Executive summary:

- In a stark reversal from the prior two quarters, among Russell Investments Factor Portfolios, Global Large Growth and Momentum outperformed the benchmark for the fourth quarter of 2024 while Global Large Cap Low Volatility, Value, and Size underperformed.

- During the fourth quarter, the decrease in correlations between the Momentum factor and the Low Volatility factor in Russell Investments Factor Portfolios reversed sharply—increasing from -0.6 0 +0.2.

- Using bond returns to refine equity momentum signals showed a premium in long/short portfolios but not in long-only portfolios.

Overview

With an end to the U.S. presidential election and increasing expectations of strong economic growth, deregulation, and lower taxes, the Russell 1000 Index finished the quarter with a robust 2.7% return. Conversely, Developed ex-U.S. Large Cap and Emerging Markets declined by -7.4% and -7.8%, respectively, amid political instability in France and Germany along with uncertainty about the impact of potential U.S. tariffs. This divergence extended to small cap stocks as well, with the Developed ex-U.S. Small Cap Index declining by -7.8% while the Russell 2000 Index increased slightly by +0.3%. The Russell 2000 Index rose sharply in November only to give up those gains in December after the Federal Reserve signaled a slower pace of interest rate cuts.

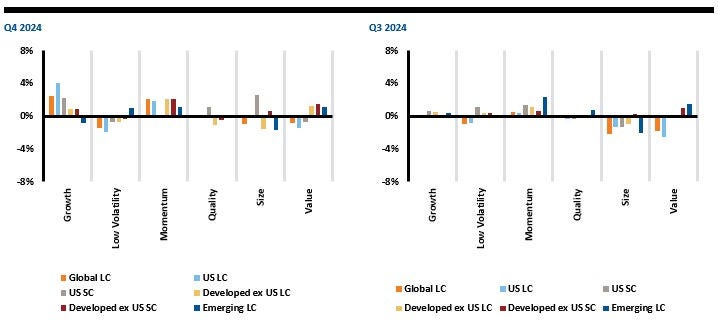

When considering Russell Investments' global factor portfolios (RFPs), Global Large Cap Growth and Momentum outperformed the benchmark for the quarter with positive excess returns of +2.5% and +1.1%, respectively. Conversely, the Global Large Cap Low Volatility, Size, Value, and Quality portfolios underperformed for the quarter with excess returns of -1.4%, -1.0%, -0.8% and -0.2%, respectively. The performance of the factor portfolios in the fourth quarter was a contrast to the prior quarter, where Value and Low Volatility were the outperformers.

Exhibit 1: Cumulative excess returns for Global Russell Investments Portfolios vs. MSCI ACWI

Source: Russell Investments and MSCI; Data as of 10/01/2024-12/31/2024.

