Stick to the plan: Insights from our Q4 Economic and Market Review

Executive summary:

- When markets are volatile, it's tempting to move into cash. But those high yields on short-term cash instruments aren't as attractive once taxes and inflation are factored in .

- The balanced portfolio has been a linchpin of many investment plans for decades, and for good reason. Its performance in 2023 once again speaks to its resilience.

- Although markets can be affected by many factors, their long-term tendency has been to move higher. This is true regardless of which political party is in power.

Our latest Economic and Market Review emphasizes the importance of resilience in an investor's journey. As we explore its insights, let me encourage you to work with your clients to stick to their financial plans and remain steadfast. It's more than just a mantra; it serves as a reliable roadmap for enduring success in the dynamic realm of investments.

Navigating the market's complexities is a formidable task. Volatility in financial markets often triggers emotional responses, making it challenging to maintain composure. Staying the course becomes a shield against emotional decisions fueled by uncertainty during market downturns. While opting for cash might seem like a defensive move, it carries the risk of missing potential market rebounds. Deciding when to reinvest becomes a delicate challenge, with mistimed decisions resulting in missed growth opportunities.

Keeping your client true to their financial plan instills discipline and supports alignment with long-term objectives. While market conditions may fluctuate, the meticulously designed plan you and your client agreed upon should be a reliable guide for navigating these changes and realizing the desired financial goals over time.

Let's navigate insights from our Economic and Market Review:

