Market

Outlook

Market

Outlook

Three-scenario problem

Markets at mid-year 2024 are priced for a no-recession soft landing in the U.S., but mixed data signals are delaying central bank rate cuts. This creates some risk of a harder landing in late 2024/early 2025.

2024 Global Market Outlook – Q3 update

Markets are pricing in a no-recession soft-landing. We think there is a good chance of a soft-landing, but the delays to central bank rate cuts means there is still the risk of a harder landing later in the year or in early 2025.

Hi, I’m Andrew Pease and I’m the Chief Investment Strategist for Russell Investments. Welcome to the third quarter update of our 2024 global market outlook.

There is still no clear answer to this year’s key question: is the United States’ economy headed towards a no, soft or hard landing.

We think that “no landing” where the economy re-accelerates and inflation rises is the least likely outcome, and that the signs of slowdown in the economic data mean the debate is now mostly between a soft landing or a recession.

Financial markets are backing the soft-landing scenario. This is evident in the optimism around earnings-growth expectations and in high-yield credit spreads that are pricing cyclically low levels of defaults. Soft landings are rare after big Fed tightenings and the argument for getting one this time is that because of Covid and the lockdowns, this cycle is so different that the normal rules don’t apply.

The case for a recession is the old rules will eventually apply, but it’s just taking longer this time. The U.S. economy has never previously avoided recession after such a sustained period of restrictive monetary policy. In fact, the resilience of the economy potentially makes the hard-landing more likely by delaying the timing of Fed rate cuts.

Although we think that a soft-landing is possible, we worry that markets are underappreciating the risk of a mild recession. This creates an asymmetry in the return outlook. There is some return upside if soft-landing expectations are correct, but a potentially significant drawdown if a recession happens.

We’re seeing better economic conditions in most other developed economies as they catch-up from relatively lacklustre post-Covid economic growth outcomes. Europe is being boosted by the upturn in global manufacturing and a resurgence in bank lending growth. Japan is also getting support from stronger global manufacturing and is being helped by the weak yen. The United Kingdom is finally seeing some better growth indicators, but persistent inflation is delaying Bank of England rate cuts.

The China outlook is also brightening as a result of policies to stabilize the property market and boost the economy. China faces longer-term structural issues related to high savings, low consumption, over-capacity, and a reliance on export demand. The policy moves, however, have boosted the near-term outlook and have helped Chinese shares bounce from deeply oversold levels earlier in the year.

