3 reasons to consider infrastructure investment

For investors, there are opportunities in the $69 trillion global gap between actual – and needed – infrastructure investment over the next 17 years. What’s behind all this? What have institutional investors uncovered that could be helpful in generating an additional source of return?

Mind the gap

“Mind the gap” is an imperative for every tube, metro or train rider.

For investors, there are opportunities in the $69 trillion global gap between actual – and needed –infrastructure investment over the next 17 years. 1

Australian and Canadian institutional investors were early adopters of infrastructure investment and have been doing so since the 1990’s. Today, many other OECD countries’ large pension funds and public pension reserve funds have allocations to alternative investments, including infrastructure.2

What’s behind all this? What have institutional investors uncovered that could be helpful in generating an additional source of return?

Why infrastructure?

It’s no secret that we believe future market returns are likely to be lower than they have been in recent years — and many analysts agree with us.3 In fact, we view lower returns as the single greatest challenge facing investors today. We believe investors cannot afford to overlook strategies that may offer incremental return, nor take on risks they do not expect to get paid for; nor disregard implementation efficiency.

This is where infrastructure comes into play. We see it as an example of an asset class that cannot be ignored in the search for additional returns in a risk-controlled way. To understand why, it’s helpful to first take a step back and define what it means.

What is infrastructure?

Infrastructure is a fundamental building block to the functioning of modern society and can include energy, transportation and communication networks and systems. Within the broad infrastructure investment universe, there exists what we call pure play infrastructure. Pure play infrastructure investment assets typically provide essential services, operate in monopoly-like competitive positions and enjoy sustainable cash flows producing reliable income streams. By way of example, we consider an airport to be a pure play infrastructure investment asset, as opposed to an airline. Another example would be a toll road, as opposed to a construction company that builds the toll road.

Today, infrastructure investment is recognised by the institutional investment community as a stand-alone asset class. Indeed, many pension plans around the world have been attracted to the infrastructure asset class since the early 1990s. But why?

The case for infrastructure investment

We believe that the reasons for infrastructure to be included in a multi-asset portfolio are threefold.

- Growth in the investable opportunity set

The first reason is access to a global growth opportunity. Upgrading the world’s infrastructure will be a dominant theme over the next 20 years. In fact, it’s estimated that a staggering $69 trillion will be spent on infrastructure by the year 2035.4 In addition, given the fiscally challenged positions of many governments and municipalities, it’s likely that there will increasingly be a reliance on private capital to finance infrastructure spending needs.It’s also important to note this trend has already been developing globally over the last 10-15 years.

Case-in-point: The market capitalisation within the broad universe of publicly traded infrastructure companies was approximately $400 billion in 2005.5 Today, that same universe has a market capitalisation of between $2 and $3 trillion.This growth in the investable opportunity set has, and will likely continue to be, driven by the following factors:- Privatisation: Where governments sell ownership stakes to private enterprise. Examples of infrastructure that have been privatised include airports, toll roads, seaports and electricity transmission and distribution assets.

- Organic growth: Where the owners of infrastructure assets expand and grow their existing businesses. Examples include energy infrastructure companies expanding pipelines and toll road operators extending highways to facilitate increased user demand.

Enhanced yield potential relative to equities and bonds

The second reason to consider infrastructure investing is the enhanced yield potential relative to equities and bonds. Infrastructure companies historically provide a relatively high dividend yield, but importantly, they also exhibit predictable and resilient cash flows. The resiliency of cash flows attached to pure play infrastructure assets can be attributed to the following: essential nature of the service provided, structural growth, high barriers to entry and strong pricing power.- Portfolio diversification and downside protection