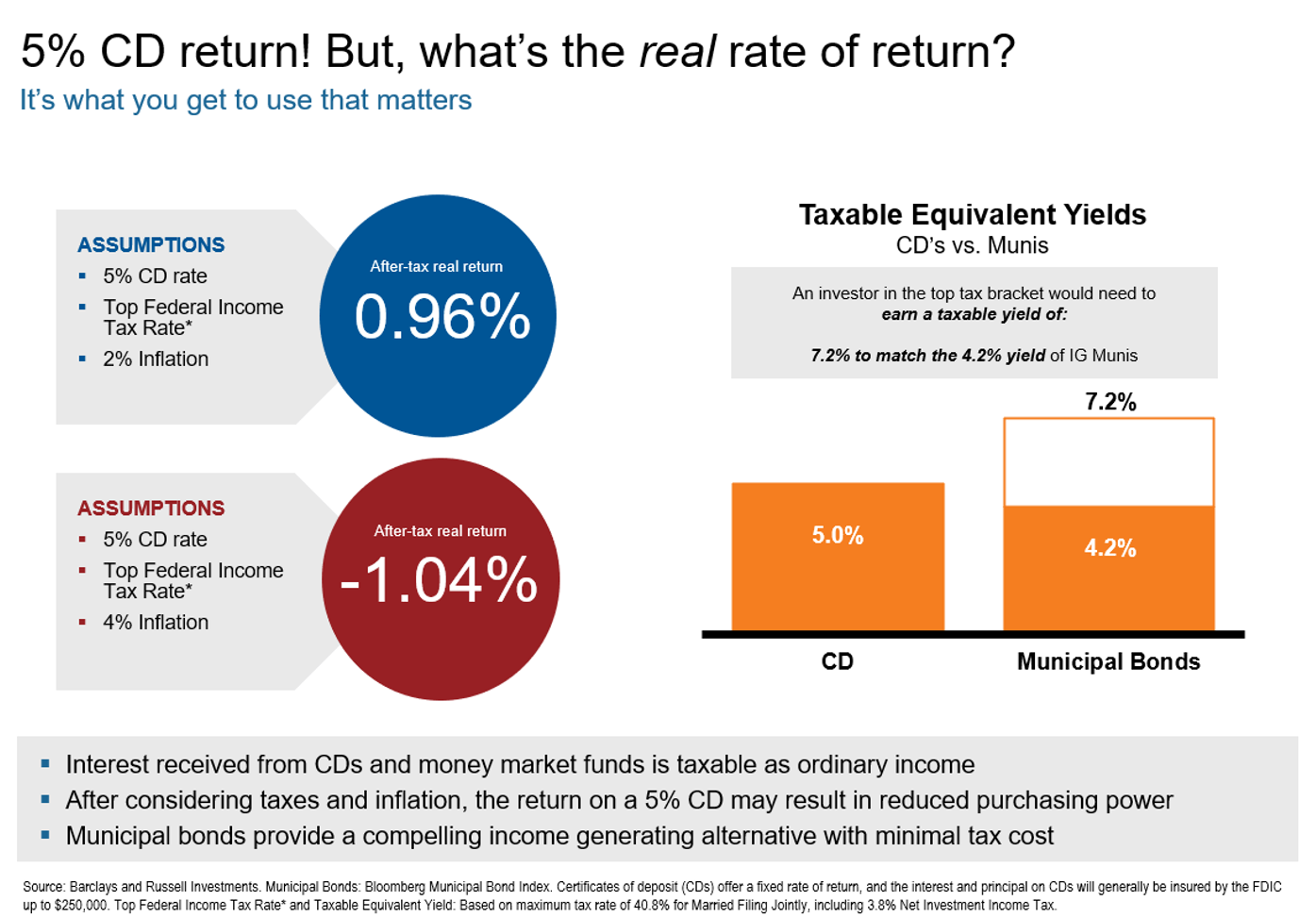

1. Yields and municipal bonds: unmasking real returns

Amid discussions about the enticing 5% yield on Certificates of Deposit (CDs), this chart reveals a nuanced reality. So much has been talked about the 5% yield that investors are getting on CDs and how good that feels; however, when you consider taxes and inflation – l look at what happens to that 5% return, particularly for accounts that are susceptible to taxes. What about owning municipal bonds? When you consider taxes, that CD would have to earn more than 7% for it to be comparable to the yield of an investment grade municipal bond. What's the message here? That 5% yield is not quite as attractive as it first appears.

(Click image to enlarge)

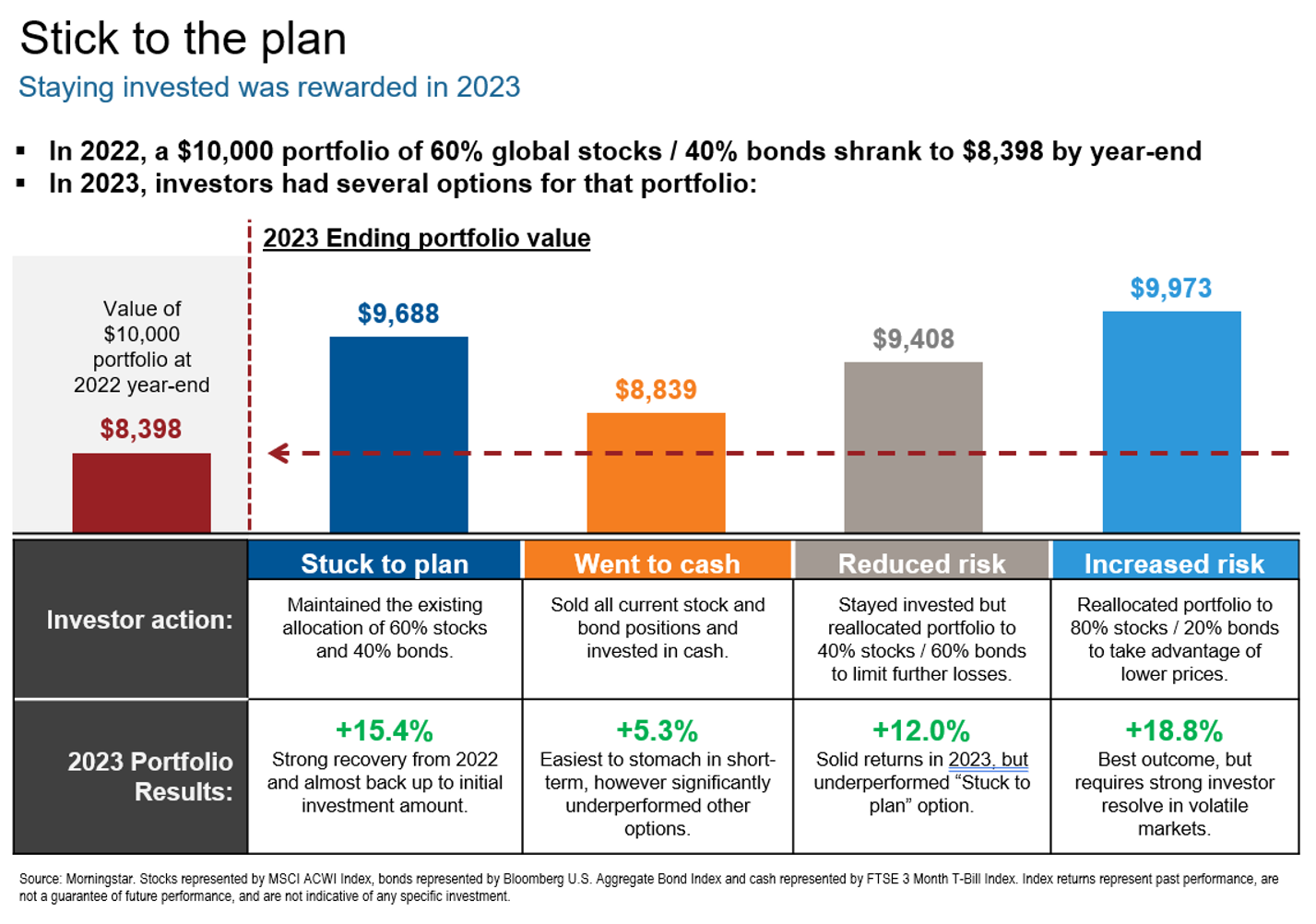

2. Staying the course: A lesson from the 60/40 portfolio

Let's look at the performance of the traditional 60/40 portfolio in 2022 compared to 2023. The chart below reinforces the power of sticking to your plan. Look at how well that portfolio performed in 2023, essentially reversing all the losses from 2022 and then some. Even if you turned the risk dial up and down slightly, the portfolio had positive results. Remember if your client has cash on the sidelines – when will they reinvest? So many decisions to make! They would likely have found themselves in a better position by staying committed.

