$20 billion club strategy series – Benefits policy

Executive summary:

- Benefits policy is one of the key levers a plan sponsor can pull to impact a plan’s outlook. This can range from very minor tweaks to the plan’s benefit formula, to major adjustments that close the plan to new hires or freeze the plan’s accrual for existing participants

- Over the past decade or so, there has been a broad trend in the industry toward closing and freezing defined benefit plans.

- Closing and/or freezing a defined benefit plan will inherently reduce the risk that the plan poses the plan sponsor, due to the reduction in future uncertainty associated with benefit accruals for active participants.

Today we continue our series on the $20 billion club strategy. For the uninitiated, the $20 billion club is a group of pension plans with more than $20 billion of global pension liability. We have been reporting on this group for the last 13 years, following how and why their funded status has changed over time and reporting on how these sponsors’ strategies for managing risk have evolved over time.

While we encourage you to read the first article to see what these mega-plan sponsors are working through in their investment policies, there are some key points worth reemphasizing. This series of blogs is for addressing the major levers that plan sponsors can pull to impact the trajectory of their large defined benefit (DB) plans. These three broad levers are often closely intertwined and pulling one lever can lead to adjusting another. The three key levers are:

- Investment policy - This lays out how those contributions go to work for the sponsor

- Benefits policy - This directly impacts plan participants’ benefit accruals

- Funding policy - This determines the contributions made by the sponsor to pay for those benefits

In the first blog of the series, we took a look at the investment policy of these mega-plans. Today we’ll be reviewing the benefits policy of the $20 billion club and what we might glean from the recent history of these mega-plans. The benefit policy is one of the key levers a plan sponsor can pull to impact the plan outlook. This can range from very minor tweaks to the plan’s benefit formula, to major adjustments that close the plan to new hires or freeze the plan’s accrual for existing participants.

During the past decade or so, there has been a broad trend in the industry toward closing and freezing DB plans. The reasoning behind this approach is myriad, complex, and non-linear. Regulations, funding hurdles, and workers’ preference toward benefits can be cited, but there is no single item that is the root cause. When the Pension Protection Act of 2006 (PPA) was passed, the DB landscape changed dramatically. While the resulting changes significantly increased protections for participants, the same changes increased the cost, governance, and burden on pension plan sponsors.

Since then, large DB plans have been on the decline, both in plan count and participant count. Total participant count is down more than 33% from 2006 to 2021, according to the Pension Benefit Guaranty Corporation (PBGC) data tables. This takes place through closing, freezing, and the subsequent natural attrition as participants leave the plan through cash out or pass away but this can be accelerated by executing pension risk transfers. This is no different for the $20 billion club plans that have altered plan design by closing plans to new entrants and, in many cases, freezing benefit accruals altogether, followed by small to large pension risk transfers.

Like many of the trends we are bringing to light in this series, this has come up in the $20 billion club before and it is no surprise that it has continued in the past few years. Closing and/or freezing a DB plan will inherently reduce the risk that the plan poses the plan sponsor due to the reduction in future uncertainty associated with benefit accruals for active participants. This, in turn, has an impact on the investment policy, which we detailed in the previous blog in this series. Exhibit 1 details some notable activity in this space over the past few years.

Exhibit 1: Notable activity 2021-2023

| UPS | Full freeze of 70,000 non-union participants became effective in 2023, as announced in 2017 |

