Value has trailed growth, but that won't always be the case

The growth-versus-value debate continues, and the growth voices have gotten stronger given the decade-plus run of large cap growth names. However, we all know that investment decisions should not be based solely on what has been working recently. Investment decisions should be based on multiple considerations, and this blog post looks at three that should probably influence growth and value positioning moving forward:

- Markets tend to run in cycles

- Long-term history suggests that value has a role

- Coming out of difficult economic periods, small and value stocks have historically led market recoveries

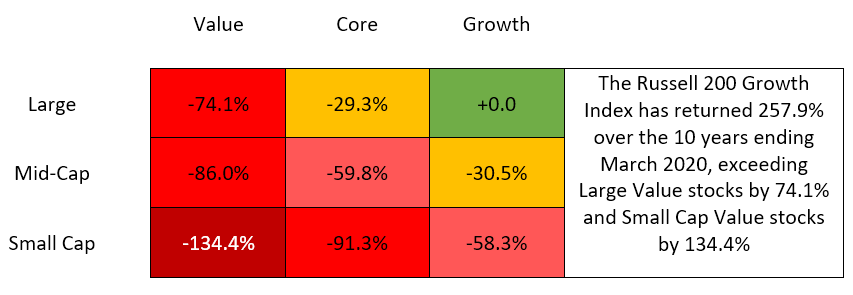

Markets tend to run in cycles: Growth stocks have dominated over the past 10 years

U.S. large cap stocks have been on a historically strong run relative to the rest of the stock market. The style box below shows how much large growth has dominated the other styles over the 10 years ending March 31, 2020.

Click image to enlarge

Large Cap: Russell 200 Growth Index, Russell 200 Index, Russell 200 Value Index, Mid-Cap: Russell Midcap Growth Index, Russell Midcap Index, Russell Midcap Value Index; Small Cap: Russell 2000 Growth Index, Russell 2000 Index, Russell 2000 Value Index.

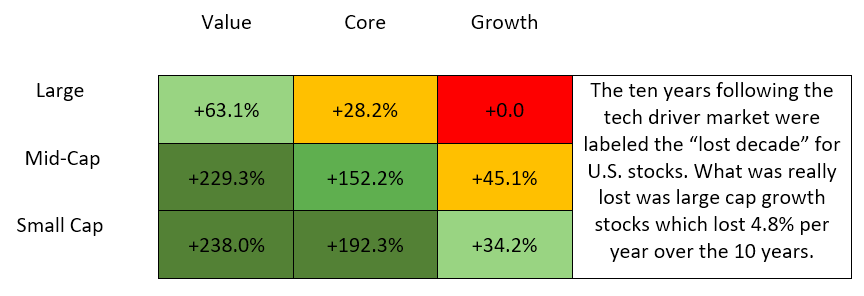

When market leadership lasts this long and the spreads become this wide, it can cause investors to rethink their diversified strategies. Is it time to jump on the large cap growth story and abandon smaller value stocks? For those that have been investing for a while, this narrative may sound familiar. Below is the same chart for the ten years ending Dec. 31, 1999, maybe the ultimate period for large cap growth investors. The pattern below looks very similar to the last 10 years.

Click image to enlarge

The ‘90s were a great 10-year run for all U.S. equity participants, but investors still were questioning whether to abandon diversification and pursue strategies heavily dominated by large cap growth stocks. For those that stuck to their disciplines, they were richly rewarded over the next 10 years, with small cap value stocks beating large cap growth by over 200%. For those that gave up on value stocks, they saw large cap growth stocks lose 4.8% per year over the next 10 years.

Click image to enlarge

A 10-year stretch is a significant time period in any investor’s horizon. A pattern that endures this long tempts investors to gravitate to it as the new normal. But, as we look back at the ‘90s, it was such an obvious bubble in hindsight and the following growth stock disappointment shouldn’t have been surprising. Will we be saying the same thing 10 years from now about the current stretch? History suggests we may …

