Why was 2017 one of our best trading years ever?

We asked Jason Lenzo (Director, Equity, Fixed Income and FX Trading team) and Chris Adolph (Head of Transition Management EMEA) to reflect on the exceptional year that Russell Investments’ trading desk had in 2017. Here they discuss the factors that contributed to the success.

Jason - 2017 was a record year of trading for Russell Investments. Where has that growth come from?

It certainly was a record year with $2.5 trillion of trading, up 20% on 2016 and “Top Global Broker” for the second year running. Not only was the total amount traded our highest ever, but the majority of asset classes traded record amounts, too. Up 36%, currency trading led the way at over $1 trillion. Securities trading was up over 16% to $184 billion and derivative trading was up 6% to over $910 billion.1

What lies behind this growth in currency trading?

The 36% growth in currency trading volumes is a good barometer of the underlying heath of our implementation capabilities as a whole. Growth across the board contributed to 2017’s record FX and trading numbers, for example:

- The volume in our third-party Foreign Exchange (FX) business – i.e. where external clients use us as their FX broker – was up 85%

- Average FX spot transaction costs for the year were less than 0.5 bps, an approximate 87% saving on what the average asset manager achieves2

- Third-party FX overlays increased by nearly 30%

- Other derivative overlays grew by 11% to $45 billion while direct investments grew 35% to $42 billion – together seeing a 14% increase to FX trading

- The total value of assets transitioned was up over 10% to $723 billion which contributed to a 30% increase in the amount of FX traded

Average FX spot transaction costs for the year were less than 0.5 bps - an approximate 87% saving on what the average asset manager achieves

The Global Broker award3 is a huge achievement; can you expand a little more on this?

Yes, it really does highlight the value-add that we bring on the execution side and is a real credit to the performance of the whole trading team. The award relates to an annual survey conducted by Institutional Investor and it’s the second year running we have won it. What’s particularly pleasing is that the survey is not just across our principal competitors in the implementation business, but across the whole of their universe, covering over 2,000 brokers and 1,300 asset managers worldwide. Furthermore, it identified us as achieving a +35 basis point price improvement relative to the average in their universe. The unique value proposition is that we are positioned to access the global markets directly around the world efficiently and with investment discipline and this delivers real savings to clients.

What do you believe is behind the trading results Russell Investments achieve?

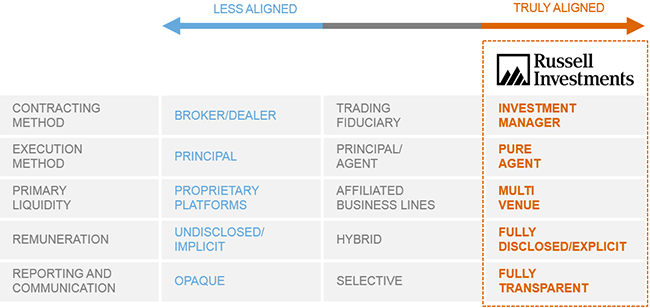

There are a number of areas that differentiate our trading capabilities and these are illustrated in the exhibit below, but three key areas are:

- We are registered as both a broker dealer in the market and as investment manager. This “dual” registration allows us to access exchanges and markets efficiently and directly, but at the same time allows us to deal in markets only accessible to investment managers such as particular crossing networks.

- We are an agency only firm, so we are always working on behalf of our clients. This means we are trading for our clients exclusively, and never trading against them, as can a dealer or a proprietary firm.

- Finally, the last area of excellence is our global reach born out of long experience over time.

All these factors come together with a very experienced team to deliver these results consistently.

What precisely is dual registration and what impact does this have on our trading capabilities?

Dual registration means we have registered the trading as both an agency-only broker dealer AND an investment manager. This structure allows our firm to access the broadest range of markets, trading venues, and networks, bringing the market together onto a single trading desk. It’s very much a story of aggregating a market that is very fragmented today to reduce spread and market impact.

Russell Investments' business model

Our “pure agency” business model is at the core of all our execution capabilities and is a key differentiator from our competitors.

Acting in a fiduciary capacity is becoming increasingly important, but costs are still a primary driver for clients. How does Russell Investments’ unique approach to trading reduce costs?

Fiduciary is an often-discussed word globally and can have a variety of legal definitions depending on jurisdiction. At Russell Investments, we view this as a duty of loyalty and a duty of care. In order for us to provide this, we need to trade and execute in a manner we feel has the highest likelihood of achieving best execution for our clients.

We need to understand both the drivers of the investment decision and the expected costs of implementation. Integrating this information into the investment decision is a key part of that duty of care and loyalty that sets us apart and also allows for efficient implementation. We are constantly evaluating execution quality, utilising third party execution measurement, and comparing our execution results against a variety of peer universes.

The peer universes are comprised of a variety of types of asset managers, broker dealers and market participants, which we feel gives us a good backdrop against which to measure our execution quality. The results prove that we have got the structure right and are accessing the markets and venues efficiently as agent for our clients.

How do you validate trade execution quality in more opaque asset classes like fixed income?

This is a great question, and really highlights the tenacity of the team looking to measure execution efficacy and also comparing with a universe of peers and market participants. In the opaquer asset classes like fixed income, data and information can prove very difficult to access, and to measure.

We have identified and purchased fixed income trading and execution data, as well as a peer universe against which to measure our trading. The stated goal is to measure the execution in the market at point of execution, as well as measure the trading results versus a variety of material peer universes. We can use this information not only at the asset class trading level (in terms of overall quality of execution over time), but also at the individual program level for transition events. This continues to support our value proposition around our execution quality and measurement of an incredibly opaque market but also is best practices for governance and oversight.

What key developments do you see in 2018 and beyond?

As indicated in the stellar growth of our third-party FX business, increased regulatory demand coupled with resources constraints have contributed to an increasing demand for asset owners and managers alike, to outsource some (and in some cases, ALL) of their trading capabilities. Russell Investments offers not only a broad platform with proven trading capabilities across a multitude of asset classes to respond to these needs, but delivers this within a fiduciary wrapper.

1 Source Russell Investments; all AUM numbers in this answer are as at 31 December 2017 and stated relative to 31 December 2016. Traded amounts are for the full year of 2017.

2 Source: Russell Investments. Costs calculated using day’s average rate method: comparison of exchange rate to average of the day’s high and low rates. Costs from 2016 Study on Asset Manager Trading Costs.

3 Institutional Investor, December 2016 – based on full-day VWAP annual data to 30 June 2016.