| AT&T | 2023 $8.1B group annuity contract purchase |

| IBM | 2022 $16B group annuity contract purchase |

| Lockheed Martin | 2021 $4.9B and 2022 $4.3B group annuity contract purchases |

| Pfizer | 2022 $0.5B group annuity purchase |

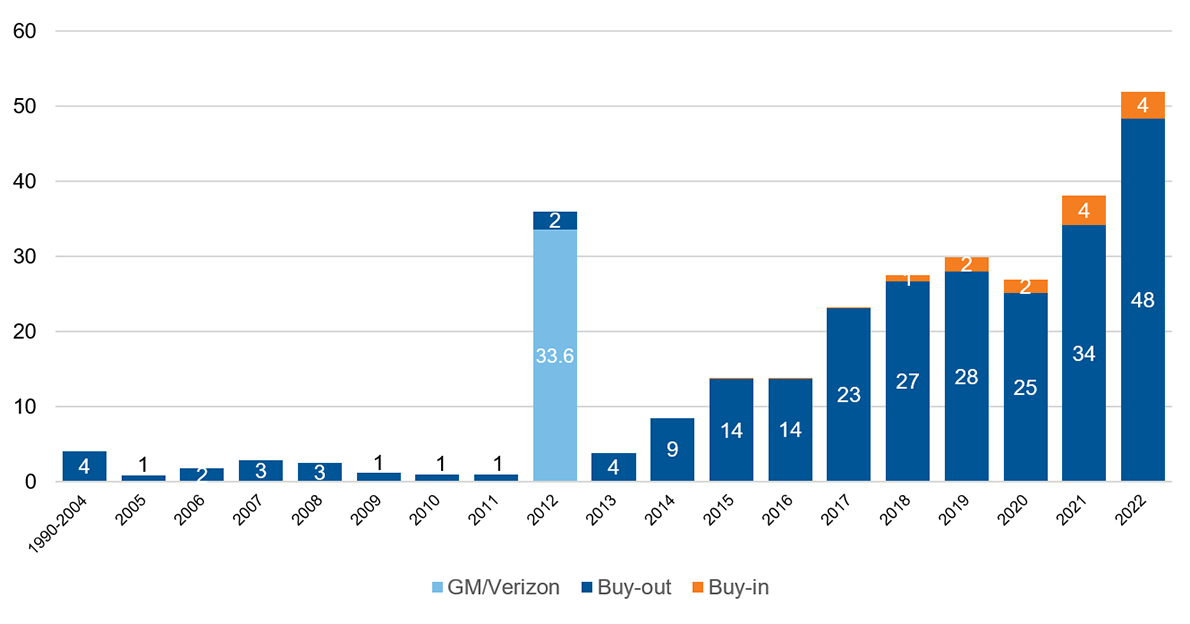

The IBM risk transfer was an especially noteworthy move by the company, being the second largest annuity purchase to date at $16 billion. Second only was the unprecedented 2012 General Motors annuity purchase of a momentous $25 billion, which arguably kicked off the high pace of annuity purchase risk transfer we see in the industry today.

Exhibit 2: Annuity purchase history

Source: LIMRA Secure Retirement Institute.

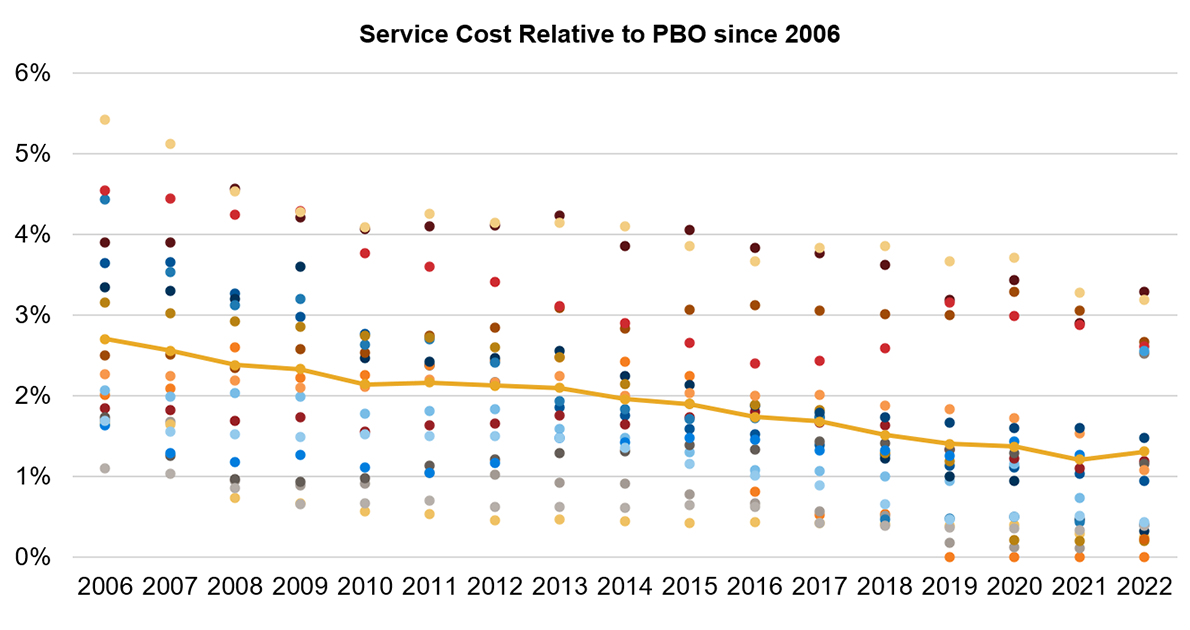

While the UPS freeze was announced several years ago, it’s worth noting that of the $20 billion club members, UPS had the highest service cost relative to PBO in 2022, a key metric when considering open and closed plans. UPS was one of only two plans where this ratio was above 3% in 2022 with Johnson and Johnson being the other. This freeze to their non-union participants will decrease this ratio going forward. With UPS in mind, let’s look more broadly at this key metric.

