Eat your broccoli: 3 approaches for investing cash on the sideline

Take your medicine! Eat your broccoli! Rip off the plaster!

We know what is good for us, but do we always do it? No.

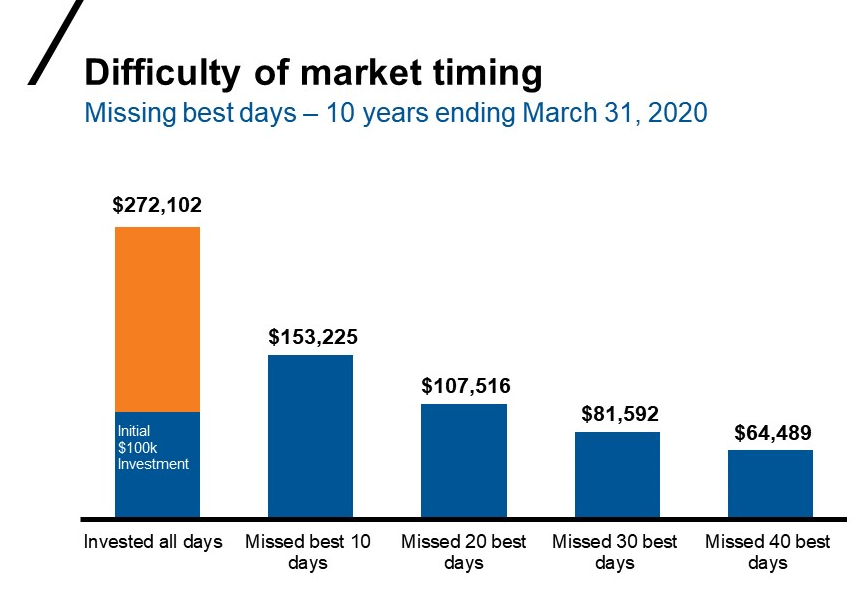

Studies have shown it is not about TIMING the market, but TIME IN the market. For the lucky ones that raised cash prior to the market peaking in February that saw this coming, or for those who capitulated and went to cash in mid-March, you now have another decision on your hands: when and how do you get back in? FOMO - fear of missing out - is pricey. Despite the generally bullish markets over the last 10 years, just missing out on a few of the best days can drastically reduce your ending wealth.

Click image to enlarge

Source: Russell Investments, Confluence. In USD. Returns based on S&P 500 Index, for a 10-year period ending 31 March 2020. For illustrative purposes only. Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly.

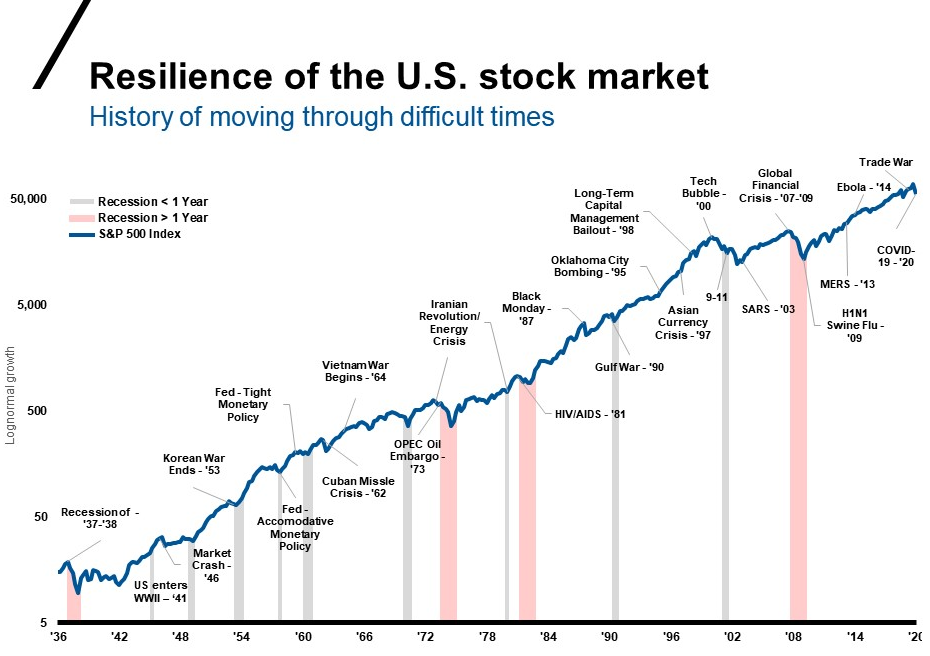

The point is: don’t start a love affair with your cash, as many investors did in 2008-2009, and forget to move on to a healthier, potentially more profitable relationship. Fear can seem to always give you a reason to not get back in, but those fears are not reflected in the reality of the markets. As you can see in the chart below, we’ve experienced other major historical events before - and the market has persisted through and out of each one.

