What role can private markets play in a total-portfolio strategy?

When our clients want to talk with us about return-seeking strategies, the conversation most often turns to private markets. No surprise. An increasing amount of capital formation and access to growth and income opportunities occur in the private markets. The private markets category is too powerful of a tool not to consider. And we believe it should be a significant portion of many portfolios. But with that power comes complexity, particularly in the form of the different types of risks to consider.

It is important to demystify private markets and take the risks they introduce and manage them, as with any core investment risk in the portfolio. Given the breadth of private markets available, the category itself must be fully understood. It must be approached with both the right understanding and the right level of access. Just as importantly, successfully navigating that complexity demands risk management at the total-portfolio level.

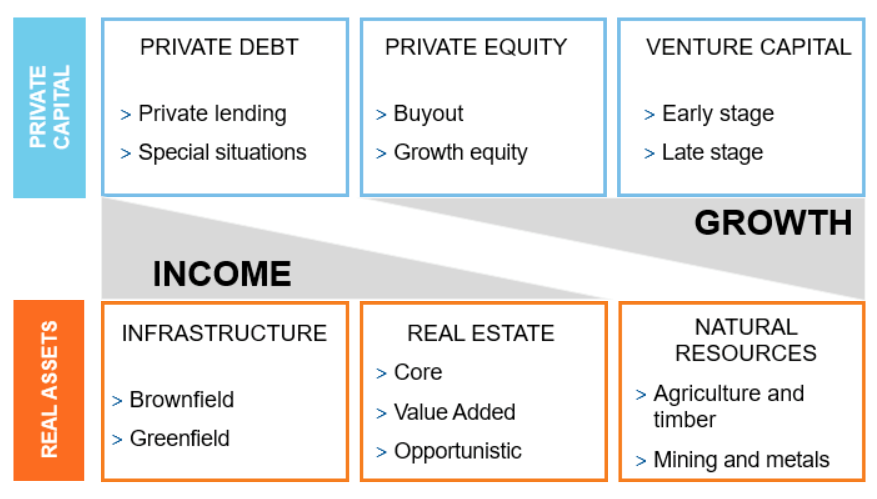

What are private markets?

Click image to enlarge

Source: Russell Investments. For illustrative purposes only. Brownfield refers to mature, existing assets. Greenfield revers to new construction.

Public and private exposures working together

We keep hammering the total-portfolio theme for many reasons. First, it’s vital to stay focused on primary portfolio objectives, the core exposures to target and the risks that can’t be allowed. This clear anchoring can often result in very different private markets portfolios for different investors. Keeping those clear objectives in mind can target private market strategies that align with the overall goal, be it return, income or a certain liquidity profile.

Once we know the blueprint for the total portfolio, we can better build the pieces. In general, we believe higher levels of skill and less constrained active risk leads to outperformance. That’s amplified with private markets, where even in a more diversified portfolio, investors may want to lean into certain asset types or sectors. Here at Russell Investments, for example, I don’t want my private-markets team to feel handcuffed by worrying about over-exposure in a specific sector or aligning to a long-term target in any given year. I want them finding the best return opportunities. But I understand those private markets opportunities are more complex and less flexible. So then, I need the publicly-traded portion of my portfolio - which is inherently nimbler - to adjust to a PM opportunity to keep my overall portfolio exposure and diversification intact. In simple terms, private markets exposure works well as a return lever only when you have an equal and opposite lever to move in public markets - a total-portfolio approach.

It’s important to note that, for most investors, either building a new private markets exposure or managing an existing PM exposure requires a dynamic approach as well. I’m not talking about market timing, but about ensuring various types of access points are considered when building the exposure, and then dynamically managing the total portfolio as objectives change and markets shift.

Secondaries as a source of returns

One fundamental belief in privates is the importance of diversifying across vintage year. Private equity tends to make chunkier allocations - buying actual companies instead of just shares in companies. That means that what was purchased last year can’t be purchased this year, so the opportunity set every year is inherently different. But if an investor leans too heavily into that approach, it could take years to build a new private markets allocation. And nearly all investors need the returns now.