Let’s turn to our asset class outlook

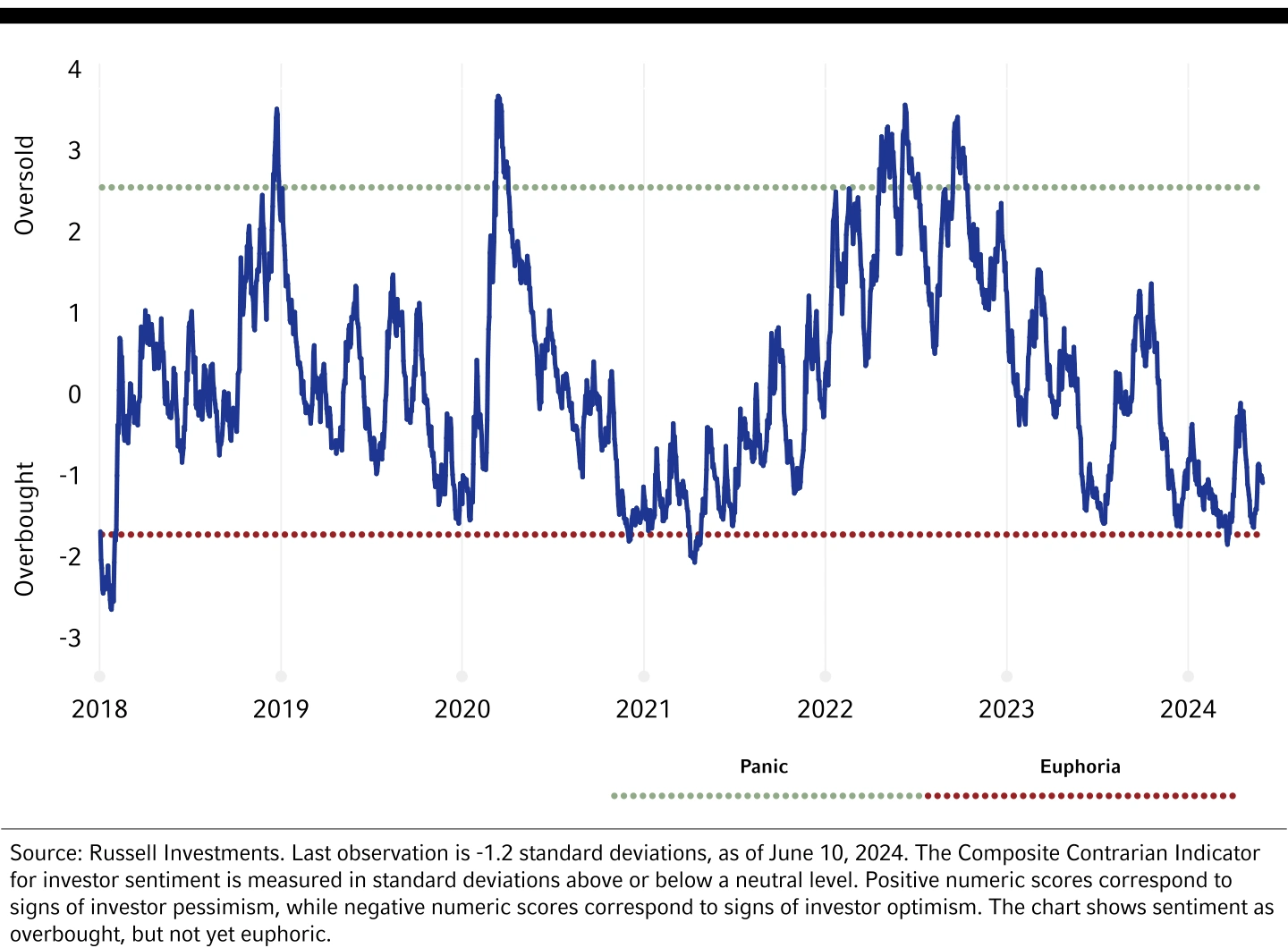

We assess the market outlook through our Cycle, Valuation, and Sentiment investment decision-making framework. The soft versus hard landing debate means the cycle remains uncertain, and valuations for risky assets such as equity and corporate credit are expensive. Government bonds, however, are attractively priced across most developed markets. Finally, our investor sentiment indicator shows that market psychology is optimistic but not at an extreme of euphoria that would warrant a strong risk-off stance in our portfolio strategies.

We’re not currently seeing strong tactical opportunities across equity regions, sectors or styles. The value factor, small caps, financials, and emerging markets offer good value, but the return asymmetry means our equity strategies are generally neutral and emphasize stock selection as the main driver of risk and return in portfolios.

The expected decline in borrowing costs from central bank rate cuts should create a tailwind for listed real estate due to its interest-rate sensitivity.

We’re neutral on most major currencies with the greenback looking expensive and the yen particularly cheap on a purchasing power parity basis.

We like the yields offered by private credit, although picking the right manager is critical. Within real assets, we expect commercial real estate values to bottom out in 2024 and we think that the sustainable energy transition should continue to support demand for base metals.

This year has become a three-scenario problem for investors. Our view is that the no landing is unlikely, the soft landing is possible, and the hard landing is more probable than priced by markets. Soft-landing expectations are likely to persist over the next few months as inflation concerns decline. The asymmetry in the return outlook, however, means we will be watching closely for signs of a deeper downturn.

Thanks for watching, please take a look at the full market outlook report, and we will talk to you again soon.

Andrew Pease

Chief Investment Strategist

“Just as last year’s investor pessimism was overdone, we worry this year’s optimism could eventually prove to be excessive.”

- Andrew Pease

2024 Global Market Outlook: Q3 update

Three-scenario problem

There is still no clear answer to this year’s key question: is the U.S. economy headed toward a no, soft or hard landing? We see plausible reasons why any of these scenarios are possible.

What are the different outcomes for the U.S. economy?

The reacceleration (no-landing) case is supported by above-trend jobs growth, double-digit expectations for corporate earnings growth and inflation that remains stuck above 2.5%.

The potential for a soft landing or a period of below-trend growth is backed by the slowdown in forward-looking labour market indicators. These include hiring rates, the cooling in wages growth that will depress real household incomes, and signs of distress from low-income consumers indicated by rising default rates on credit cards and auto loans.

The case for a hard landing (recession) relies on historical precedent. The U.S. Federal Reserve (Fed) has embarked on the most aggressive tightening since former Fed Chairman Paul Volcker’s tenure in the early 1980s, and the yield curve (10-year minus 2-year) has been inverted since mid-2022. This is a classic recession warning sign: the U.S. economy has never previously avoided recession after a sustained period of restrictive monetary policy.

No landing seems the least likely outcome. There is enough evidence that the economy is slowing and inflation pressures are easing. Households have exhausted their pandemic excess savings and the 2023 fiscal boost from the federal government’s Inflation Reduction Act of 2022 has turned into an economic drag. The recent uptick in six-month annualised measures of core inflation is, in our view, more noise than signal and we expect the ongoing moderation in wage growth will eventually return inflation to the Fed’s 2-2.5% comfort zone.

Is the U.S. economy headed for a soft landing or a recession?

The main debate is between a soft landing or a recession. The economic data aren’t much help as the slowdown signs can be read as either a healthy rebalancing that allows inflation to cool without triggering negative growth, or the pathway toward a mild recession beginning later this year or early 2025.

The case for a soft landing is that this cycle is so different that the normal rules do not apply. The inflation spike was mostly due to demand recovering more quickly than supply following the Covid-19 pandemic. In contrast to previous Fed tightening episodes, households and the corporate sector did not overborrow, and have been protected from Fed rate hikes by locking in low rates on 30-year mortgages and longer-term corporate bonds. Tight Fed policy has been less painful than usual, which has allowed the economy to slow gradually and bring down inflation without triggering a recession.

But it could also be a case of this time is longer rather than this time is different. The soft landing could overshoot into at least a mild recession. In fact, the resilience of the economy potentially makes the hard-landing more likely by delaying the timing of Fed rate cuts.

Are markets underappreciating the risk of a mild recession?

Financial markets are backing the soft-landing scenario. This is evident in the optimism around earnings-growth expectations and in high-yield credit spreads that are pricing cyclically low levels of defaults. We think both scenarios are possible, but that the market is underappreciating the risk of a mild recession. This creates an asymmetry in the return outlook. There is some return upside if soft-landing expectations are correct, but a potentially significant drawdown if a recession occurs.