Click image to enlarge

Source: Morningstar Direct – S&P 500 Index, St. Louis Federal Reserve. Data as of 31 March 2020.

Let’s look at 3 strategies for re-entering the market

When it comes to investing back into the markets, there are three schools of thought around the entry point:

1. Invest it all at once

Ripping off the plaster and putting it all to work at once has historically been your best option, because the stock market tends to go up most of the time. However, this option also carries the biggest psychological burden of regret and anxiety.

Many investors assume stocks drop right after they put their money in because the system is rigged! From a behavioural perspective, investors feel much worse seeing stocks fall after investing a lump sum, when compared to the good feeling they should have after seeing stocks rise by the same magnitude after investing the same lump sum amount. This is the human bias of loss aversion: a cognitive phenomenon where a person is affected more by a loss than by a gain.

2. Have a set schedule (i.e., dollar cost average)

I like to call this the no regrets method. If you invest some money and the market goes down - that’s OK, you have more dry powder ready to go. If you invest some money and the market goes up - great.

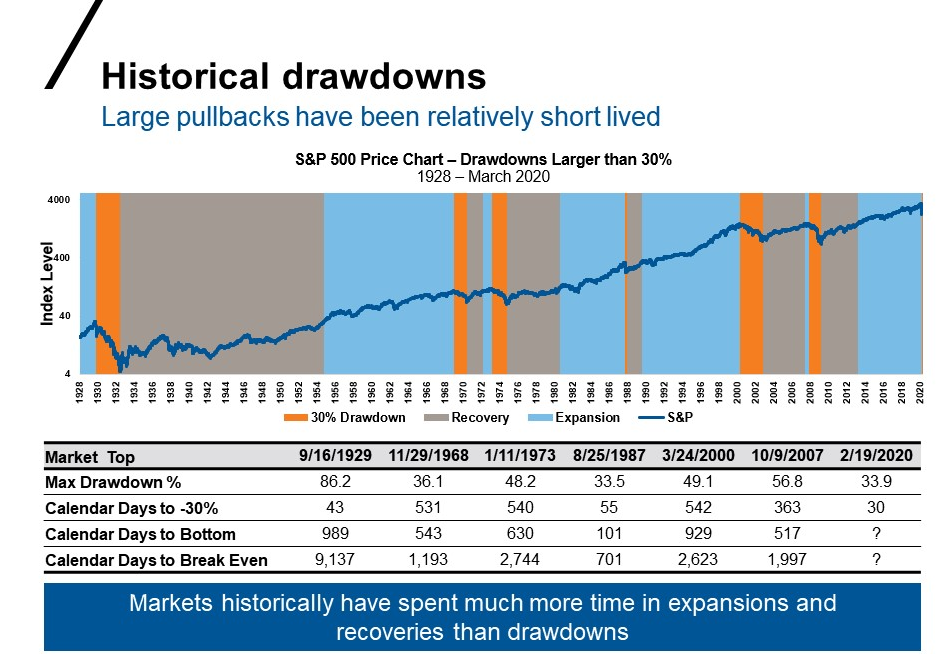

The amount or frequency doesn’t matter as much as simply having a plan and sticking to it. The chart shows that in the last five drawdowns and recoveries since the Great Depression, the average bear market has lasted roughly 18 months (544 days) from peak to trough, with the breakeven point reached in about another five years (1,851 days). What this shows is that we spend much more time in recoveries and expansions than in drawdowns (even though it might not feel that way).

As we have seen since the beginning of the year, the market can move very fast, and having a plan in place is essential.

Source: Factset and Morningstar. Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly.

3. Using a catalyst

Having a specific catalyst or even an entry point in mind is the final option. For instance, you may decide to deploy your investments when stocks go down another 10%. As you can probably imagine, the issue is that the market does not cooperate with your targets and you may never find the perfect moment to deploy your cash. We may be back to where we started.

The bottom line

The goal is not to have perfect timing on every investment. Instead, we believe it's best to work with an investment professionalto establish a consistent plan that accomplishes YOUR desired outcome. Like eating your broccoli, some bites may not make you happy, but you’ll be more financially healthy because of it.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.