Factor performance

Global Russell Investments Factor Portfolios' performance dynamics

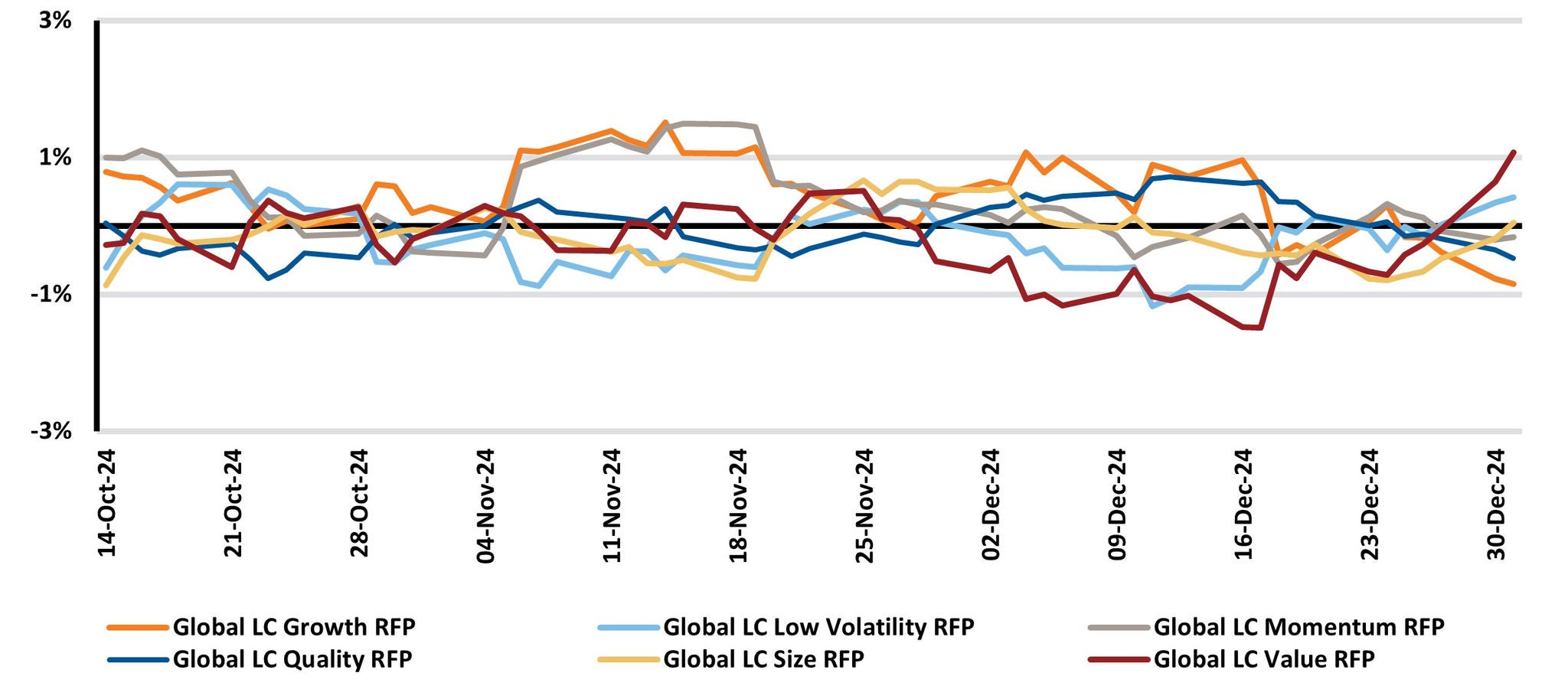

The performance dispersion among Global Russell Factor Portfolios (RFPs) in the fourth quarter was smaller than prior quarters, with dispersions between Value and Growth factors bound to +/-2% for most of the quarter. Growth and Momentum outperformed the market for the majority of the entire quarter, while Value and Low Volatility underperformed before recovering slightly to finish the quarter off their lows.

Exhibit 2: 10-Day rolling excess returns for Global RFPs vs. MSCI ACWI

Source: Russell Investments and MSCI; Data as of 10/1/2024-12/31/2024.

Russell Investments Factor Portfolios' performance across regions

In the fourth quarter of 2024, the performance of the factor portfolios was diverse among U.S and non-U. S. markets in Low Volatility and Value factors but showed uniformity in Momentum and Growth factors. The Momentum factor outperformed strongly across all regions against its respective benchmarks, with excess returns ranging from +0.1% to +2.1%. Similarly, the Growth factor also outperformed across all regions except Emerging Markets, with excess returns ranging from -0.8% to +4.1%.

The Low Volatility factor underperformed its respective benchmarks across all regions apart from Emerging Markets, where it outperformed by +1.0%. The underperformance in Low Volatility was larger in the U.S. in both Large Caps and Small Caps (-1.9%, -0.6%, respectively), where broad markets had positive performance. The underperformance in Developed ex-U.S. markets was not as large, with negative excess returns of -0.8% in Large Cap and -0.3% in small caps.

The Value factor performance was split between U.S. and non-U.S. regions. In the U.S., Large Caps and Small Caps underperformed their respective benchmarks by -1.4% and -0.8%, respectively, while logging positive performances in Developed ex-U.S. Large Cap, Developed ex-U.S. Small Cap and Emerging Markets (+1.2%, +1.5%, +1.1%, respectively). In comparison to the other factors, the performance of the Quality factor across all regions was muted and in a range of -1.0%-+1.1%. The strongest outperformance for the quarter came from the U.S. Large Cap Growth factor with excess returns of +4.1%, while the weakest performance was also in U.S. Large Cap, with the Low Volatility factor underperforming by -1.9%.

