Q4 2022 Economic and Market Review: Stay in the game!

Do markets go up more than they go down? Are we in a recession? Why did bonds struggle in 2022? And why oh why do I have to pay taxes on capital gains when the market was so awful last year?

Each of these answers can be found in Russell Investments’ Economic and Market Review, which we update and share each quarter. This commentary is produced by an amazing team of investment professionals who work together to assess the latest market trends and recent performance, as well as what’s driving opportunities across equities and fixed income. The review also includes a look at historical comparisons of markets in general and our insights on the economy, taxes, capital gains and more.

Key takeaways from Q4 2022

Here are a few highlights based on questions we have received from clients over the last quarter. Check out our Economic and Market Review page, which includes short videos covering the issues addressed in the presentation.

Q: What are capital gains? And why did they make 2022 more difficult?

Mark Eibel: We can all agree that 2022 was a tough year in markets—in fact, equities were down approximately 19% at the end of the year. If investors held equity funds in a non-qualified (taxable) account(s), those funds likely paid out a distribution. Well, guess what? Those distributions (dividends) are taxable. So—adding insult to injury—even if the performance of your account went down, you still get to pay taxes.

Call to action: If you are an investor or financial professional, take a look at the potential benefits of active tax-managed investing—and how it can help you keep more of what you earn.

Q: Should I have waited to invest when the market was up? It seems like I have the worst timing.

Mark Eibel: This graph looks at the recessions over the last 50 years. If you had invested $100 during any period where there has been a recession, your three, five and 10-year returns on that initial investment would have been positive, with only a few exceptions. Remember, the market is a forward-looking mechanism. If you’re waiting for an all-clear/everything-is-OK signal to invest your money, you’ll probably never get it. In addition, it’s virtually impossible to time the market—i.e., to get in at the lowest point, and exit at the highest point. Trying to time the market usually results in missing too many of the up days—and remember, markets go up more often than they go down.

Call to action: Stay in the game, unless you have a short time-horizon. You will probably be glad you did.

Q: If I had a capital gains payout in 2022, how much in taxes would I owe?

Mark Eibel: Here is our capital gains story again. 😊 Capital gains can get paid out in a year where markets are up—and in a year where markets are down. This illustration puts real numbers on capital gains payouts aligned with real tax rates on real dollar amounts. The one example from 2022 shows a tax bill anywhere between $9,600-$15,000. YIKES! There's nothing more difficult, particularly in the down years, than having to pay a big tax bill on top of investment losses.

Call to action: For your non-qualified assets that are susceptible to taxes, make sure you are talking to your advisor about solutions to minimize that problem.

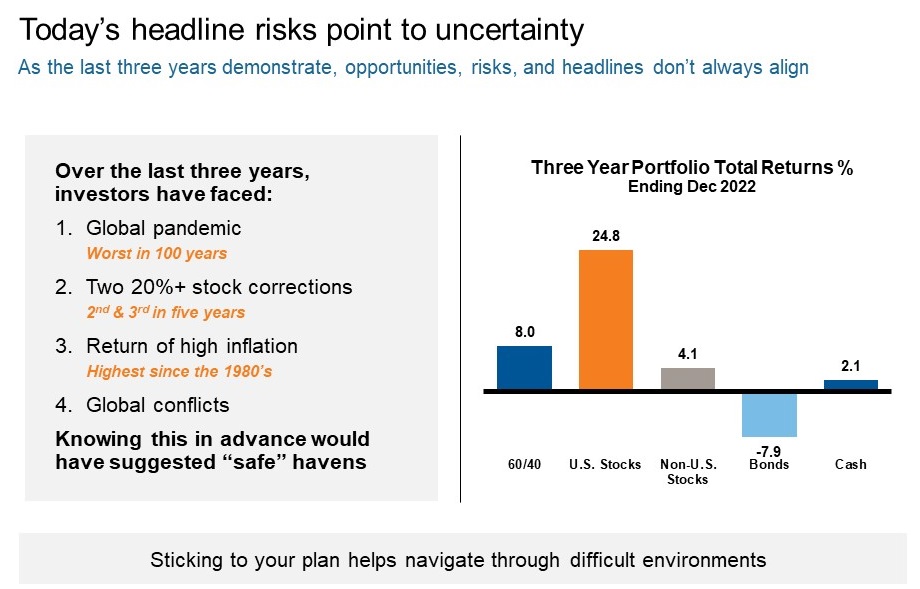

Q: With the amount of market volatility over the last three years, I feel like I should have just stayed out of the market. Am I wrong?