Secondaries can help. Secondaries are simply private assets being sold in the midst of their investment period. In early stages of a privates program, using secondary investments as a core return source can be useful to get money in the ground quicker, while still maintaining vintage-year diversification. This can be done for strategic reasons or risk management needs. With the right level of access and the skill to identify attractive pools of secondary assets, investors may be able to build a PM portfolio both more quickly and in a more risk-managed way. Over time, as new vintage years are then layered in through primary investments, the allocation to secondaries may be reduced, but that allocation can still remain an attractive return source.

The importance of a dynamic approach

Further, as the private portfolio matures, the underlying exposure will shift, based on new investments but also based on the pace of realisation for existing PM investments. This is a key reason a holistic and dynamic approach to portfolio management matters so greatly. Instead of thinking simply in terms of two-dimensional diversification - public or private - best-in-class asset managers can matrix that into multi-dimensional diversifiers, by layering in vintage year, geography, cap-size, manager skillsets and more, all with the intention of generating outsized return while potentially creating even greater diversity at the total-portfolio level.

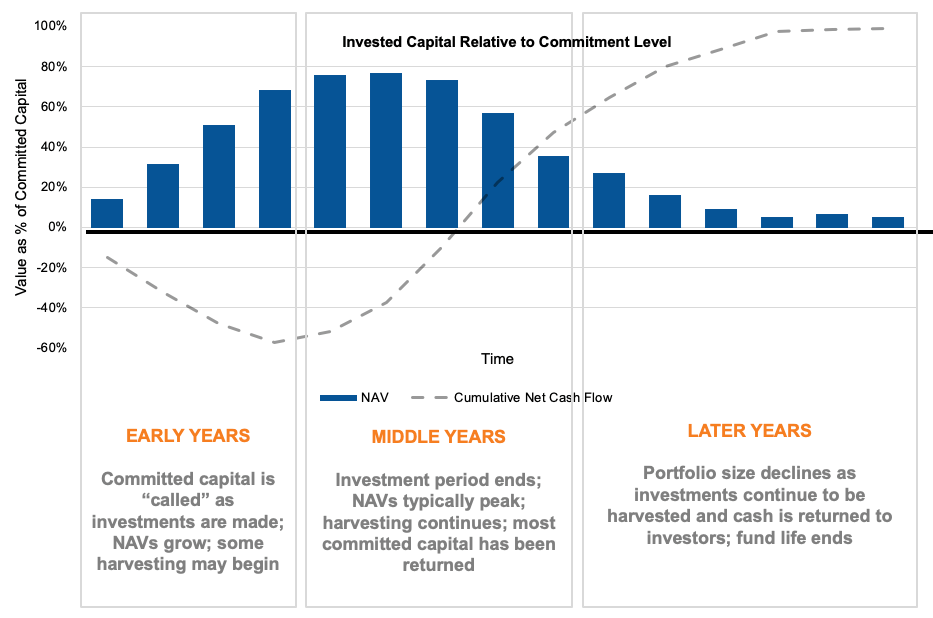

Life cycle of a private markets fund

Click image to enlarge

Source: Russell Investments. Illustration indicative of cash flows and Net Asset Values (“NAV”) for a typical private markets fund. There is no guarantee actual cash flow and NAV profiles will reflect the estimates shown.

Bringing it back to the total portfolio, with proper look-through and awareness, private market risk can be managed by using the publicly traded portion of the portfolio as a lever. This dynamic management can help ensure that both the public and private portions of the portfolio are complementing each other along the way. This simple but critical discipline is often overlooked when portfolios are thought of simply as pieces and there is not an integrated way to better manage risk across the entire portfolio.

Integrated holistically, private markets can add diversification of return sources. They can also help provide resilience during market downturns. And the longer time horizons may help reduce behavioural investment mistakes, as investors are required to take a longer-term approach. By working with a solutions provider who understands both the nuances of the PM category and the intricacies of a total portfolio, investors can use private markets to diversify even further and increase the likelihood of meeting overall objectives.