Exhibit 3: Excess returns of RFPs vs. corresponding benchmarks

Source: Russell Investments; FTSE Russell; MSCI

Performance of subfactors in the global universe

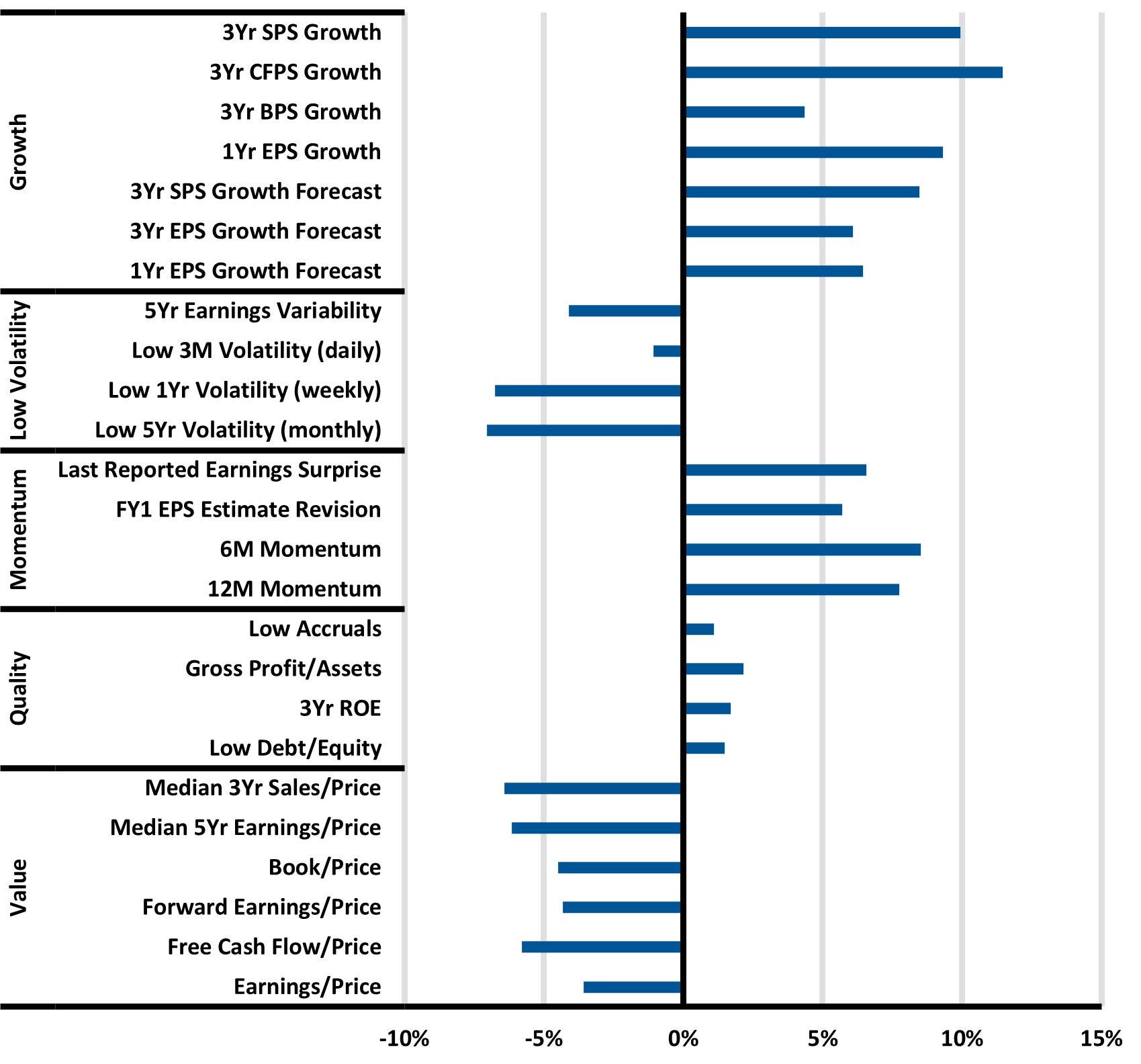

Exhibit 4 below illustrates the performance of various subfactors in the MSCI All-Country World Index (ACWI) universe for the last quarter, represented by top minus bottom quintile portfolios.1 All Growth subfactors had strong positive returns in Q4, reversing a trend from the prior quarter. The largest positive return for the quarter came from the 3-year Cash Flow per Share Growth subfactor with a return of +11.5%. In addition, all Momentum subfactors were strongly positive with returns-based factors—12- and 6-month Momentum (+7.8%, +8.5%, respectively)—performing slightly better than analyst-based factors. All Low Volatility subfactors had a negative return, with 5-Year Monthly Volatility having the largest negative return of the quarter at -7.1%. Similarly, all Value factors had negative returns, with the largest negative return for the quarter belonging to the Median 3-Year Sales-to-Price subfactor, which had a return of -6.4%. Quality subfactors were also positive across the board with all factors, though subdued relative to the strong performance of Growth and Momentum factors.