Conditions are improving in most other developed economies as they catch up from relatively lackluster post-Covid gross domestic product (GDP) growth trajectories. Europe is recovering from near-recession conditions in 2023, jointly boosted by the upturn in global manufacturing and a resurgence in bank lending growth. Japan’s GDP growth was surprisingly subdued over the first quarter of 2024, but the near-term outlook is more promising with support from improving manufacturing activity and the weak yen. The United Kingdom is experiencing a modest improvement in growth indicators, although persistent inflation is delaying the timing of Bank of England rate cuts.

The China outlook is also brightening as a range of policy measures are being implemented to stabilise the property market and boost the economy. China faces significant longer-term structural issues related to high savings, low consumption, over-capacity, and a reliance on export demand. The policy moves, however, have boosted the near-term outlook and have helped Chinese shares bounce from deeply oversold levels earlier in the year.

This year has become a three-scenario problem for investors1. Our view is that the no-landing scenario is unlikely, the soft landing is possible, and the hard landing is more probable than priced by markets. Soft-landing expectations are likely to persist over the next few months as inflation concerns decline. The asymmetry in the mid-year return outlook, however, means we will be watching closely for signs of a deeper downturn.

GDP growth since the COVID-19 pandemic

“The no-landing scenario is unlikely, the soft landing is possible, and the hard landing is more probable than priced by markets.”

- Andrew Pease, Chief Investment Strategist

Artificial intelligence growth debate

Beneath the market hype around artificial intelligence (AI) there has been an important debate about the impact AI will have on productivity and economic growth. On the skeptical side is Economics Professor Daron Acemoglu at the Massachusetts Institute of Technology, who thinks the cumulative boost to U.S. GDP over the next 10 years will be not much more than 1%. This compares with optimistic predictions from analysts at McKinsey & Company and Goldman Sachs who argue that the cumulative increase in GDP could be as high as 7% (or nearly US$2 trillion in inflation-adjusted terms). The International Monetary Fund published staff notes in January that stated AI has the “potential to reshape the global economy”.

Long-term GDP trends are determined by the growth in the working-age population and productivity (i.e., output per unit of input). Ageing demographics mean current GDP growth trends can only be maintained with rising productivity. The growth optimists see green shoots from the potential exponential advances in artificial intelligence.

How much could AI potentially boost GDP growth by?

AI is already resulting in cost-structure improvements for some firms. For example, computer programming and coding groups have reported dramatic increases in productivity. These are still early days for large language models2, and we should not forget that the virtual assistant ChatGPT was released just 18 months ago in November 2022.

The gap between the skeptics and optimists is largely about the proportion of tasks that can be done by AI on a cost-effective basis. Professor Acemoglu believes this is quite low. We’re more optimistic given the early indications of efficiency gains in certain industries, and the speed at which improvement is occurring. Additionally, the benefits of AI will likely lead to reallocation of labour and new tasks, rather than simply being a cost-saving measure.

The two useful historical analogies are the introduction of electricity and the early days of the internet. Both technologies eventually resulted in about a one percentage point per year boost to productivity, consistent with the optimistic range of AI forecasts.

This has several implications. First, an increase in potential growth should lead to a higher equilibrium interest rate (r-star). Second, absent changes in taxation and distribution policy, a boost in productivity through AI should favor capital over labour, meaning that corporate profit margins should be supported. Third, it increases the fair value range for equity markets by supporting margins and increasing the potential for longer-run earnings-per-share growth.

“The benefits of AI will likely lead to reallocation of labour and new tasks, rather than simply being a cost-saving measure.”

