who they are and how they relate to us. Putting it another way, it’s the number of people who wouldn’t feel embarrassed about joining uninvited for a drink if you happen to bump into them in a bar.” This is known as Dunbar’s number1, and includes family, friends and work relationships. In Dunbar’s research, he categorizes the 150 people: five intimate friends/family, 15 good friends and 50 friends, which leaves room for 80 potential work-related relationships.

If you stop to think about the number of close family members, friends, work colleagues and clients you have, it’s likely the number reaches well over 150. Dunbar’s research has caught the eye of various industries over the last few decades with some adopting the number as part of their everyday operations. Gore-Tex, a well-known consumer brand, follows Dunbar’s number by constructing office buildings with a limit of 150 employees and 150 parking spaces. When the building reaches capacity, they build another facility. In fact, Western armies have been operating in units of roughly 150 soldiers for hundreds of years.2 As human beings, science has shown that it is difficult to manage and maintain more than 150 total relationships. For this reason alone, we should regularly evaluate how we run our business and the relationships we continue to foster.

Be intentional with your time

According to the 2019 American Time Use Survey, conducted by the Bureau of Labor Statistics, the average American adult gets 8.8 hours of sleep per day, spends 1.2 hours eating and 5.2 hours engaging in leisure activities for a total of 15.2 hours of time spent outside of the workplace. Leisure activities included watching TV, socializing and exercising. Please note, this does not include time on social media, which as of 2020, takes up 2.2 hours of an average person’s day.3 This leaves us with 8.8 hours of remaining time.

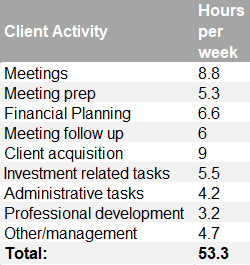

Coincidentally, a 2019 financial services survey conducted by Kitces research shows the average financial advisor reports spending 43 hours per week working, which equates to 8.6 hours per day. However, when Kitces probed more deeply, the survey identified how advisor time demand broke out by activity. The graph below illustrates the time demand placed on financial advisors during a work week.

Hence, there is a disconnect. The average advisor works 43 hours per week but has 53 hours of duties required to meet client demand. Research shows that clients are not satisfied with the level of communication they receive from their financial advisor:

A December 2019 study by research firm YCharts revealed most clients said they do not hear from their advisors as often as they would like. 64% of those surveyed said their advisor infrequently or very infrequently contacted them. 66% said more contact would give them more confidence in their advisor, while 75% said it is important for advisors to anticipate issues and contact them in advance. The study also found 86% of respondents said their advisors’ communication styles were important, while 88% said it was a factor in whether they remained with the advisory firm.4

So, how many households do successful advisors typically serve?

According to a recent McKinsey report, the top 25% of advisors in North America serve 140 households with an average of 3.4 accounts.5

According to Dunbar’s number, if you consider advisors already have 70 friends/family relationships, that’s 60 households above their work-related capacity (which Dunbar indicates should be no more than 80). As a result, what tasks fall through the cracks? Are phone calls and emails getting returned on time? Is paperwork and trading being done correctly? Even more importantly, do you have the proper work/life balance? As I struggled with these issues during the pandemic, I embraced our firm’s business solutions techniques to help me solve these challenges. The categories I focused on were: service model, relationships and how I run my business.

Service model

The first step to take is to assess your current service model. According to our methodology, three effective questions to ask yourself are:

- Calculate your capacity: How many households are you currently servicing?

- Time audit: How much time to you need to execute on your current service model?

- Service model: What service model will best serve your clients going forward?