Exhibit 4: Performance of cap-weighted top-minus-bottom quintiles – Q4 2024

Source: Russell Investments; MSCI; Refinitiv

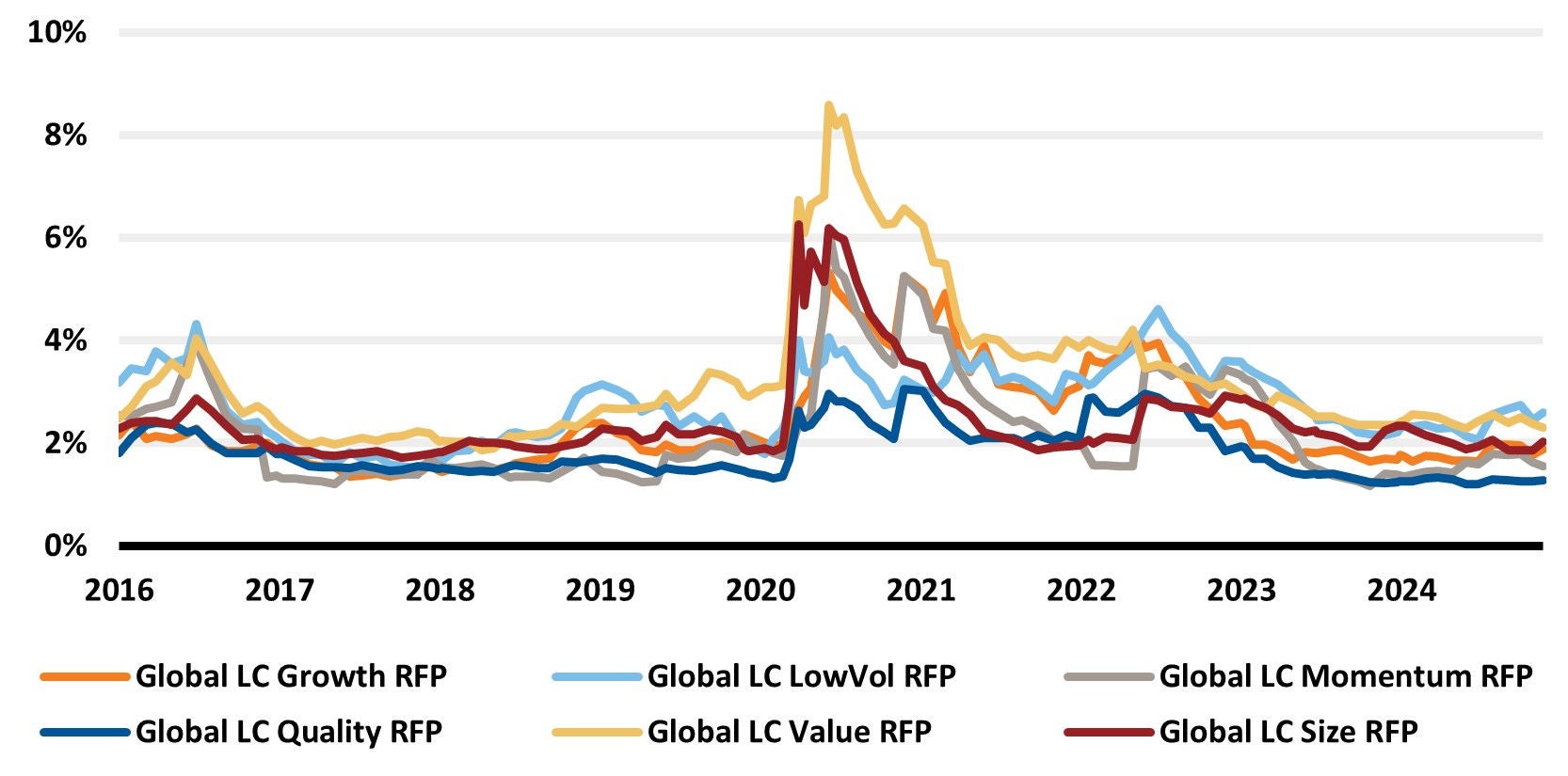

Ex-ante correlations and active risk of Global Russell Investments Factor Portfolios