Mark Eibel: It sure has been a challenging last three years in our lives, both from a market perspective and just from a life perspective. We’ve gone through the worst pandemic in 100 years, staggering market volatility, decades-high inflation and a war between Russia and Ukraine, just to name a few. What’s interesting, though, is that when we look at the total return on a 60/40 portfolio, a U.S. stocks portfolio or a non-U.S. stocks portfolio, we see positive performance numbers for all three. So, rest assured that your persistence paid off by staying in the game with a diversified portfolio.

Call to action: If you have an investment time period of longer than three years, stay invested. I think you'll be glad that you did in the long run.

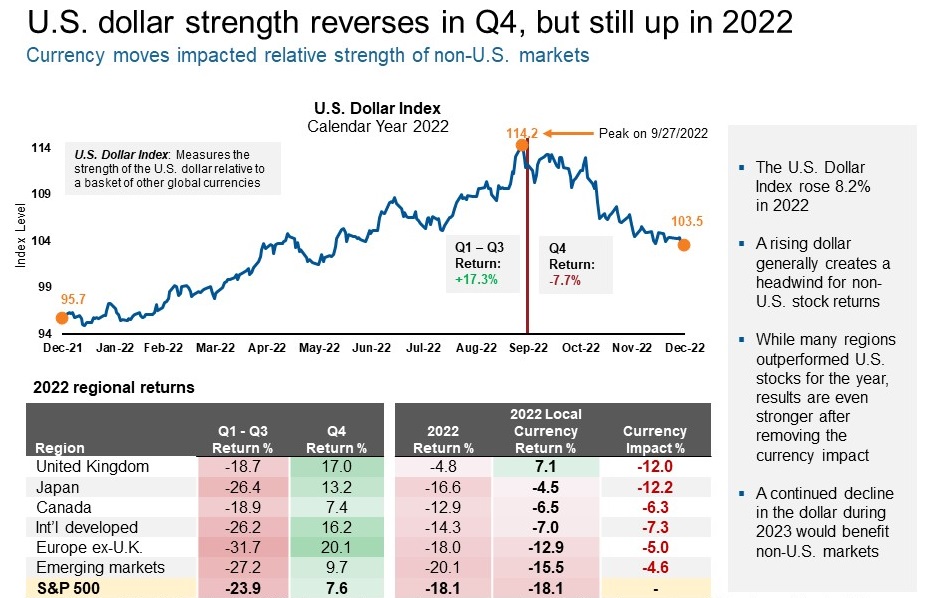

Q: What happened to the overall purchasing power of the U.S. dollar in Q4?

Mark Eibel: Good question. A strong dollar means that when you translate earnings outside of the U.S. into U.S. dollars, you get fewer of them—and the dollar was very strong in 2022, rising over 8%. However, the strength of the dollar reversed in the final quarter due to U.S. growth concerns and a potential slowdown in Federal Reserve rate hikes. The impacts of this to non-U.S. markets were notable, with international markets rising nearly 18% in the fourth quarter of 2022. The image below shows how key non-U.S. markets fared last quarter. It’s always fascinating to see the short-term impact of currency on returns.

Call to action: A continued decline in the dollar during 2023 would benefit non-U.S. markets. However, if a recession does strike the U.S., investors may pile into government bonds, which would prevent the dollar from weakening materially. With so much uncertainty, we believe it’s best for investors to maintain a diversified portfolio and steer away from any outsized currency bets.

The bottom line

The Economic and Market Review is a quarterly piece that our Russell Investments sales team is privileged to share with both financial professional and end-investor audiences. Give us a call or send us an email and we are happy to review further with you.

And, to finish off where we started, we believe investors that stick with the markets through thick and thin will likely be rewarded. In other words, stay in the game if your investing time-horizon is greater than three years—because the game is far from over.