– Alex Cousley, Director, Senior Investment Strategist

U.S. growth forecasts anticipate soft landing

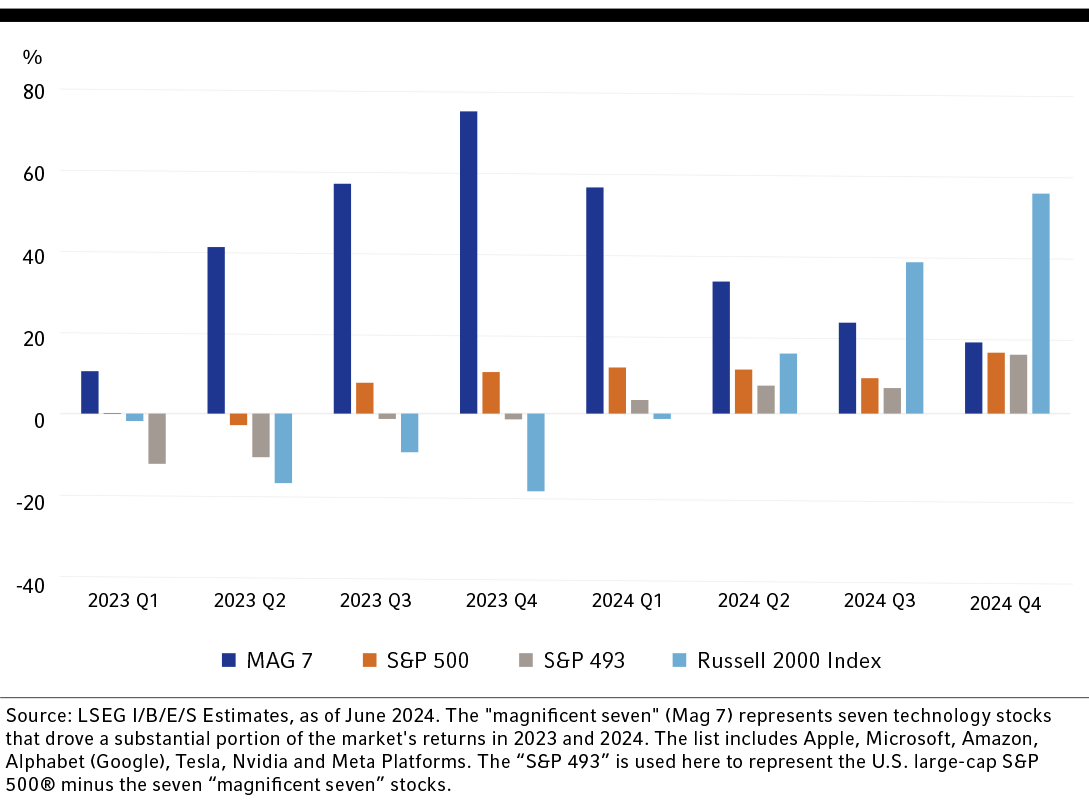

U.S. companies recorded respectable earnings in Q1 2024. S&P 500® earnings grew by around 11% year-over-year, stronger than in the prior quarter. Once again, Magnificent Seven companies played a key role, growing earnings by more than 50% year-over-year. By contrast, earnings-per-share (EPS) growth for the S&P 493 (S&P 500 excluding Magnificent Seven) was near 3% year-over-year. Nevertheless, this was an important quarter for the S&P 493, as it marked the beginning of an earnings recovery. As the year progresses, industry analysts expect that S&P 493 EPS growth will increase, while the Magnificent Seven companies decelerate.

What’s the earnings outlook for small-cap companies?

U.S. small-cap companies (see chart below) have been hit harder than their large-cap peers by sensitivity to higher interest rates but showed tentative signs of stabilisation in the first quarter. Russell 2000® Index earnings growth was close to flat year-over-year, versus negative growth rates in 2023. Industry analysts expect a sharp rebound in small-cap earnings, with earnings growth rates reaching more than 50% year-over-year by the end of the fourth quarter of 2024.

We think these consensus expectations are too optimistic. They could be correct if the soft landing eventuates (our base case scenario), but we still see a 35% probability of a recession over the next 12 months. A recession would see earnings contract by 10-15% year-over-year.

The consensus optimism might be correct if the no-recession soft landing eventuates. However, there is little scope for further upgrades, and this potentially places a ceiling on how much further U.S. equities can rally.

Earnings-per-share (EPS) growth rate for publicly listed U.S. companies

“Our base-case scenario is that a soft landing eventuates, but we still see a 35% probability of a recession over the next 12 months.”

