Fixed Income Q4 Survey 2022: Managers relatively confident on fundamentals, despite the challenging environment

The latest

- The ubiquitous enemy of global markets has been inflation and markets have been right to predict major tightening by global central banks. Have central banks still been too slow to tame inflation? The UK and Europe are still grappling with inflation while economic growth is slowing down. In the U.S., there has been some light at the end of the tunnel, as latest inflation figures moderated slightly in October. However, even there, growth signals are blinking amber. Are markets perhaps thinking that battling inflation will come at a huge economic growth cost?

- The era of loose monetary policy is truly over. Credit markets had been accustomed to low interest rates, but now face headwinds—inflation, higher rates and slowing growth. Are managers seeing any deterioration in fundamentals?

- Emerging markets have not been immune, of course. China's zero-COVID lockdown approach has impacted growth, while also overshadowing its real estate sector. Higher rates in the developed world are also an attractive asset allocation magnet. How are managers perceiving risk appetite in emerging markets?

Battle inflation at the cost of growth?

Views from interest rate managers

- There is no surprise that managers have little belief in the Federal Reserve bringing down inflation to its 2.0% target in the near term. The majority of respondents expect it to remain above 2.5% over the next five years.

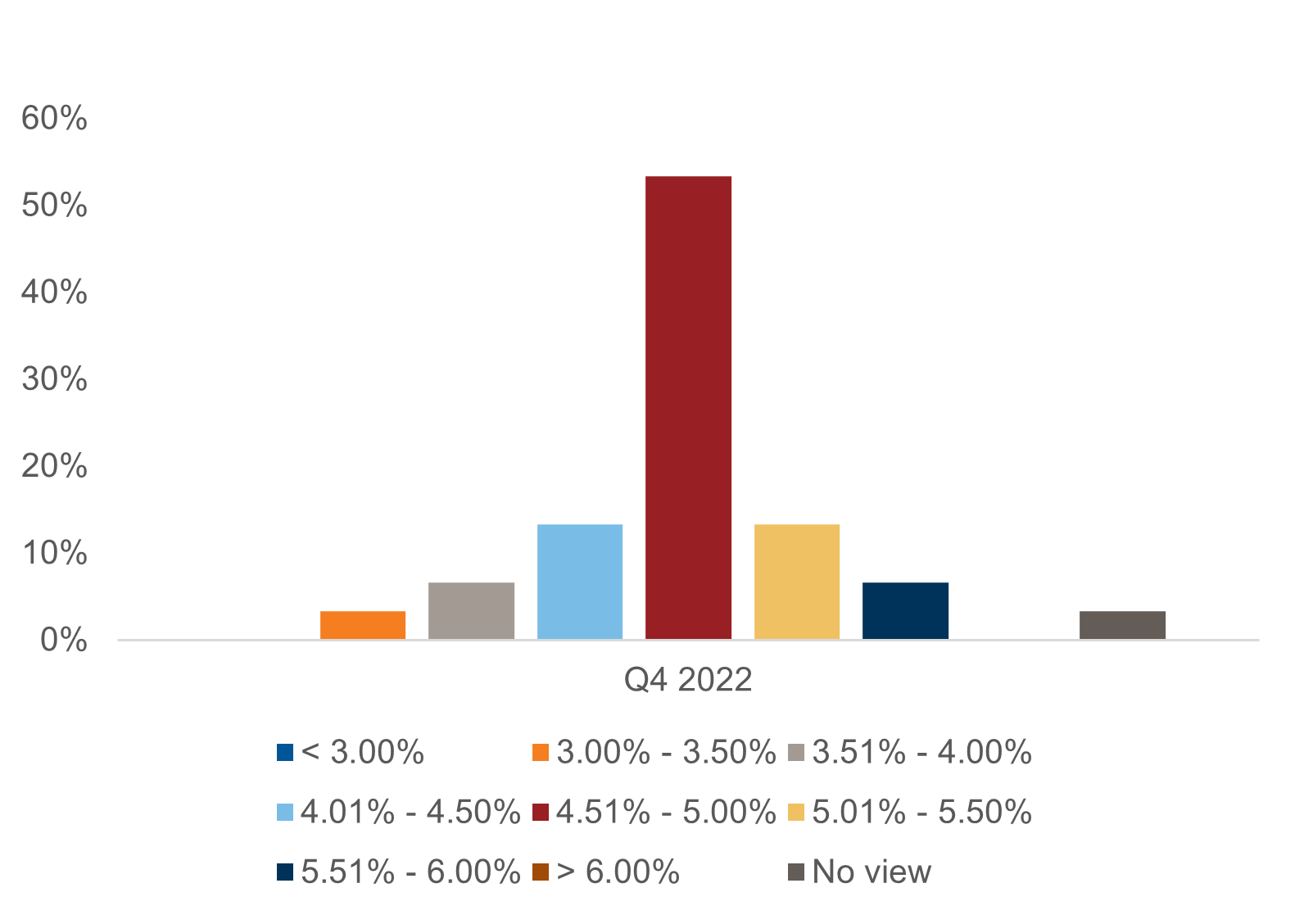

- Over half of investors (53%) expect the U.S. 10-year Treasury yield to trade between 3.76% and 4.50% in 12 months. However, expectations are downwardly biased as remaining participants expect it to trade at lower levels. That being said, the majority of participants were neutral duration.