(Click image to enlarge)

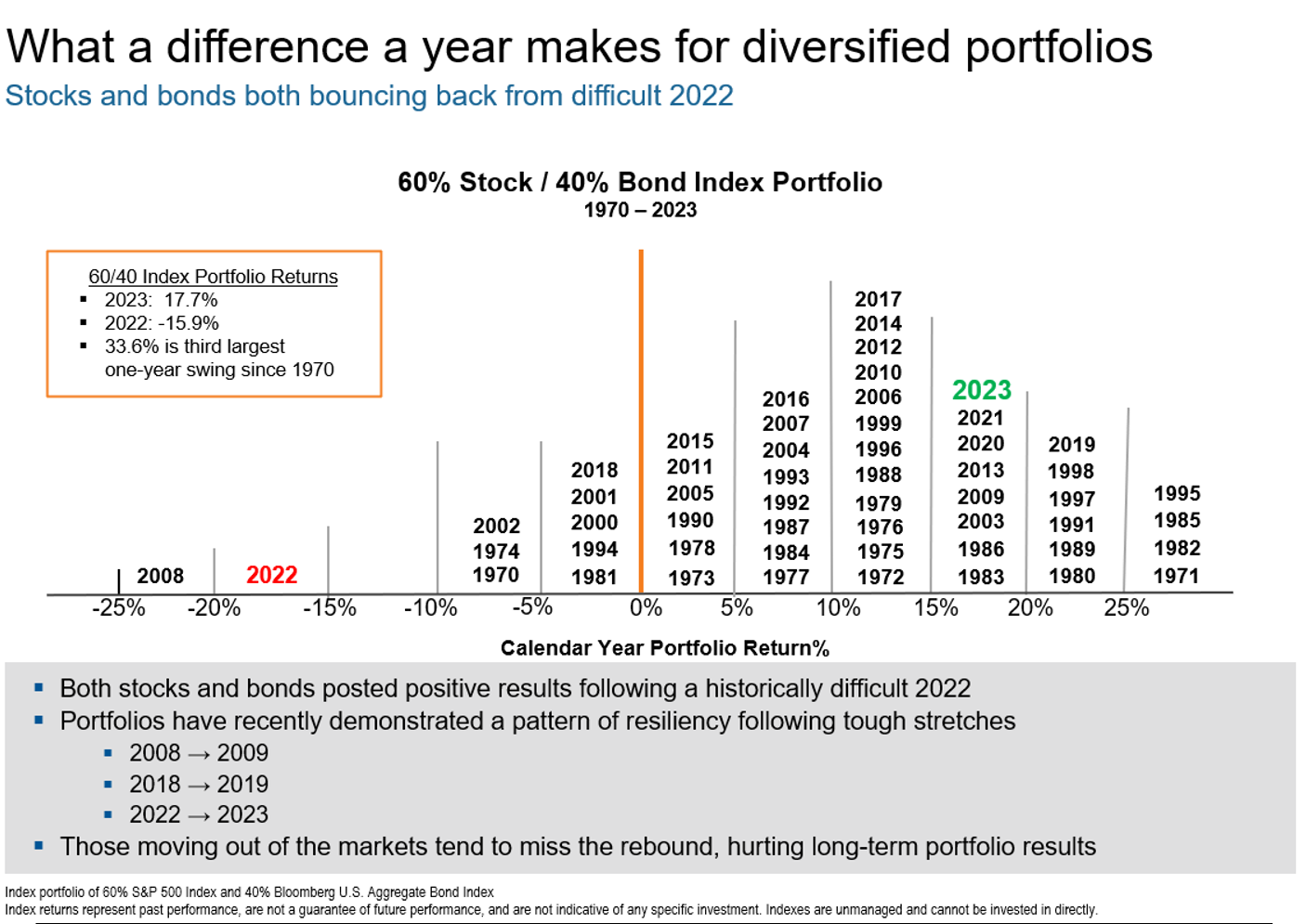

3. Stocks and bonds both bouncing back from a difficult 2022

Visually, what's the first thing you see when you look at the chart below? Markets go up more than they go down. It's interesting to see what generally happens in the year after a down year. As an example, look at 2022 and 2023. While 2022 was down, we had a strong bounce back in 2023! What's the point of all of this? Taking a historical perspective over 50 years challenges skepticism during negative return years. The visual representation emphasizes the resilience of markets. Our theme of sticking to the plan is reinforced: Resist the reflex to sell during downturns, as history suggests that staying the course is prudent and potentially lucrative.