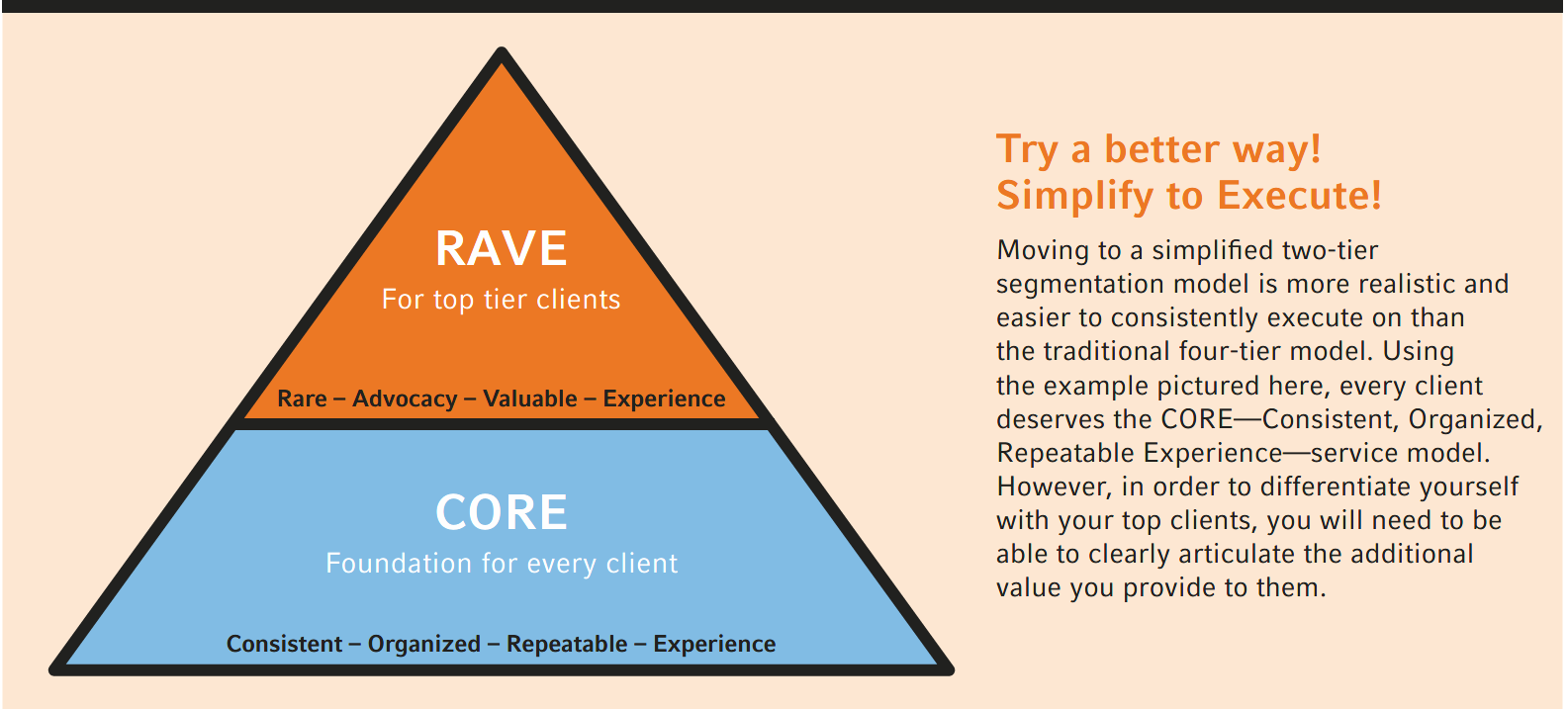

Consider developing a two-tier client segmentation and service model.

Over the last few decades, we’ve worked with thousands of advisors who have struggled to find capacity in their business. We have found that the most successful advisors spend more time with their top clients, building relationships and creating client advocacy. One key component is narrowing the time deficit identified earlier and streamlining your client service model.

Our business solutions team at Russell Investments advocates for a two-tier client segmentation and service model. Recently, a colleague of mine wrote an article about implementing a two-tier system. Following the 80/20 rule, identify your top 20% of clients by revenue as top-tier and building a RAVE (rare, advocacy, valuable, experience) service model. The remaining 80% are identified as CORE (consistent, organized, repeatable, experience)

Click image to enlarge

Personal relationships

Time is precious. We should be intentional about the relationships we choose to fill that time. A good place to start is to take inventory of your family, personal friends, work and client relationships. Who are the people in your list of 150? The next question to ask is, are the people within your 150 a positive influence on your life? If not, consider disengaging with them over time and incorporating others into your circle who may enhance your life.

Consider developing a strategic focus within your practice

Developing a strategic focus within your business allows you to leverage your relationships, expertise and personal interests. As professionals, we naturally gravitate toward people with similar interests. Focus on challenges that these groups may face and specialize in solutions that can be delivered in a customized way that can result in viral marketing. Once everything is aligned, your 150 can become the referral engine your business needs to thrive.

Business operations

There is no silver bullet for running a wealth management practice. Dunbar’s number has provided us with insights into the optimal number of relationships a human being can handle before things start falling through the cracks. The Bureau of Labor Statistics research tells us how we spend our time. As wealth management professionals, it’s important to be intentional with how you run your business. There are only so many hours in a workday and you don’t have control over time, but you do have control over what you do with your time.

Consider systematizing your practice

Systematize your business. Ask yourself the following question: If you unexpectedly were called away from work for an extended period of time, would your staff be able to seamlessly run your business? One consideration as it pertains to systemization is creating a checklist for your entire business. Some of the most complex occupations run with the aid of a checklist. In the book "Checklist Manifesto", author Atul Gawande writes, “Four generations after the first aviation checklists went into use, a lesson is emerging: checklists seem able to defend anyone, even the experienced, against failure in many more tasks than we realized. They provide a cognitive net. They catch mental flaws inherent in all of us—flaws of memory and attention and thoroughness. And because they do, they raise wide, unexpected possibilities.” Creating a checklist for processes and procedures to effectively run your business will empower you to focus your limited time in areas that leverage your 150.

The bottom line

The world we live in has dramatically changed in the last 14 months. COVID-19 has changed the way we do business, the way we service our clients and the way we utilize technology. Arguably, this is the ideal moment to identify the people in our lives with whom we want to proactively invest our time, energy and include in our 150. If you’re skeptical of Dunbar’s number, reflect on your own life. How many people do you see at family weddings? How many people attend religious services when a family member or friend passes away? If you’re on social media, how many people wish you a happy birthday each year? When I did my own reflection, each occurrence roughly came out to Dunbar’s number. Next time you leave someone a few messages with no response or wonder why you haven’t heard from someone in over a year, don’t get offended. Ask the following question, Am I in their 150?

4 Advisors Magazine: Abrupt market downturn sees advisor-client talks boom

Based on responses of individuals who currently invest $500k in AUM with financial advisors and wealth managers surveyed in “How can advisors better communicate with their clients”, December 2019 by YCharts. Total sample size represented 650 individuals across the U.S.