– BeiChen Lin, Director, Investment Strategist

Regional snapshots

United States

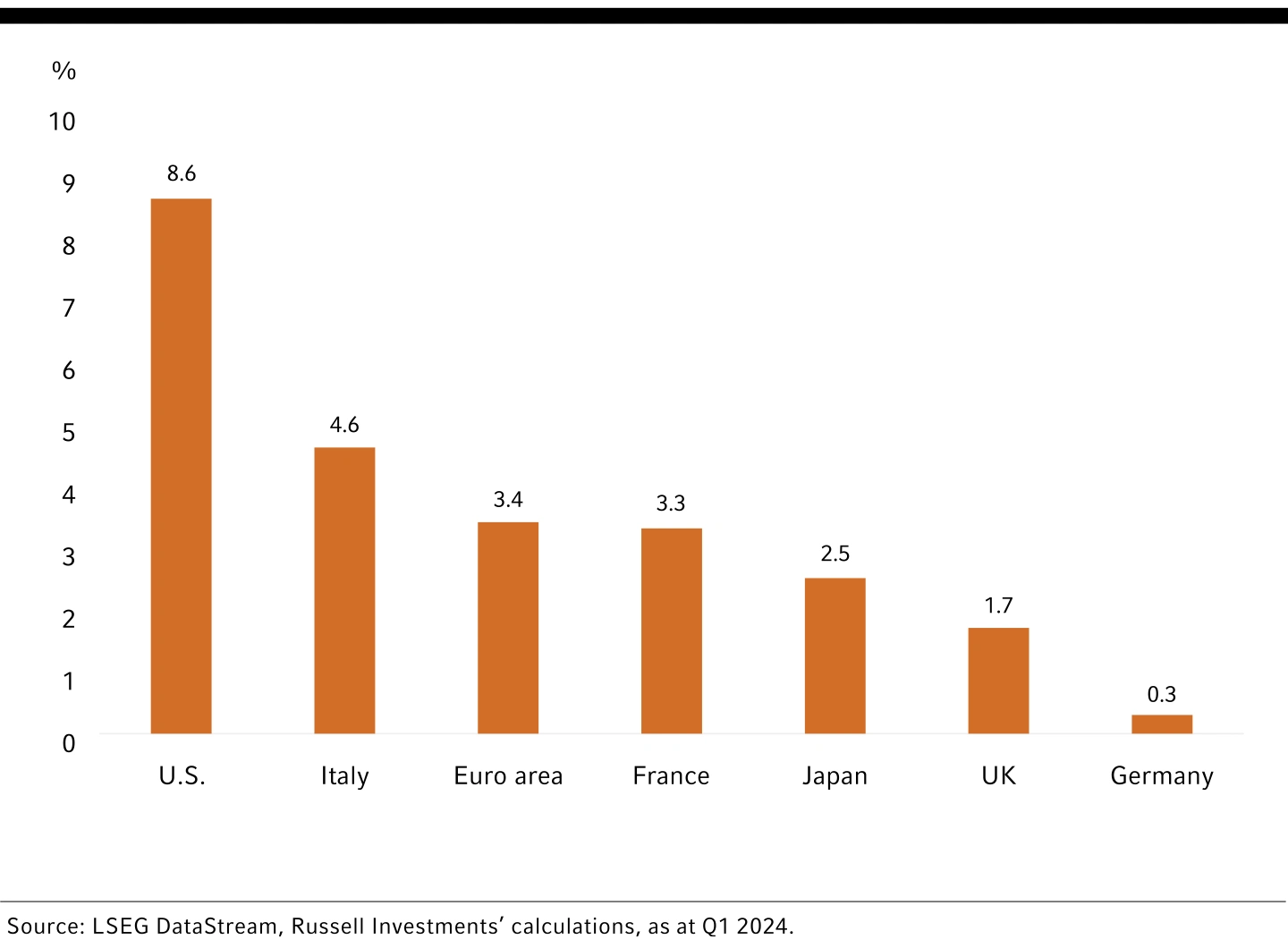

The U.S. economy at mid-year 2024 is on firmer footing. The labour market has painlessly rebalanced back to 2019 levels–strong but no longer overheated enough to generate significant inflation. Core personal consumption expenditures (PCE) inflation has moderated to 2.6% from a cycle-high of 5.6% and appears on track to drop toward the Federal Reserve’s goal next year. On the back of this progress, we expect the Fed to start carefully cutting rates later this year, with September the likeliest timing for the first move. Corporate earnings were robust in Q1 with growth led by the Magnificent Seven. Importantly, we also saw profits stabilise for the broader large-cap S&P 500 and small-cap Russell 2000 indices in the period.

We think it is more likely than not that the U.S. economy can avoid a recession in the year ahead, but macro uncertainty is high. The Fed has exhibited reversion aversion, demanding a high bar on the inflation data to kick off rate cuts. This leaves some risk that the gradual slowing in the cycle could extend into a downturn. Markets are priced for the expected soft landing but without the uncertainty and humility around this outcome that we also see. Equity valuations are expensive and credit spreads are tight. Our proprietary measure of market psychology shows investor optimism, but it is not at extreme levels of euphoria at mid-year that would warrant a sharp risk-off posture. Treasury yields remain extremely volatile into the combination of choppy data and a data-dependent Fed. We see good value in bonds over the medium-term; both in terms of their starting real yield and as a diversifier to more adverse economic scenarios.

Eurozone

The outlook for the eurozone economies continues to brighten as industrial activity picks up, bank lending growth improves, and inflation tracks toward the European Central Bank’s (ECB) comfort zone. The ECB delivered its first 25-basis-point (bps) rate cut in early June and the market anticipates a further 100 bps of easing over the next 12 months.

The recent European parliamentary elections have generated some political turmoil due to the success of right-wing populist parties. The decision by France’s President Emmanuel Macron to call an election in the national assembly (where the government is formed) has created fears that one of Europe’s largest economies could soon be governed by the far right. This has helped trigger a near 4.5% sell-off in eurozone equities as investors worry about the prospect of unfunded tax cuts against the backdrop of high government debt levels. These fears seem overdone, however. France’s two-stage electoral process means a far-right win is not assured. Furthermore, the example of Italian Prime Minister Giorgia Meloni shows that European populist parties can behave responsibly once in power.

We believe European stocks are attractively valued relative to U.S. stocks and can rebound once the political drama subsides and as earnings expectations are upgraded in line with improving economic conditions.

United Kingdom

The UK outlook is beginning to improve, albeit from a low base. Consumer and business confidence are rebounding and there are signs that house prices are beginning to recover. Core inflation, however, is proving sticky, and at 3.9% is preventing the Bank of England from signalling near-term rate cuts. Interest rate markets have priced 100 basis points of Bank of England (BoE) easing over the next 12 months, which seems realistic given inflation should get closer to the BOE’s 2% target over the next year.

Prime Minister Rishi Sunak has called an election for July 4, which current public opinion polls indicate is set to be resoundingly won by the Labour Party led by Keir Starmer. The Labour Party is running a cautious campaign, promising that there will not be substantial changes to taxation and government spending.

The FTSE 100 Index is relatively attractive with a 12-month-ahead price-to-earnings ratio of 11.4 times and a 3.5% dividend yield. UK gilts are attractively valued with a 10-year yield at 4.1%.