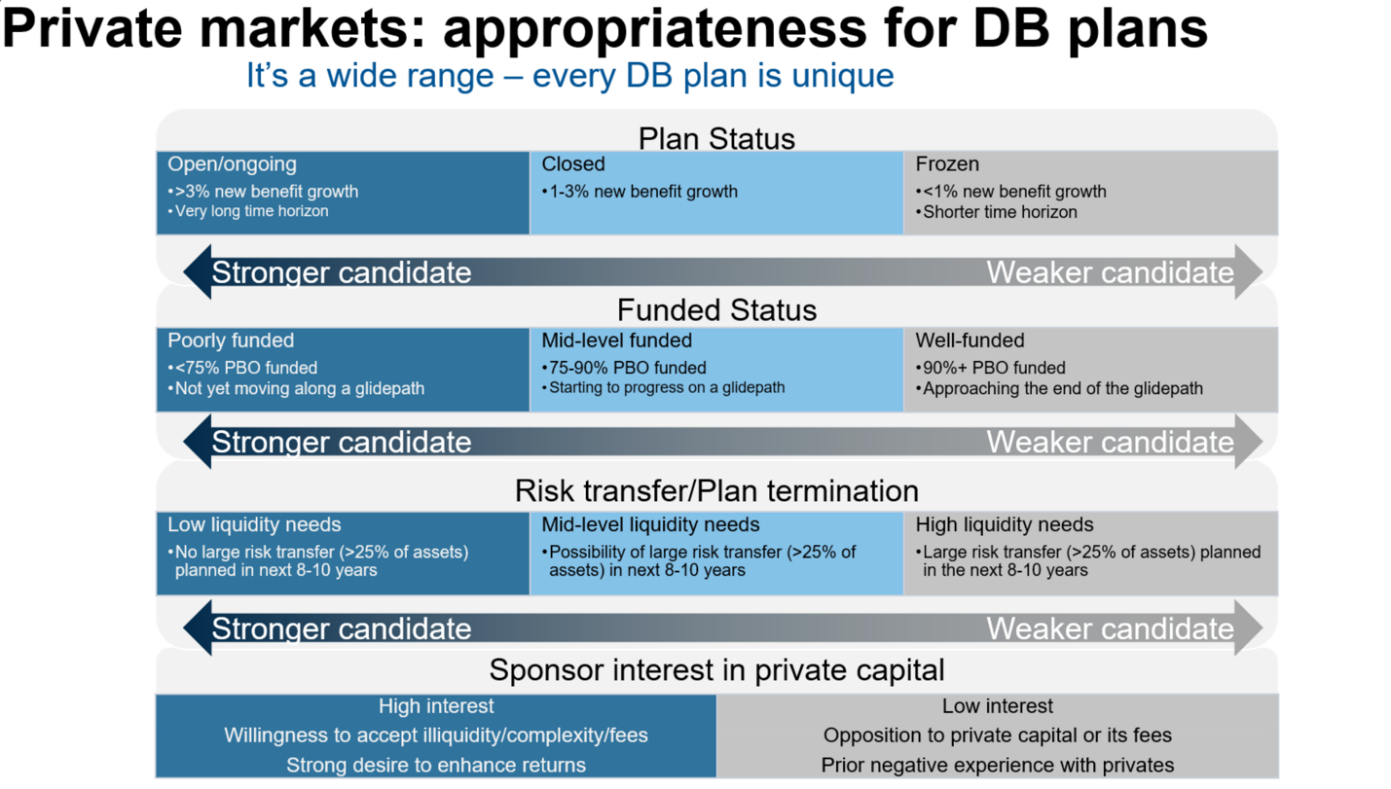

No matter who invests in private markets, a holistic approach still matters

Are private markets right for everyone? Because they come with longer time horizons, the simple answer is probably not. But a more accurate - and more nuanced answer - again looks at this from a total-portfolio level. It becomes less a question of yes or no to private markets and more of a question of what size and composition of allocation to PM makes the most sense.

A non-profit endowment with a long investment horizon and a need to overcome a 5% annual distribution and 2% inflation, has a demand for a 7% return that is close to non-negotiable. As a PM candidate, we believe they’re a hard yes. On the other extreme, a very well-funded frozen DB plan is probably far less of a candidate. The time horizon may be too short and the dependence on high returns may not be great enough. But for the majority of investors who live along this spectrum, the allocation answer, as the chart below shows, is likely significantly more than zero.

Source: Russell Investments.