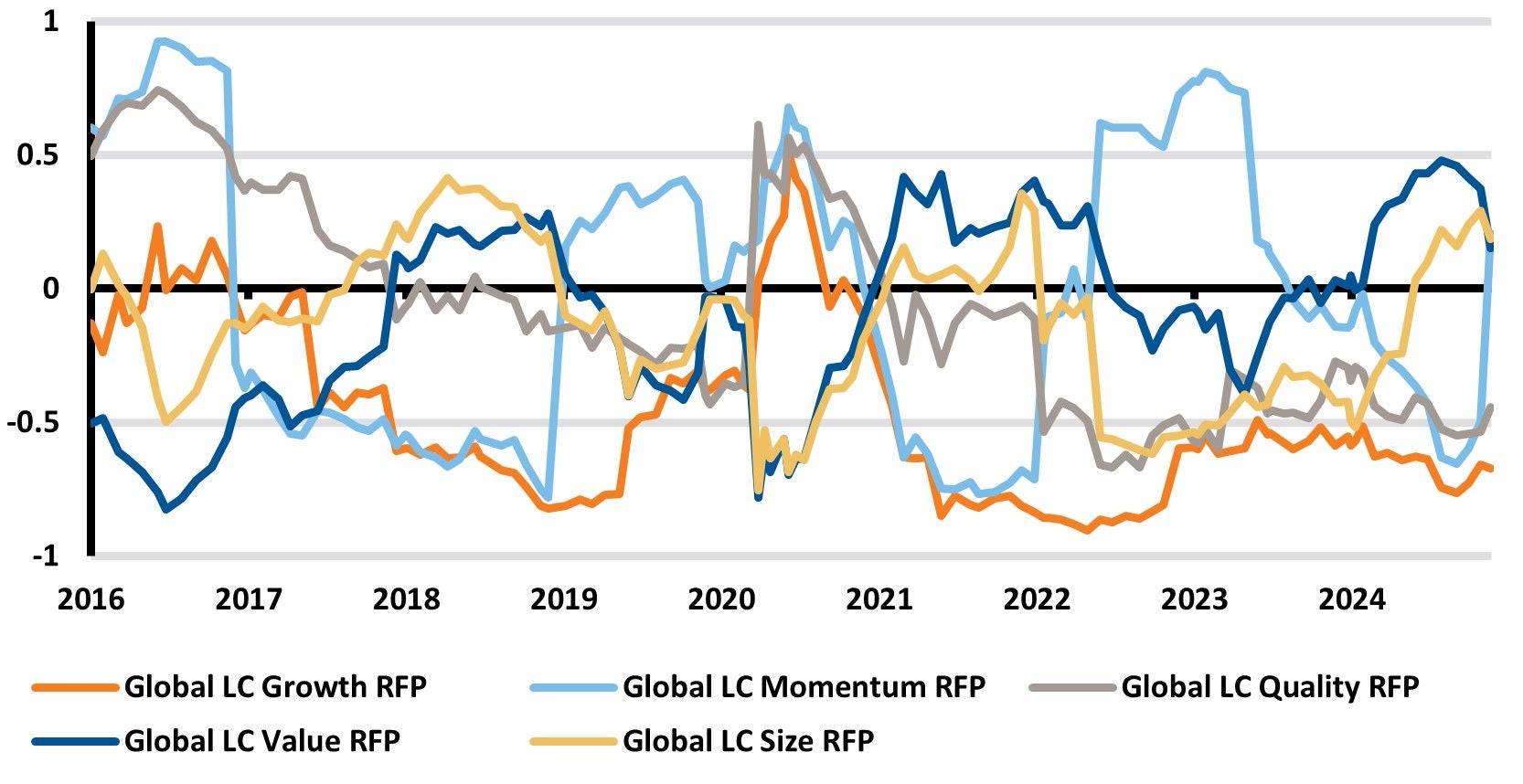

In the fourth quarter, the decreasing correlation between Momentum and Low Volatility reversed sharply over the quarter, increasing from a -0.6 to +0.2. Conversely, the increasing correlations between the Value and Size factors and Low Volatility observed over the past year decreased from recent highs reached in the prior quarter, as illustrated in Exhibit 5 below.