Japan

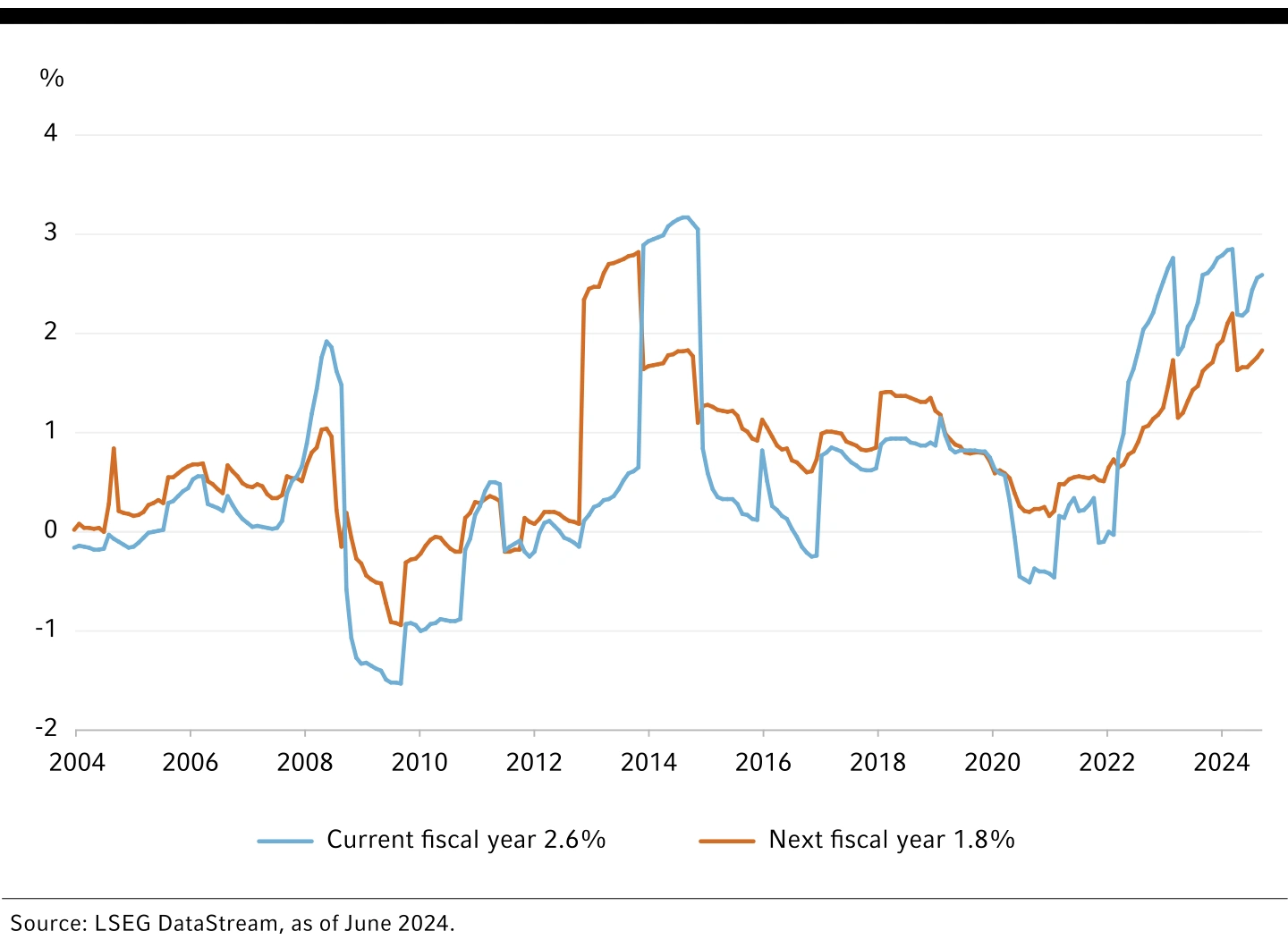

Japan is the land of rising inflation expectations, after having experienced more than 20 years of near-zero inflation. The chart below shows professional forecasters are expecting inflation to be close to the Bank of Japan’s (BoJ) target next fiscal year. In March, the BoJ raised interest rates for the first time in 17 years and seems likely to raise rates further, albeit in a patient manner. The economic outlook looks decent, with manufacturing picking up and the China outlook becoming more supportive. The depreciation in the Japanese yen is supporting inbound tourism.

Japanese government bonds look unattractive on valuation, especially given rising inflation expectations. Japanese corporate earnings are expected to be robust, although equities have priced in a lot of good news. The Japanese yen screens as one of the cheapest G103 currencies but will only likely strengthen when the interest rate differential between the U.S. and Japan starts to narrow.

Core inflation forecasts: Japan

China

Chinese policymakers have become more forceful in trying to turn the nation’s property market around. They have effectively created a program that will allow local governments to purchase excess inventory in different cities. The size of this pilot program is not large, but we think this shift in the stance of policymakers is an important turning point in China’s economy. We expect it will be expanded should it prove successful.

Additionally, Chinese corporates have become more focused on governance and shareholder returns. For years, Chinese equities have suffered from dilution i.e., companies issuing more shares. We have seen an increase in buyback announcements, which will allow better economic activity to flow through more meaningfully to earnings per share. Chinese equities continue to look cheap relative to broader global and emerging market equities.

There are still risks on the horizon for China. There could be tensions with the U.S. in the leadup to the November federal government elections. There is also the risk of more aggressive action from the European Union following the dramatic growth in electric vehicle exports to Europe. These risks, along with the upcoming Chinese government plenum4 in July, need to be closely monitored by investors.

Canada

The Canadian economy has avoided recession as population growth has supported consumption and, in turn, GDP growth. However, the persistent increase in the unemployment rate (from a low of 5.4% to 6.2% over the past 12 months) and the greater than 3% contraction in the per-capita GDP since the second quarter of 2022 both indicate the economy has been weaker than the headline GDP suggests.

Given that backdrop, it makes sense that the Bank of Canada (BoC) was the first G7 central bank to ease policy, cutting its target rate by 25 bps to 4.75%. We see the potential for three additional cuts this year, so long as the disinflation trend continues. Our path for the BoC is slightly more dovish than the industry consensus view, but that's also because we are somewhat more concerned about the economy. While a recession in Canada is no longer the consensus outlook, we believe the risk of the Canadian economy slipping into a recession over the next 12 months remains above average.

Given our macroeconomic views, we maintain a positive outlook for government bonds, which are likely to benefit from economic turbulence, while being cautious about the outlook for Canadian equities.