As a way of further illustrating the trend of pension plans closing and freezing, we can look at the size of service cost relative to PBO across the $20 billion club. The service cost for a pension plan represents the annual cost associated with new benefit accruals for active participants. For an established and open plan, the service cost relative to the PBO will be consistent as active participants accrue benefits and inactive participants exit the plan through mortality (or otherwise). This ratio of service cost to PBO is generally between 3% and 5% for an open plan.

However, there has been a broad trend of plans closing to new entrants (soft-freeze) and freezing benefit accruals altogether (hard-freeze) for several years. For a soft-frozen plan, this ratio will decrease over time and will be 0% for a hard-frozen plan. Exhibit 3 illustrates the move of closing and freezing plans since PPA was passed in 2006 through the decline of service cost to PBO. In 2006, the service cost ratio among these companies ranged between 1.1% and 5.4%. In 2018, the range had dropped to between 0% and 3.3%, with an average decrease of about 1.6% since 2006.

Exhibit 3: Service cost relative to PBO since 2006

Source: SEC Form 10-K filings.

With the uptick in pension risk transfers, which focus on non-accruing participants (i.e., they have no service cost), it would be reasonable to expect that the service cost relative to PBO would increase as the PBO shrinks. However, even as plans have executed lump sum offers and annuity purchases, the ratio of service cost to PBO has continued to drop over the past few years, further emphasizing the impact of closing and freezing.

It would be fair to point out that this ratio on average did not decrease in 2022 for the first time since we began tracking this metric more than a decade ago. This is partially due to the restructuring of the $20 billion club membership, which we comment on below. However, looking at Exhibit 3, we have started seeing diverging paths even within the $20 billion club members. The plans with higher service cost relative to PBO have been relatively flatter, or at least have a slower decline, than those plans now at the bottom of this exhibit that continue their steady trend toward zero. Similar to UPS previously mentioned, many of these freezes were implemented years ago and are continuing to come to fruition or have over the past few years. This is something we will continue to track.

What does this all mean for your DB plan?

As mentioned in our investment policy blog, one of the main goals of the $20 billion club has always been to help plan sponsors understand how industry trends have been developing. Not all plans are created equal, and we focus on these largest plans because they have access to the most sophisticated service providers and the latest innovative strategies. They also tend to have experienced experts on staff that can focus a large portion of their time on their DB plans. Gathering and examining what these jumbo-sized plans have been implementing and adjusting, both reactively and proactively, helps not only to observe the current trends, but also to provide unique insight into where the industry may be heading.

As we’ve mentioned, the different levers available to plan sponsors are often intertwined but the industry trend on benefits policy has been one that has leaned into closing and freezing plans and executing risk transfers. This reduces the overall risk of the plan through a shorter in-plan duration and the ability to lock things in when fully funded through hibernation as well as other concepts; however, there are considerations on how and when to do this. Choosing the right populations to annuitize with an insurer is already an important decision, but are you considering what that will mean for the asset allocation after the fact? Off-loading certain participant cohorts can look appealing at first blush, but the leftover plan can sometimes unintuitively lead to higher average contribution requirements.

At Russell Investments, we are agnostic on whether your plan is open, closed, or frozen; however, each of these plan states has drastically different needs, objectives, and goals. Open plans will inherently have a higher return hurdle rate to keep up with the service cost for actively accruing participants. Frozen plans have a definite timeline as participants leave service through termination, retirement, and ultimately mortality; this means that plan sponsors may want to consider end-game planning and how to approach those specific concerns. Closed but unfrozen plans land somewhere in the middle with unique considerations and timelines. Add a layer of funded status to the mix and things can get complicated fast. We’re here to help with those complications and work through those details whether it be picking the right return-seeking and liability-hedging mix, selecting the equity mix, or helping implement a completion mandate to reduce interest rate risk.

A note on $20 billon club membership

Over the past several years, inclusion in this group of mega-plans could have increased a few times due to falling interest rates, which caused liabilities to soar. However, we have kept this group stable in the past to maintain a certain level of consistency. This past year was an exceptional year in many ways but that has shone through in the DB plan space perhaps more keenly than many other areas. We have used this as an opportunity to refresh the membership of our $20 billion club. The most recent list of 20 companies—many of which have long been members of the club—can be found in our 2023 update.