- Surprisingly, no investors believed that the U.S. would enter into a recession before the end of 2024.

- The majority (56%) also expect the Fed to reduce its balance sheet by $1,250bn - $2,250 billion throughout the current tightening cycle. However, 90% of investors already consider liquidity conditions to have deteriorated.

- Meanwhile, there has been a shift regarding expectations for the 10-year German bund, with almost two-thirds of participants expecting it to remain at a level equal or higher to what the highest expectations were in the previous survey.

Where do you see U.S. CPI inflation averaging over the next five years?

Views from investment grade (IG) credit managers. Are concerns mounting?

- 58% of respondents expect a moderate widening in spreads in the next 12 months, up from 39% in 2Q 2022, and up from 30% a year ago. Meanwhile, only 13% of respondents expect a significant tightening.

- There has been a deterioration of expectations regarding the evolution of credit metrics, as 79% of managers indicated that they expect the leverage of lower quality IG credits in the U.S. to deteriorate amid a weakened economic environment. Regarding Europe, 83% of managers expect leverage metrics to decline.

- The main concerns among investors are inflation (88%), which leads to more restrictive monetary policies (54%). Moreover, a recession in the U.S. is also at the forefront of investors’ concerns (71%).

- Concerning Europe, investors are not expecting the conflict in Ukraine to further escalate (33%).

Global leveraged credit

- Global leveraged investors (53%) expect spreads to further widen in the coming 12 months, albeit moderately.

- Managers remain relatively confident on issuers' credit stance, with the majority of investors (89%) expecting only a moderate deterioration in overall corporate fundamentals amid the challenging economic environment.

- Within this space, 37% of investors favor global high yield bonds, up from the previous survey’s 32%. In contrast, U.S. leveraged loans remains the least favored product.

- Confidence in fallen angels remains considerably positive, as 30% of the survey respondents classified them as rising stars, while 70% classified them as potentially attractive opportunities.

- Concerns of defaults increased, as 70% of investors indicated that they expect defaults to stand between 3% and 5%. In the last survey, 70% of respondents expected defaults to remain below 3%.

- Managers were unanimously underweight in Chinese real estate.

Risk across the globe

Emerging markets (EM) local currency favored over hard currency

- Managers remain neutral in regard to the performance of EM currencies, with 53% expecting a positive performance of EM currencies in the next 12 months, and 82% expecting this over the next three years. 75% of managers think current rates are at a relatively cheap level.

- 75% of managers indicated that they favor local currency over hard currency (HC) for the next 12 months, up from 62% earlier in the year.

- Investors are very positive toward Latin America, with 87% of managers reporting it as their most favored region. This value is higher than the 72% registered in the last survey and the 57% seen one year ago. Interestingly, investors were equally uninterested in both EMEA and Asia.

- Notably, 33% of managers expressed having more than 15% exposure in EM HC corporates, an increase from the 29% registered in the last survey. Moreover, the percentage of those that indicated an allocation between 12% and 15% increased—from 7% to 17%.

Developed market currencies

- The majority of investors (75%) expect the U.S. dollar (USD) to trade between 0.96 EUR/USD and 1.05 EUR/USD. However, 20% consider that there is potential for it to trade up to 1.15 EUR/USD. Moreover, they do not expect the currency to break the 0.91 EUR/USD mark.

- 63% of managers expect G10 (Group of Ten) implied volatility to decrease in the next 12 months, a reversal from the previous survey in which the majority expected it to increase. One year ago, all managers expected G10 implied volatility to increase. The same occurred for EM currency implied volatility.

- Investors expect the USD to post the worst performance among G10 currencies, followed by the British pound (GBP) and and the Japanese yen (JPY). However, investors are not able to agree regarding the latter, as JPY was also the most favored G10 currency

Securitized sectors

- Two thirds of managers indicated that they seek to maintain their current risk position, with another third indicating that they seek to add risk. This contrasts with the last survey, when 35% of respondents indicated that they were seeking to reduce risk.

- Moreover, all managers showed interest in mortgage beta, with 60% indicating that they are already long and the remaining 40% indicating interest in adding.

- Nonetheless, the majority of managers (58%) indicated that they expect a moderate widening in non-agency spreads over the coming 12 months.

- Managers expressed balanced concern about underlying loan collateral credit deterioration, with 64% considering it to be their main concern.

Conclusion

Major central banks have been quick and strong on interest-rate rises to tame inflation, with moderating prices in the U.S. perhaps offering some light at the end of the tunnel for aggressive tightening. Nevertheless, markets don’t expect inflation to come down to traditional target rates for the next few years. Furthermore, market participants did not believe the U.S. would enter into recession before 2024. If this is true, are managers' expectations for the Fed and bond markets appropriate?

Participants in this survey clearly felt that inflation concerns were larger than recession fears. However, very rarely does the Federal Reserve embark on a tightening bias without triggering some form of recession. Should the economy evolve negatively in line with previous hiking cycles, managers may find themselves offside. The OBR thinks the UK is already in a recession, and we think it's likely that Europe, China and probably the U.S. will follow suit. How will central banks navigate this macro environment?

Fortunately, amid this microeconomic environment, managers believe credit fundamentals will be resilient. However, how deep will potential recessions be? Could the war in Ukraine escalate? Will China come to grips with COVID? How will fundamentals fare if the environment deteriorates more rapidly than currently thought?