Iran attacks Israel. How could markets be impacted?

Executive summary:

- The initial market reaction to Iran’s attack on Israel was measured, with S&P 500 Index futures trading up 0.3%.

- Historically, geopolitical events have generally led to modest selloffs in equity models and a flight to safety in bond markets, with long-lasting impacts atypical.

- In the wake of Iran's attack on Israel, we believe that maintaining a slightly defensive posture across our portfolio strategies is appropriate.

Our investment leadership team convened twice on Sunday to discuss the conflict between Iran and Israel, its key watchpoints in the days ahead, and the pertinent risks onto markets, our investment portfolios, and our clients.

The team broadly agreed that maintaining a slightly defensive posture across portfolio strategies remained appropriate.

What happened

Several Iranian military commanders were killed in an airstrike on its embassy in Damascus, Syria on April 1. Iran warned for days that it would respond against Israel, leaving investors on edge. Ultimately Iran carried out its retaliatory attack on April 14—involving a wave of unmanned suicide drones, cruise missiles, and ballistic missiles launched against Israel. In a separate engagement, Iranian commandos also seized an Israeli-linked commercial container ship near the Strait of Hormuz over the weekend.

From an investment perspective, while the scale of the strike this weekend was jarring, there were important mitigating factors:

- Iran warned the world of its launches in real-time and sent a letter to the United Nations that its actions in the region had concluded before any projectiles even reached Israel. These steps might have been taken by the Iranians to reduce the risk of the conflict escalating further.

- Israel—with support from the United States and other allies—claims it successfully shot down 99% of the Iranian weapons systems, resulting in minimal damage, and there has been no loss of life reported thus far. This "success" could possibly inform the likelihood and extent of retaliation from the Israeli side.

Israel’s War Cabinet met on Sunday to discuss its response. Whether they choose to retaliate, and if so, whether that informs a further material escalation of the conflict (or not) will likely drive market sentiment in the near-term.

Initial market reaction

The initial market reaction as of 7 p.m. Eastern time on Sunday was measured and, if anything, indicative of a modest relief rally. S&P 500 Index futures traded up 0.3%, while the May 2024 WTI crude oil futures fell 0.4%. These moves only partially unwound the geopolitical risk premia that had accumulated in both over the last two weeks.

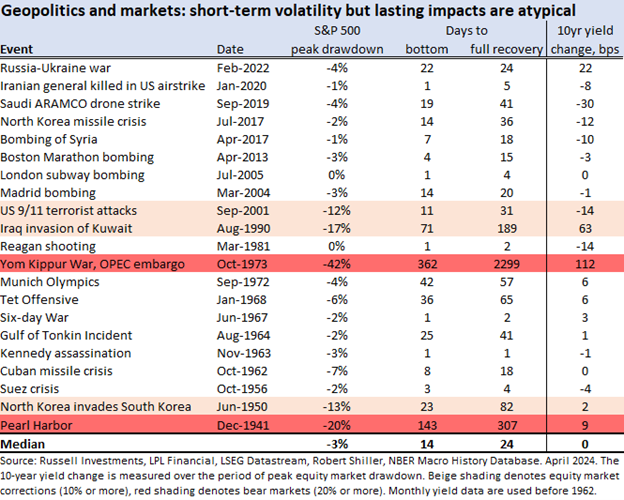

Lessons from history

While it is impossible to forecast the future evolution of the conflict between Iran and Israel with high confidence, history can provide some context on the ability for geopolitical events to impact markets. In the table below we show the response of U.S. equity markets and Treasury yields to past conflicts. While past episodes vary in their impact, geopolitical-driven equity market selloffs are typically modest (3%) and equities typically recover rapidly once the conflict has stabilized—with the S&P 500 Index typically re-achieving its pre-crisis levels in less than a month. In fixed income, our strategy team expects Treasury yields would decline in a stress scenario, but the details will matter for the asset class as crosscurrents from investor risk aversion (lower yields) and higher energy prices and inflation (higher yields) leave a checkered history.

The Yom Kippur War and subsequent OPEC oil embargo against the United States and other nations in 1973 was an exception, resulting in a more severe drawdown in markets as a doubling of retail gasoline prices and energy rationing contributed to a severe recession and stagflation period for the U.S. and other developed market economies.

Thankfully, the U.S. is much better insulated against energy shocks today. Relative to 50 years ago, consumers spend a smaller share of their budgets on energy products, and the U.S.—now the biggest oil and gas producer in the world—has become a net exporter of energy. As such we don’t think the current conflict has yet risen to the level of posing a systemic risk to the business cycle and financial markets. It might take a further escalation, potentially involving threats to the shipment of energy products transiting the Straits of Hormuz, to rise to this level.

Positioning

Before the Middle East conflict broke out, our investment strategy team had expressed some concern about expensive valuations in equity and credit markets and signs that market psychology had become lopsided and very optimistic (a cautious signal for the outlook).

Our portfolio management teams have generally been managing their strategies to risk levels consistent with this slightly defensive posture. Our multi-asset portfolios have exposure to duration which could benefit from a potential decline in Treasury yields in a risk-off scenario. Meanwhile, stock selection from underlying money managers is the primary driver of outcomes in equity portfolios. While this security selection has generally resulted in a very small underweight to the energy sector, the portfolio management teams remain comfortable with current exposures.

If markets did sell off more aggressively in coming weeks, that scenario could be a catalyst for us to move portfolios up from a slightly defensive to neutral allocation. Signs of investor pessimism and ongoing conversations between our research teams and money managers will guide those decisions.