Fixed income in 2023: Is a renaissance coming?

Fixed income: shifting macro trends may lead to a rebirth

With 2022 thankfully in the rear-view mirror, the outlook for fixed income has brightened. The global macro trends that created an annus horribilis for fixed income assets last year—inflation and rate hikes—have begun to shift. Our optimism about the potential for positive bond returns is linked to our belief that 2022’s tight monetary policies will lead to declining inflation in 2023. This should allow central banks to suspend rate hikes and potentially pivot to an easing bias.

Fixed income returns in 2022: A year to forget

2022 proved to be the worst year in bond market history with the Bloomberg Global Aggregate Index declining -16.3%.1 A prolonged bull market in equities, a geopolitical crisis in Ukraine, supply-chain issues, loose monetary policy leading up to the pandemic, and the huge fiscal spending packages governments launched to help business and individuals through the pandemic-induced lockdowns, all contributed to the rise of inflation. As inflationary pressures grew, central banks were forced to start implementing unprecedented aggressive rate hikes in early 2022. This drove fixed income returns lower as yields rose and bond prices fell.

As investors we must remember past performance does not guarantee future results. We present the case why this clause perfectly depicts our outlook for fixed income in 2023.

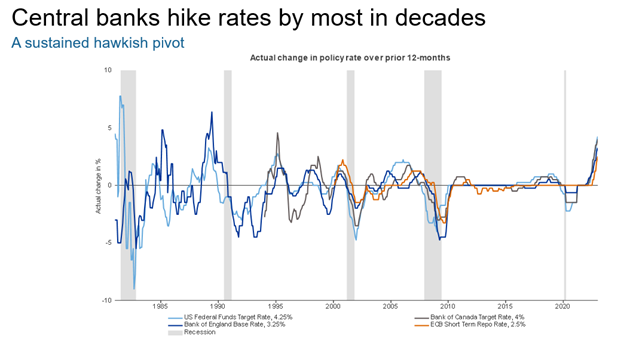

Click image to enlarge

Source: Refinitiv DataStream, Russell Investments. ECB= European Central Bank

Fixed income in 2023: An improving outlook

The risk of a further significant selloff in bonds seems limited, given that inflation may have already peaked and markets have priced in hawkish outlooks for most central banks. Our confidence in the bond market outlook isn’t solely due to the likely decline in inflation and the potential end to the tightening cycle, but also due to the current level of yields. Yields are at multi-year highs in both real and nominal terms, with some high-yield bonds nearing double-digits. These attractive higher yields can help shield investors from the negative impact of further interest rate increases on portfolio returns—we believe these losses would be more than offset by the income from higher yields. In fact, high-quality corporate bonds currently offer higher yields than dividend stocks. As yields on bonds were falling, sometimes moving below dividend yields on stock indices, many investors were forced into higher equity allocations to meet return expectations. This phenomenon became known in the markets as TINA or there is no alternative. Rising rates, however, mean we could be transitioning into the world of TARA—there are reasonable alternatives.

Fixed income poised to reclaim its traditional roles

There are three distinct roles fixed income traditionally plays in a balanced multi-asset portfolio. Now that markets are widely expected to return to their traditional behavior, fixed income should once again provide capital preservation, income and diversification benefits to investors.

CAPITAL PRESERVATION

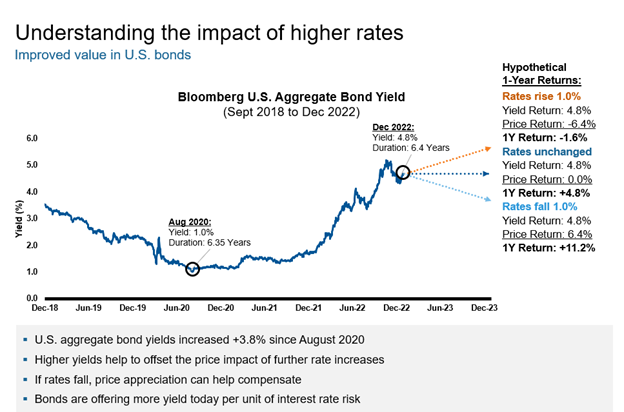

As previously mentioned, we expect inflation to be on a downward trend, providing room for long-term yields to fall. Yields and bond prices move in the opposite direction, therefore a decline in yields results in a rise in bond prices. Expected total returns look quite attractive for bonds in 2023. Even a 1% drop in yields can roughly result in positive double-digit annual returns.

Click image to enlarge

Source: Bloomberg. Data as of 12/31/2022. U.S. Aggregate Bond: Bloomberg U.S. Aggregate Bond Index.

Yield: Yield-to-Worst of the Bloomberg U.S. Aggregate Bond Index. Duration: Modified Adjusted Duration of the Bloomberg U.S. Aggregate Bond Index.

INCOME

The low interest-rate environment that we experienced for almost a decade is behind us and central banks have made that abundantly clear. As yields move higher, investors can look to bonds as a source of stable income. The periodic coupon payments received are essentially an opportunity to get paid while you wait for more stability in the markets.

If the bonds do not default, the price appreciation and income gained from holding these bonds make it quite challenging to disprove the advantages of fixed income in a portfolio. But there is one more benefit we must still cover, arguably the preeminent advantage of holding this asset class this year—diversification.

DIVERSIFICATION

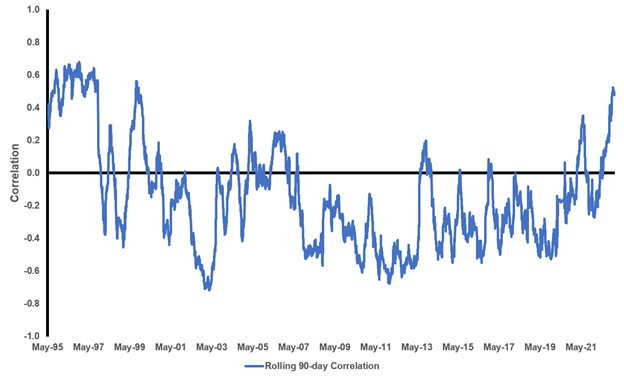

Fixed income is expected to regain its role as a diversifier in 2023 as we believe the relationship between bond and stock price movements will be restored. Much of the pain multi-asset investors experienced last year was due to these two asset classes falling together. We believe the economic downturn will lead to a recession this year and think that will result in a shift back to a negative correlation between stocks and bonds.

Click image to enlarge

Source: S&P 500 TR Index and Bloomberg US Aggregate Bond TR Index. Daily return excludes holidays and weekends. As of December 31, 2022. Correlations measure how two different securities move in relation to each other. Correlation ranges from +1.00 to -1.00. A perfect correlation of 1.00 between two asset classes means they will move

in the same direction, whereas a perfect negative correlation of -1.00 means the asset classes will move in opposite directions. Generally, a number above 0.7 indicates a high degree of positive correlation.

The bottom line

The primary risk to our view would be a resurgence of inflation, which could potentially lead to more rate hikes for longer than currently expected. We recognize there are no guarantees in financial markets, but if we can infer anything from last year’s performance, it is that the revival of bonds should be top of mind. 2022 was a turbulent year—a perfect storm for fixed income investors. However, the forecast has improved. It is premature to think it is smooth sailing ahead but as you position your investments for the year, consider reinstating fixed income as a stabilizer in your portfolio.

1 Morningstar Direct