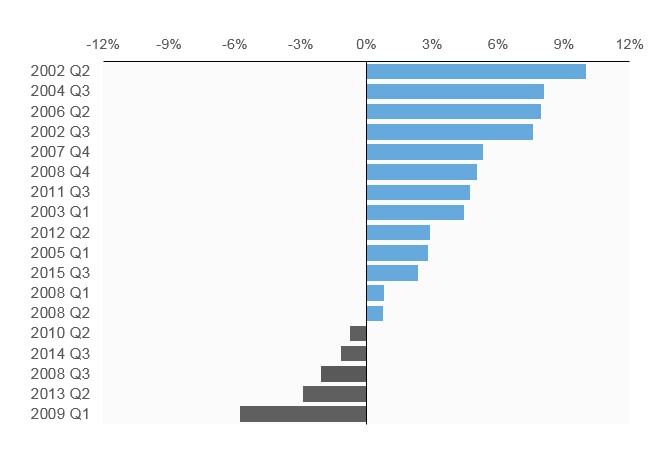

The third reason to consider infrastructure is portfolio diversification and downside protection. As a defensive alternative to equities, exposure to infrastructure can help manage total portfolio volatility, given its forecasted low correlations to stocks, bonds and real estate. Since 2001, infrastructure securities have outperformed global equities during 13 of the 18 quarters where the Russell Global Index experienced a negative quarterly return.6 On average, the S&P Global Infrastructure Index has outperformed global equities by 2.8% per quarter during negative quarters. And dollar for dollar, we believe downside protection may be worth more than upside growth.Chart: Outperformance of S&P Global Infrastructure Index vs. Russell Global Index during quarters of negative equity market performance

Maximising the benefits of infrastructure

We believe a well-defined and repeatable investment process is required to create an infrastructure portfolio to help achieve desired investment outcomes, and to deliver on the infrastructure investment value proposition. The following three considerations may be helpful to consider when investing in the infrastructure asset class:

Pure play

The unique characteristics of pure play infrastructure are what ultimately drive the portfolio diversification and enhanced yield (or income) associated with the infrastructure asset class. Caution is warranted when expanding the investable universe beyond pure play infrastructure companies (i.e. construction, airlines, telecommunications carriers), as this may expose investors to industries and businesses that are more cyclical in nature and whose revenues or earnings are much more dependent on the business cycle. In times of recession or economic downturns, these companies are more likely to suffer, therefore mitigating the portfolio benefits of the infrastructure asset class.

Global

Infrastructure is a global asset class, with an opportunity set in the trillions of dollars for decades to come. Over 80% of the world’s infrastructure investment needs are outside of Europe.7 By constraining portfolios to European infrastructure (which tend to have bias toward airport services, toll roads and electric utilities) investors may be forgoing investment opportunities in key areas such as multi utilities and energy related sectors.

Actively managed multi-manager portfolio

This may help mitigate single manager risk, in addition to providing access to the rich source of potential active management opportunities that infrastructure allows, including balanced sector exposures, alpha generation potential and prudent risk management.

While it is possible to gain passive exposure to infrastructure, there may be significant opportunity costs, including lower returns and greater risks, attached to forgoing active management in favor of passive implementation approaches. In contrast, actively managed portfolios tend to have more balanced sector exposures, emphasise pure play infrastructure investments and may be well positioned to exploit market inefficiencies such as business fundamentals, relative valuation and merger and acquisition activity. Active managers in this sector can also provide access to an expanded investment universe through out-of-benchmark exposures.

Infrastructure: A key part of a multi-asset portfolio

In short, we believe that infrastructure exposure can be a key part of a multi-asset portfolio. Infrastructure can provide an opportunity to help achieve desired investment outcomes while effectively managing overall risk at the total portfolio level. In today’s world of low returns, the game is on to unearth additional sources of return. Infrastructure may be worth the dig.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.

1 Source: McKinsey Global Institute, October 2017 “Bridging global infrastructure gaps”. The estimate of total demand is higher than the $49 trillion projection in 2016 research. It has been adjusted based on a longer projection period of 19 years (2017-35) (versus 15 years (2016-30)) base

year prices have been updated to 2017 from 2015 and GDP growth forecasts have been revised upwards, driving higher infrastructure needs, improved data and projections by external providers of water and telecom data.

2 Source: Annual Survey of Large Pension Fund and Pubic Pension Reserve Funds Report on Pension Funds’ Long-Term Investments 2015

3 Source: The ECB Survey of Professional Forecasters Third Quarter 2018 and Russell Investments Data as of June 2018

4 Source: McKinsey Global Institute, October 2017. “Bridging global infrastructure gaps”.

5 Source: S&P Global Infrastructure Index

6 Source: S&P Global Infrastructure Index, Russell Global Index, as of September 30, 2018

7 Source: Global Infrastructure Outlook, July 2017 https://outlook.gihub.org/