Australia and New Zealand

Australia remains on the narrow path of avoiding recession. The consumer is under stress from the increases in the Reserve Bank of Australia’s (RBA) cash rate and variable rate mortgage interest rates. Consumer spending has slowed materially. Tax cuts will start on 1 July. It is unlikely that all the increase in disposable income will be spent, but it may provide some support, particularly to lower-income consumers. Improvement in Chinese economic activity will also be supportive.

The inflation pulse in Australia lags the rest of the world by about six months (due to a later reopening from the pandemic lockdowns), and so the RBA will likely lag major central banks to reduce rates. Our current base case is for a cut in November, but there is growing risk that the RBA may stay on hold until early 2025.

New Zealand’s economy has contracted in three of the last four quarters, illustrating the pressures that the economy is facing following the aggressive action from the Reserve Bank of New Zealand (RNBZ). The outlook remains challenging, with credit growth still soft and a large current account deficit. Despite the unemployment rate having risen more than 1% from its low, wage pressure has not abated yet. This leaves the RBNZ in an uncomfortable position. We expect that the RBNZ will commence cutting rates after the U.S. Federal Reserve.

“European stocks are attractively valued relative to U.S. stocks.”

- Andrew Pease

Asset-class preferences

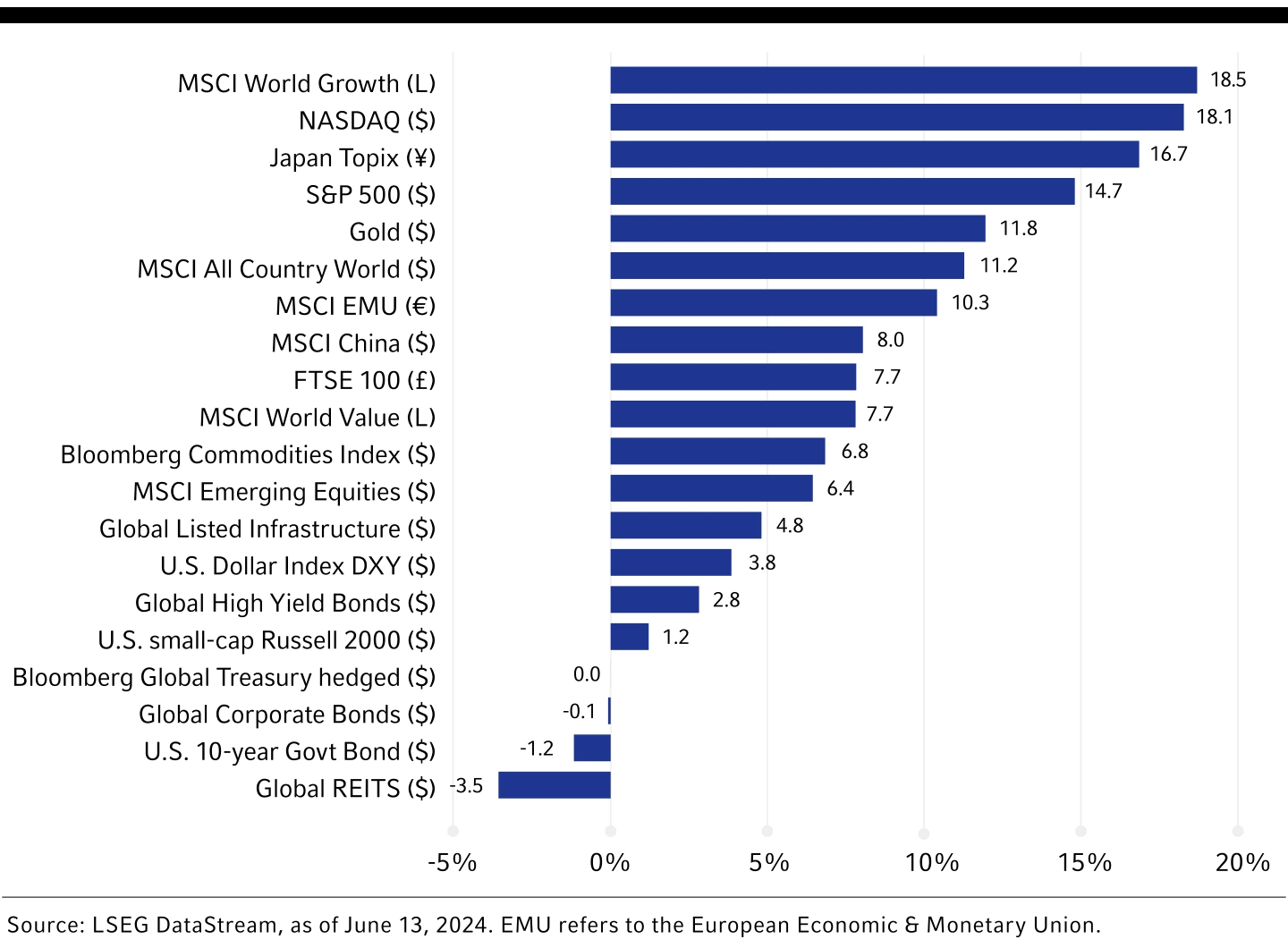

Global equities delivered solid returns in the first half of 2024 with those gains once again spearheaded by U.S. mega-cap growth stocks. Dispersion within the Magnificent Seven and across the broader equity market remains high, however. NVIDIA continued to shine with strong demand for its computing technology, particularly graphics processing units, propelling a blockbuster earnings report and stock performance in the period. Meanwhile, smaller companies – which tend to be more exposed to interest rates via short-term and variable interest rate borrowing – have faced stiffer headwinds from the Federal Reserve’s restrictive monetary policy. The U.S. small-cap Russell 2000 Index went sideways in the year to mid-June, trailing U.S. large-cap performance by a wide margin.