The amount of illiquidity an investor can tolerate is often much higher than perceived. Understanding the cash-flow profile associated with different types of private markets investments is also useful in this regard. Funds distribute capital throughout their entire life and investors do not have to wait for the end of a fund’s life to regain committed capital. For example, in a typical buyout fund, investors can reasonably expect to receive their capital commitments by years 7-8. In private credit, the timeline is shorter, with committed capital being returned by years 5-6. We believe it’s worth a little professional analysis that considers other assets in the portfolio and tests for stress events. Determining the optimal level of privates - and the types of privates - can result in a liquidity-risk profile that not only meets overall needs, but also creates the opportunity to pick up extra return or yield.

Why the right partner matters

Private market investing provides both powerful opportunities and potential hazards. We believe there are five key reasons that show why it’s vital for investors to work with the right strategic partners:

- A total-portfolio approach – Big surprise, right? But, if you skip everything else on this list, make sure your strategic partner has both the depth of platform you expect from a private markets specialist and a total-portfolio approach. There are more ways than ever before to access private markets. And while this may mean more opportunities for customisation, it also means more complexity. Work with a partner that knows how to build a total portfolio, knows how to balance both privates and publics, and knows how to dynamically manage portfolio changes over time.

- Access and sourcing – In private markets, outperformance depends on gaining access to top-quartile managers. How much does this access matter? According to Cambridge Associates, the performance spread between top-quartile and bottom-quartile managers, over time, is a shocking 14%.1 According to Hamilton Lane, 20 years ago there were 1,551 private markets funds. As of September 2022, managers with funds raised in the trailing 10 vintage years are 12,500+ Funds.2

- Portfolio contracting & administration – Investing in private markets requires literal limited partnerships. That fact kicks off a number of legal requirements, such as partnership agreements, private placement memoranda and subscription agreements. These each require intense legal review and require investors to be able to negotiate side letters - addressing issues such as key-man clauses, fees, terms and other complex issues. And once these partnership documents are signed and executed, there are still likely to be numerous partnership amendments. For many investors, these legal burdens quickly become too cumbersome, making it vital that they work with a solutions provider with deep and dedicated legal resources. In addition, private market investing requires intense ongoing data monitoring and engagement. Events like capital calls - when the money an investor commits is called down at key moments in a fund’s life cycle - kick off whole streams of complex activities. Given the unique nature of each investment, benchmarking PM performance is also more nuanced. And proper monitoring includes engagement activities, such as attending mandatory annual meetings and Limited Partner Advisor Committees (LPACs).

- Risk management – Over the last decade, the market capitalisation of private markets has expanded, as have the types of ways to access PM, such as primaries, secondaries and co-investments. Given these developments, along with better access to data, investors are now able to have a clearer picture as to how both public and private market risks are integrated across the total portfolio. This includes cash-flow profiles of different types of investments, mapping scenarios on the impact of different economic environments and rolling up portfolio exposures at the total portfolio, in order to determine desired positioning for future commitments. This also applies to investors who have seasoned private market portfolios, or legacy assets, that may be in wind-down mode but still need to be able to integrate these exposures at the total-portfolio level.

- Operational due diligence – We also believe the best solutions providers will staff a separate operation team outside of the investing function - one that performs due diligence on potential private market managers’ back offices. This due diligence will look at valuation policies and fund structures, and will perform reputational research. Why? Efforts like this can provide private markets investors with an additional layer of governance and reputational risk management.

The bottom line

The lower-return environment is real and unavoidable. Whether or not it’s navigable is another matter. We believe your money needs to work as hard and as smart as it possibly can. The private markets category is too powerful of a tool not to consider. But with great power comes great responsibility - great enough to demand a total-portfolio approach. Choose to bring along a strategic partner with a holistic understanding of this high-potential space.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice

1 Source: Cambridge Associates All Private Equity, Venture Capital, Growth Equity and Buyouts, Mezzanine and Distressed, years from 1981 – 2017. Returns shown net of fund fees and expenses. Returns shown through 2017 because in the early life of a fund, IRR may not be meaningful as the fund is still in the investment period and therefore IRR does not truly reflect performance of the fund. Returns for more recent fund vintages may be lower than the returns shown above and IRRs are more likely to be negative. For illustrative purposes only. The returns shown above correspond to alternative investment products managed by third-party managers. They do not represent the actual investments of the Fund, Russell Investments or any of its other clients. Past performance is not indicative of future results