The 15/35/50 Retirement Lifestyle Rule

The majority of working life is spent saving earnings for retirement. But Russell Investments research shows that investors will only save 15% of their investment pot during their working years. Developing an investment plan is therefore crucial to keep the portfolio growing, even after retirement.

The 15/35/50 Retirement Lifestyle Rule

Regular savings and market growth are important for building a retirement nest egg. But, continued investment growth after retirement can be crucial in helping maintain or even improve the funded ratio (the value of total assets compared to future spending needs). This has become increasingly more important against today’s low interest rate environment and rising life expectancies.

At Russell Investments, we believe that pension pots can be divided into three distinct parts:

- 15% from money saved during working years

- 35% from the investment growth realised before retirement

- 50% from investment growth that occurs during retirement

A post-retirement asset mix

The key is having the right portfolio asset mix in place at retirement and during retirement — one that balances the general stability of bonds with the continued growth potential of equities. The Russell Investments 15/35/50 Retirement Lifestyle Rule is all about striking a post-retirement asset mix that offers the potential to generate strong and steady cash flow for the rest of an investor's life. As unique investment outcomes change during retirement, it is also important to regularly revisit the portfolio asset mix.

Managing risk while planning for growth

When it comes to designing an effective retirement portfolio, there are three primary risks to consider:

- Market volatility

If the market declines, the portfolio value will be affected. To address this risk, it often makes sense to move into more conservative investments as retirement approaches.

- Longevity risk

Many people underestimate their true life expectancy. If an investor's portfolio does not continue to grow during retirement, they could run out of money.

- Sequential risk

The timing of the move from accumulation to decumulation can be crucial to the long-term health of an investment portfolio due to the importance of the sequence of investment returns. Poor returns early in retirement are much more harmful to an investor’s retirement prospects than poor returns later in retirement. The more equity oriented a portfolio, the larger the potential impact of sequential risk.

With the right portfolio asset mix and the skill of professional fund managers, the risk of market volatility can be reduced whilst still potentially earning the growth and long-lasting income required. The Russell Investments 15/35/50 Retirement Lifestyle Rule can help explain the various components of retirement income.

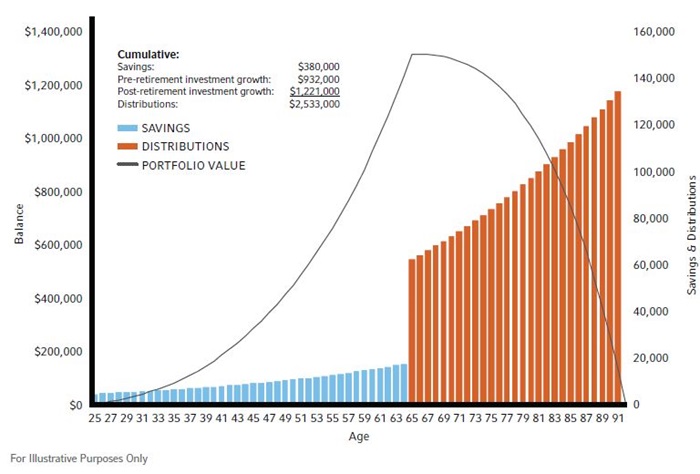

The power of growth after retirement

Example:

Paul starts saving for retirement at the age of 25 by contributing 6% of his annual $65,300 salary. His company’s defined contribution plan provides a 50% match, which means his employer contributes another 3% of his salary.

Over the next 40 years, he receives an average 3.5% annual salary increase, and continues to make annual contributions to his plan. At 65, Paul begins to withdraw from his retirement savings — starting with 4.7% of the portfolio value the first year and increasing this rate by 3% (expected rate of inflation) each year until age 91. Paul is able to withdraw more than $3.2 million during retirement.

Paul’s case illustrates the Russell Investments 15/35/50 retirement lifestyle rule in action:

- Only 15% of Paul’s total retirement income came from his cumulative contributions of $380,000

- 35% of Paul’s total retirement income came from cumulative investment growth of $932,000 that occurred before he turned 65

- $1,221,000 – a whopping 50% – of Paul’s total retirement income came from cumulative investment growth that occurred after retirement

- Paul’s total distributions between 65 and 91 were $2,533,000

Making pension pots last a lifetime

Regardless of an investor's stage in life, the fundamentals of investing remain the same. Work with a professional investment adviser. Take advantage of market performance. And consider multi-asset investing, which can help diversify portfolio risk.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.