Volatility in fixed income markets remains high as data-dependent central banks were met with volatile – and at times discordant – inflation and growth data. Sovereign yields rose sharply through mid-April as hotter inflation figures in the United States delayed the expected timing of Fed rate cuts. Softer growth and moderating inflation more recently caused a U-turn lower in yields with markets now expecting a September rate cut from the Fed, following similar moves in June by the European Central Bank and Bank of Canada.

Asset-class performance, year-to-date through 14 June

What’s the business cycle outlook?

We assess the market outlook through our cycle, valuation, and sentiment (CVS) investment decision-making framework. The cycle remains highly uncertain. Economies operating at full employment with inverted yield curves suggest we are late cycle. But resilient growth, improving corporate earnings, disinflation, and expected central bank rate cuts leave the path to a soft landing open. Valuations for risky assets such as equity and corporate credit skew expensive, particularly in the United States, where investors are pricing in a soft-landing scenario with high confidence. Meanwhile, government bonds look attractively priced across most of the developed markets, with high real yields and diversification potential should a more adverse economic scenario materialise. Finally, our sentiment indicator shows market psychology is optimistic but not at an extreme of euphoria that would warrant a sharply risk-off posture in our portfolio strategies.

COMPOSITE CONTRARIAN INDICATOR:

MARKET SENTIMENT IS OPTIMISTIC BUT NOT AT EUPHORIC EXTREME

While our CVS framework skews somewhat cautious – suggesting some potential downside asymmetry for stocks and corporate credit – we do not see the current setup as being an unsustainable extreme that would warrant a significant deviation away from our long-term strategic asset allocation. Our portfolio strategies are generally emphasising diversification into high macro uncertainty and emphasising security selection as the primary driver of active return.

Our asset class preferences as of mid-2024 include:

- We do not see extreme tactical opportunities across equity regions, sectors, or styles. Cheaper segments of the equity market include the value factor, small cap, financials, and the emerging markets. But most of these exposures carry higher betas 5 in a period of elevated uncertainty. As a result, our equity strategies are generally neutral and emphasise stock selection as the main driver of risk and return in portfolios.

- Government bonds are attractively valued. We think many developed market sovereigns offer good carry with real yields at their highest levels in decades and the potential for double-digit returns in a recession scenario. Credit spreads are historically tight for both investment grade and high yield corporates, leaving an unattractive risk-reward profile for multi-asset investors.

- With central bank rate cuts kicking off in parts of the developed market, the expected decline in borrowing costs should create a tailwind for listed real estate due to its interest-rate sensitivity. Meanwhile, net operating income (NOI) growth has remained healthy, as supply is still tight in some markets. Listed real estate and listed infrastructure valuations are more attractive than equities, making them a notable diversifying asset for a balanced investment portfolio. While we are cautiously optimistic on the U.S. economic outlook, risks remain. Listed infrastructure’s low downside capture can help buffer portfolios should equities sell off. OPEC+’s extension of its oil production cuts, along with heightened geopolitical tensions, create a floor for crude oil prices. But oil prices may also be constrained by lackluster demand as the global economy transitions toward a period of below-trend growth. Gold has been buoyed by geopolitical tensions and central bank purchases, but stretched valuations relative to real interest rates, combined with reports that the People’s Bank of China paused gold purchases in May, may result in downside risk to gold prices going forward. The global transition to sustainable energy should support healthy demand for base metals.

- We are neutral on most major currencies, with the US. dollar looking expensive and the Japanese yen particularly cheap on a purchasing power parity basis over the medium-term.

- Private markets have demonstrated resilience, particularly in midst of rising costs of capital and the uncertainty stemming from a year filled with several national elections. However, a considerable amount of unrealised value remains in the market and distributions to paid-in capital continues to be low as a weak exit environment has challenged many sponsors. While the proliferation of continuation vehicles is expected and will continue to be a source of proceeds for investors in private equity, we anticipate some transactions will come under increasing scrutiny in a more contested valuation environment. Higher interest rates are forcing management teams to be more creative and focus on operational value-add to drive outcomes. Yields on private credit remain attractive; however, elevated macro uncertainty suggests that choosing private credit funds with robust asset management capabilities remains critical. Within real assets, commercial real estate values are expected to bottom out in 2024 with gridlock between buyers and sellers addressed, in-part, via debt maturities.

“Our portfolio strategies are generally emphasizing diversification into high macro uncertainty and emphasizing security selection as the primary driver of active return.”

- Paul Eitelman, Senior Director, Chief Investment Strategist, North America

Prior issues of the Global Market Outlook

1 The Three-Body Problem in physics shows that the motion of three objects cannot be predicted: https://en.wikipedia.org/wiki/Three-body_problem.

2 Large language models are deep-learning algorithms that can recognize, summarize, translate, predict, and generate content using very large datasets.

3 The G10 consists of eleven industrialized nations that meet on an annual basis or more frequently, as necessary, to consult each other, debate and cooperate on international financial matters. The member countries are Belgium, Canada, France, Germany, Italy, Japan, the Netherlands, Sweden, Switzerland, the United Kingdom, and the United States.

4 In China, a plenum refers to a meeting attended by all full and alternate members of the Communist Party’s Central Committee. Typically, there are seven plenums between party congresses, which occur once every five years.

5 The term 'beta’ is used in finance to denote the volatility or systematic risk of a security or portfolio compared to the market.