$20 billion club: Higher rates means…higher return assumptions?

Executive summary:

- The average expected return on asset (EROA) assumption for the largest U.S.-listed pension plan sponsors increased to 6.70% in 2023—the first time a year-over-year increase has been observed in 19 years of records.

- Previously, EROA assumptions used for income statement purposes in the U.S. had only decreased year-over-year due to two factors: An increase in liability-hedging fixed income in DB portfolios and a decrease in expected returns on fixed income due to declining interest rates.

- 2023's increase in EROA assumptions is a recognition by large pension plan sponsors of a new, high-rate investing environment. Plan sponsors may want to consider potentially re-risking their portfolios to try to generate additional return to cover liability growth and some excess, depending on long-term objectives and current funded levels.

We've just completed our review of the 21 U.S.-listed companies with the largest corporate defined benefit (DB) liabilities using their recently released annual reports. The data is fascinating since this group is the bellwether for the corporate pension industry. The latest trends often begin with this group, whether it be pension risk transfer, cash balance conversions, or discretionary contributions.

What can we learn from this year's data? Plenty. It turns out that funded ratios for this group actually declined, with an average drop of 1.4%, despite relatively strong equity performance (these sponsors also have large allocations to fixed income). The gains on the assets were insufficient to overcome the losses in the liabilities due in part to a ~25 bps fall in discount rates.

Also, as previously reported, one of the largest corporate DB sponsors – IBM – made a significant shift from offering defined contribution (DC) benefits to offering DB benefits in their previously-frozen, overfunded U.S. DB plan. We have thoughts on how a shared DB/DC model could work to benefit both employers and employees. Their 10-k filing included a few other details we share in our report. It's a topic worth your time.

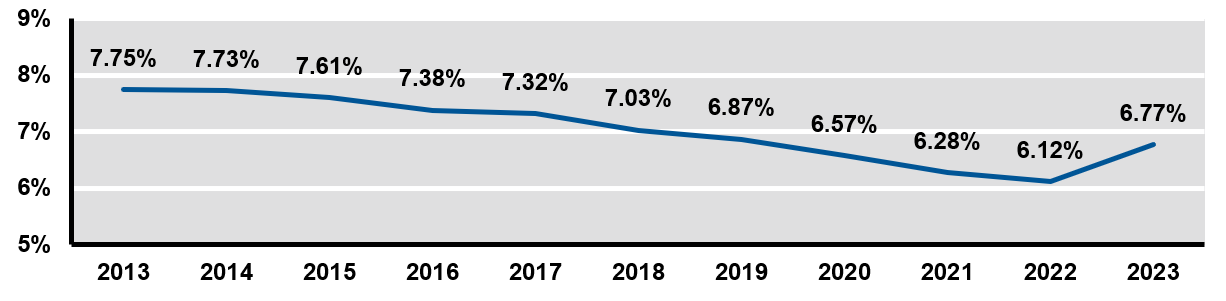

I would like to focus here on a development we have not observed in the 19 years' worth of historical data we have collected for this group. Not once in that time has the average expected return on assets (EROA) assumption increased year-over-year. We can attribute this decrease to two trends.

First, as my colleague Adam Field reported last year, these plan sponsors have made significant shifts toward liability-hedging fixed income over time, an asset class that generates lower expected returns than most other assets. In 2011, the average portfolio allocation to fixed income for this group was 37%. It has now increased to 54%. This is partly due to the adoption of de-risking glide paths, which naturally lead to more fixed income as funded status improves. Funded status last year reached its highest level since before the Global Financial Crisis in 2008, and sponsors have made significant progress on their glide paths.

Second, until 2022, the fixed income yield and expected return had generally declined. The combination of low yields and the potential for rising rates (which have a negative impact on fixed income returns) dampened fixed income return expectations, at least in the medium term. This impact, along with the higher allocation to fixed income, pushed EROA assumptions down.

It's hard to believe that just 11 years ago, the average EROA assumption for this group was 7.75%. In 2022, that number had fallen to 6.12%, dipping lower each year. Now, having reviewed the latest filings, we see that most of these companies increased their EROA assumption for 2023 pension expense purposes, with the overall average increasing to 6.70%, as shown here.

Exhibit 1: Average EROA assumption

Source: 10-k filings

This rise in return expectations is primarily due to the rise in fixed income yields, though asset allocation changes may also be at play. The material increase in rates in 2022 and its impact on EROA assumptions leads to a few important takeaways for plan sponsors:

First, the EROA assumption in the U.S. is used in pension expense calculations (i.e., the impact of the pension plan on the corporate income statement). Higher return assumptions will lower pension expense (or increase pension income) in isolation, but there are other moving pieces related to higher rates in this calculation. Pension expense calculations are complex and important to many plan sponsors, but changing the EROA assumption does not directly impact the economics of the pension plan.

Second, return assumptions have increased, but have liability return needs increased more? Liabilities grow with interest, so higher interest rates lead to higher asset returns needed to offset liability return requirements. This increase can at least partially be covered by higher expected returns in fixed income. We cover the interaction of these liability return elements in depth here.

Third, it's possible that the relative return advantage to investing in equities compared to fixed income is diminishing. While expected fixed income returns have improved in capital market assumptions over the last year or so, equity market returns may not have changed as much as fixed income, depending on the method used.

This could open up the discussion on potentially "re-risking" the portfolio (i.e., increasing equity-like exposure) to try to generate additional return to cover liability growth and some excess, depending on long-term objectives and current funded levels. That said, we generally would not advise scaling back on hedging interest rate risk. We cover the topic of re-risking here.

We will review the asset allocations of these companies in the coming weeks and report on whether they have made changes to their asset allocations associated with this trend, but for now, suffice it to say that these companies recognize we are operating in a new environment with higher rates, which could have investment implications that ought to be considered.