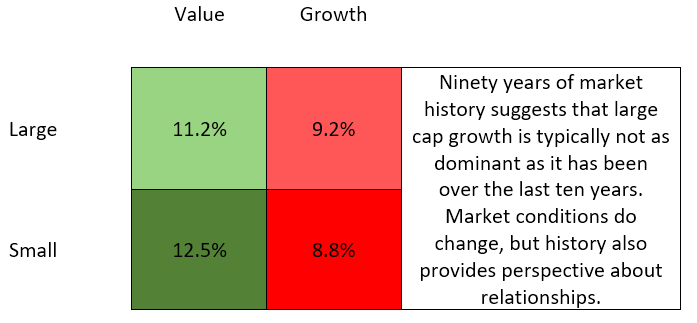

Long-term history suggests that value has a role

The long-term history of the stock market shows that growth stocks do NOT always dominate. Despite the duration of the current large cap growth run, for the 41-plus-year-history of the Russell Indexes, the small cap value index (Russell 2000 Value Index) has managed to maintain a modest lead over large cap growth (Russell 200 Growth Index): 11.4% versus 11.1% annualized (1979 - March 2020). Looking longer-term, the Fama/French stock market research returns have their own value and growth streams which date to the late 1920s. If one links that data to the Russell Indexes, the advantage of small value relative to large cap growth grows to over 3.0% per year (12.5% versus 9.2%), annualized back to 1930.

Click image to enlarge

The long-term impact of this history is not adequately portrayed by the 3.2% annual spread. For someone that was able to invest $1,000 in 1930 and invested it all in the large cap growth portfolio, it grew to an impressive amount of over $2,800,000. That’s the power of compounding 9-plus% a year over 90 years. However, if that same investor had put that $1,000 in a small value portfolio, it would have grown to over $56,000,000. That’s the power of compounding at over 12% per year for 90 years, and a reminder of why so many seasoned investors swear on the long-term benefits of small cap and value stocks.

Coming out of difficult economic periods, small and value stocks have historically led market recoveries

Also influencing the future direction of the markets is that we are in the midst of an economic recession. Growth stocks seem to be holding up relatively well during this period as growth sectors continue to function at or near pre-recession capacities. However, the rest of the economy will eventually start recovering and history has demonstrated that coming out of such periods, market leadership can and often does change. Here is what the average leadership has looked like for the five years coming out of the last four recessions that were accompanied by a 30%-plus market correction:

Click image to enlarge

Large Cap Growth: Fama/French Big Growth Portfolio 1930 -1978 linked to Russell 200 Growth Index 1979 - 31 March 2020; Large Cap Value: Fama/French Big Value Portfolio 1920-1978 linked to Russell 200 Value Index 1979 - 31 March 2020; Small Cap Growth: Fama/French Small Growth Portfolio 1930 -1978 linked to Russell 2000 Growth Index 1979 – March 31 2020; Small Cap Value: Fama/French Small Value Portfolio 1920-1978 linked to Russell 2000 Value Index 1979 - 31 March 2020.

Sources: http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library

These results shouldn’t surprise investors that follow market behavior, as markets tend to run in cycles and leadership changes often occur at economic inflection points.

To summarize:

- This has been a great run for large cap growth stocks, but markets run in cycles. The late ‘90s, and the 10 years that followed, should be a good reminder.

- Long-term history suggests that value and small cap stocks tend to win over time. That certainly does not guarantee the same results going forward, but does suggest abandoning such names may be a regrettable decision.

- We are in the middle of a recession. Coming out of recessions, equities tend to produce strong results. However, large cap growth stocks have trailed other market segments, on average, during those periods.

With these in mind, how should investors be thinking about and positioning equity portfolios?

- Will the large cap growth trend maintain its momentum?

- It is possible that the current large cap momentum continues for a while. However, to believe it will go on forever seems misguided, based upon experience. A more balanced profile including value and smaller cap names will likely be rewarded as markets tend to revert to their historical relationships.

- Coming out of the recession and the yet-to-be determined market bottom, what exposures will likely serve the portfolio best?

- Fortunately, we have limited experience over the last 40 years of coming off a recession tied to a 30%-plus market correction. However, during those last four occasions, smaller securities tended to lead relative to larger growth names. Diversifying away from the large growth names that have been dominating market results may benefit investors as the market begins to accelerate out of our current challenges.

- Should this influence how investors think about active and passive positioning?

- It has been a difficult stretch for active managers as they tend to underweight the largest, most highly valued stocks in the market. Fundamental approaches tend to seek less efficient market opportunities further down in the cap spectrum. An environment in which smaller, value-oriented securities lead, may be a more friendly market environment for active managers.

The bottom line

It can be difficult when one segment of the market leaves the rest behind. The temptation to follow the trend and abandon more diversified mixes can be very high, leading to classic buy high investor behavior. It is impossible to predict what comes next from the current market environment, but having diverse exposure to all segments of the market will provide investors with the opportunity to participate.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.

Related articles:

Growth pains? The case of leaning into value over growth

3 reasons why value stocks may outperform soon