Ex-ante active risk levels—predictive measures of the active risk associated with factor portfolios in Exhibit 6—flattened after displaying a slight trend up over the prior quarter in Value, Low Volatility, and Growth portfolios.

Exhibit 5: Ex-ante correlations with Global LC Low Volatility RFP

Source: Russell Investments; Axioma; MSCI; Data as of 01/2016-12/2024.

Exhibit 6: Ex-ante tracking errors of Global RFPs

Source: Russell Investments; Axioma; MSCI; Data as of 01/2016-12/2024.

Spotlight on: Investigating bond returns for equity momentum signals

Momentum investing is a strategy where assets with strong past performance are expected to continue outperforming in the future, while those with weak past performance are expected to underperform. While this approach is commonly applied to equities using equity-specific data, we explore the potential for bond returns to inform equity momentum signals.

Momentum strategies exploit the tendency of prices to persist into intermediate time horizons, typically three to 12 months. In equities, this phenomenon is well-documented, with factors such as investor herding and slow information diffusion cited as contributing factors. Bonds, however, differ from stocks in key respects, including their payoff structures, sensitivity to interest rate movements, and the influence of macroeconomic factors such as inflation and monetary policy. Despite these differences, bond returns might provide leading information about economic conditions and risk sentiment, which can influence equity prices.

Constructing momentum signals from bond returns

In this report, we investigate whether bond momentum can complement or diversify equity momentum strategies. There are several elements to consider with using this approach:

- There can be multiple issuances of bonds for each issuer, with varying maturities and with different terms and conditions

- A significant portion of a bond's total return is explained by changes in interest rates, and we are interested in capturing the return that is specific to the credit risk of the issuer.

We address the issue of multiple issuances by considering the bond with the closest maturity date at each date of signal creation. If there were multiple bonds with the same maturity date, we chose the bond with the highest coupon rate. While this approach does not fully remove the impact of term spread, it lowers it for each issuer. In addition to removing the impact of interest rates, we use credit returns from Ice/BofA rather than total returns to calculate the momentum signal. Credit returns are in excess of the return of the duration-matched Treasury bill for each security, which removes the term premium and produces the component of return based on the credit risk of the issuer.

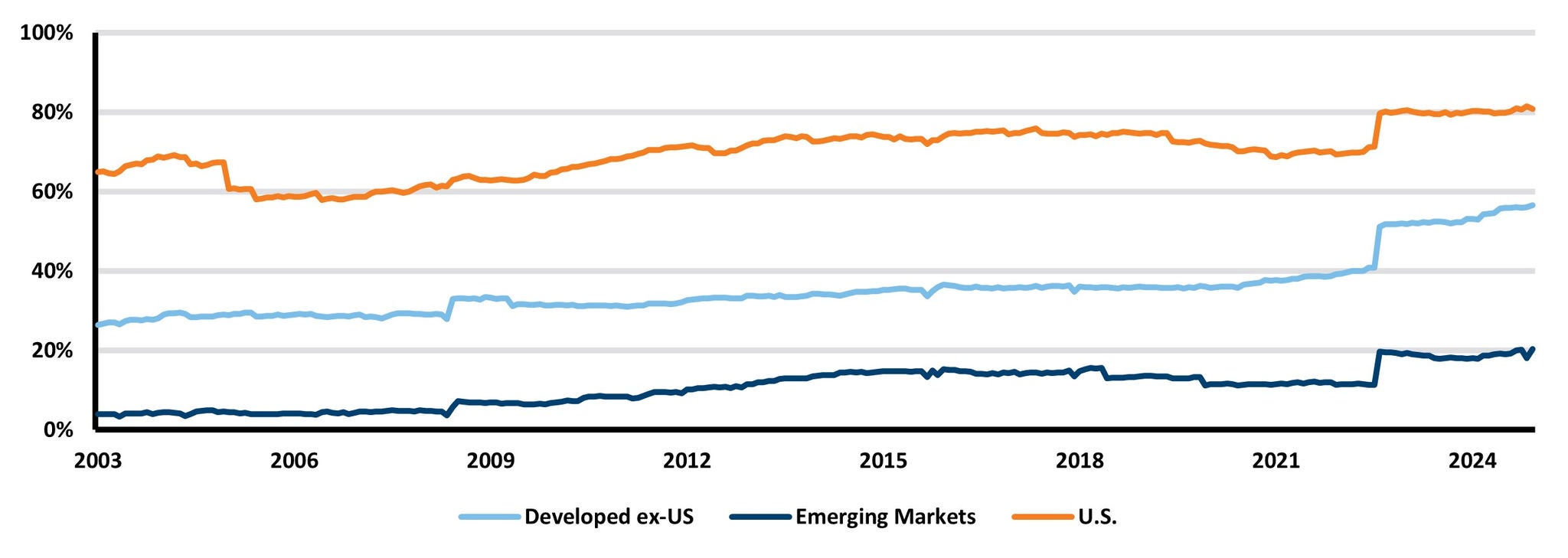

Data

We use the MSCI ACWI Index as the universe of securities and map the constituents using Refinitiv's entity security master to a representative bond. Exhibit 7 shows the percentage of securities in the MSCI ACWI index that are mapped to a representative bond. The U.S. region is well covered, at consistently above 60% of the name count. While the Developed ex-U.S. region coverage has grown over time, it has been below 40% for most of the sample period. The Emerging Markets region has very low coverage at below 20% over the entire sample period. Thus, we exclude emerging markets for the remaining portion of this analysis.

Exhibit 7: Percent of constituents of MSCI ACWI index that have a representative bond (by region)

Source: MSCI, Russell Investments, Refinitv, Ice/Baml Indexes

Analysis

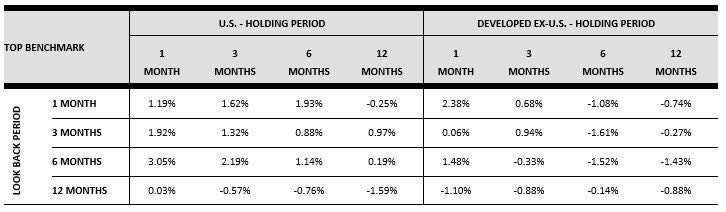

For each security in the universe, using the representative bond, we calculate returns for each 1-, 3-, 6- and 12-month trailing period at each month-end. We than segregate the universe into equal-weighted quintiles that have holding periods of 1, 3, 6, and 12 months for each trailing period. Exhibit 8 presents the performance of top-minus-bottom portfolio returns for U.S. and Developed ex-U.S. markets for each holding and look-back period.

Exhibit 8: Top Minus Bottom Quintile annualized returns (01/01/2003 – 12/31/2024)

Shorter look-back periods of 1, 3, and 6 months—when combined with short holding periods of 1-3 months—show a premium across both U.S. and Developed ex-U.S. regions. The higher premium of 3.1% was in the U.S. region for a 1-month holding period, using a 6-month look-back. The longest look-back period did not have any meaningful excess returns, with the highest return at 12 basis points.

In general, shorter look-back and holding periods tend to provide stronger performance in both markets, while longer look-back and holding periods exhibit diminishing or negative returns.

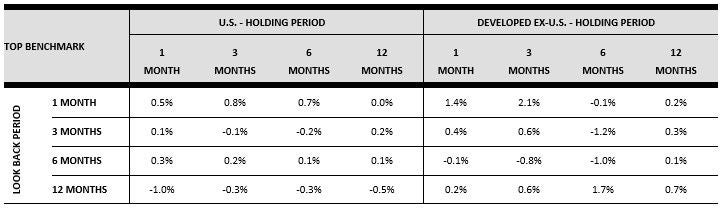

Exhibit 9 presents the long-only portfolio excess of the top quintile vs. the region's respective benchmark. When utilizing a long-only constraint, the large excess returns that we observed in the long/short portfolios disappear. It appears that most of the premium was realized was due to the short position on the equities with the worst performing bonds, rather than a long position on the winners.

Exhibit 9: Top Quintile Minus Benchmark annualized excess returns (01/01/2003 – 12/31/2024)

Implications for Factor Portfolios

While utilizing long-only portfolio construction of bond momentum on equity securities doesn't show promise, the premium observed by shorting the worst performers could potentially still be used by applying an exclusion or underweighting approach to further refine equity momentum signals to realize additional alpha.

1 Top minus bottom cap-weighted quintile portfolios are not investible and are used to proxy the performance of the subfactors used in the construction of RFPs. RFPs are long only portfolios.