(Click image to enlarge)

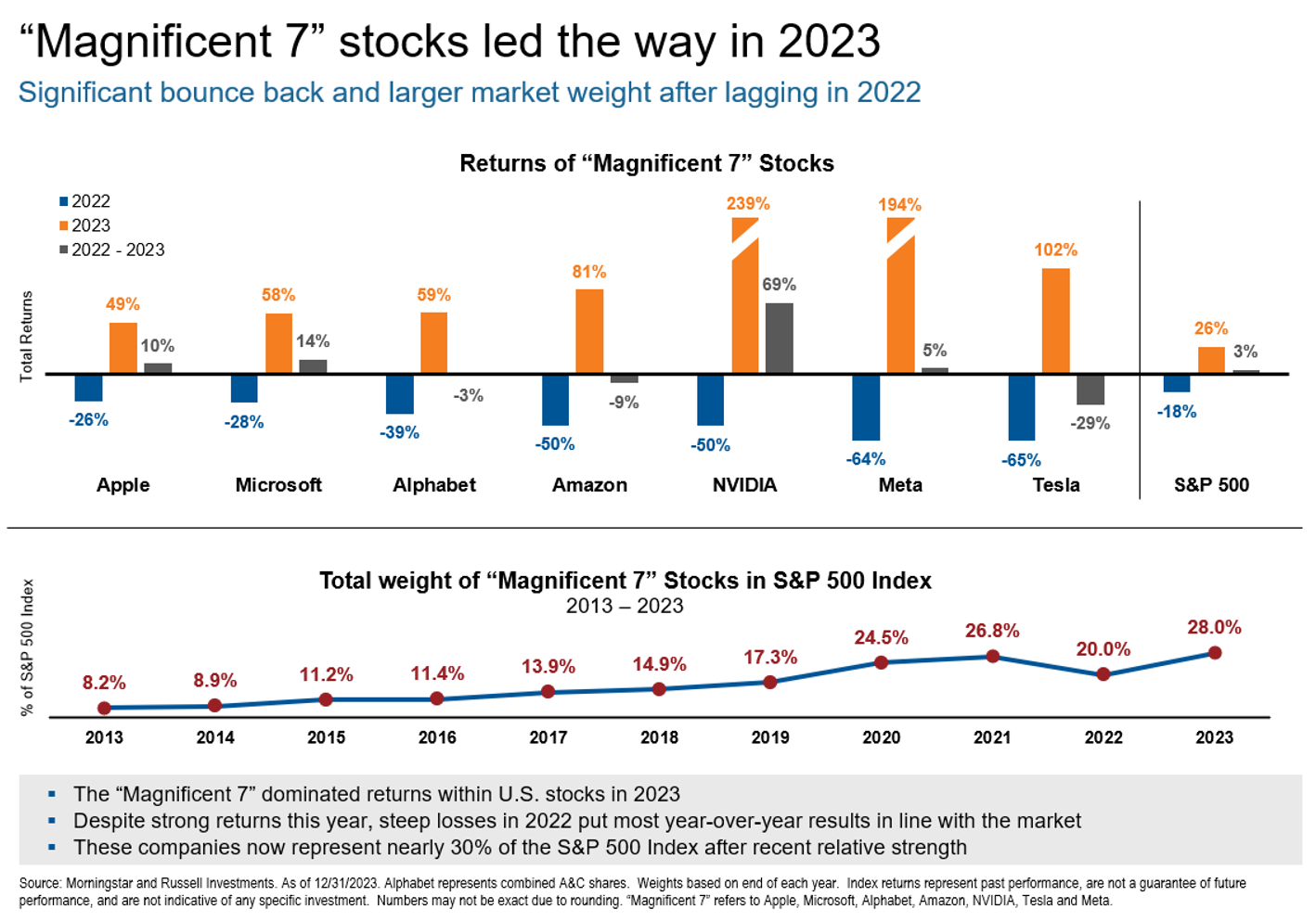

4. Magnificent 7 stocks: balancing gains and underperformance

Shining a spotlight on the Magnificent 7 – not the one with Yul Brynner but the dominant group of technology stocks. A couple of interesting observations on the Magnificent 7: they now represent almost 30% of the broader indexes, which means the market's movement depends on these names. Now look at how much the Magnificent 7 outperformed in 2023; however, when linked to the underperformance of 2022, they came in pretty much flat. The lesson again echoes our theme: disciplined investing and resisting the temptation to time the market are pivotal for long-term success.

(Click image to enlarge)

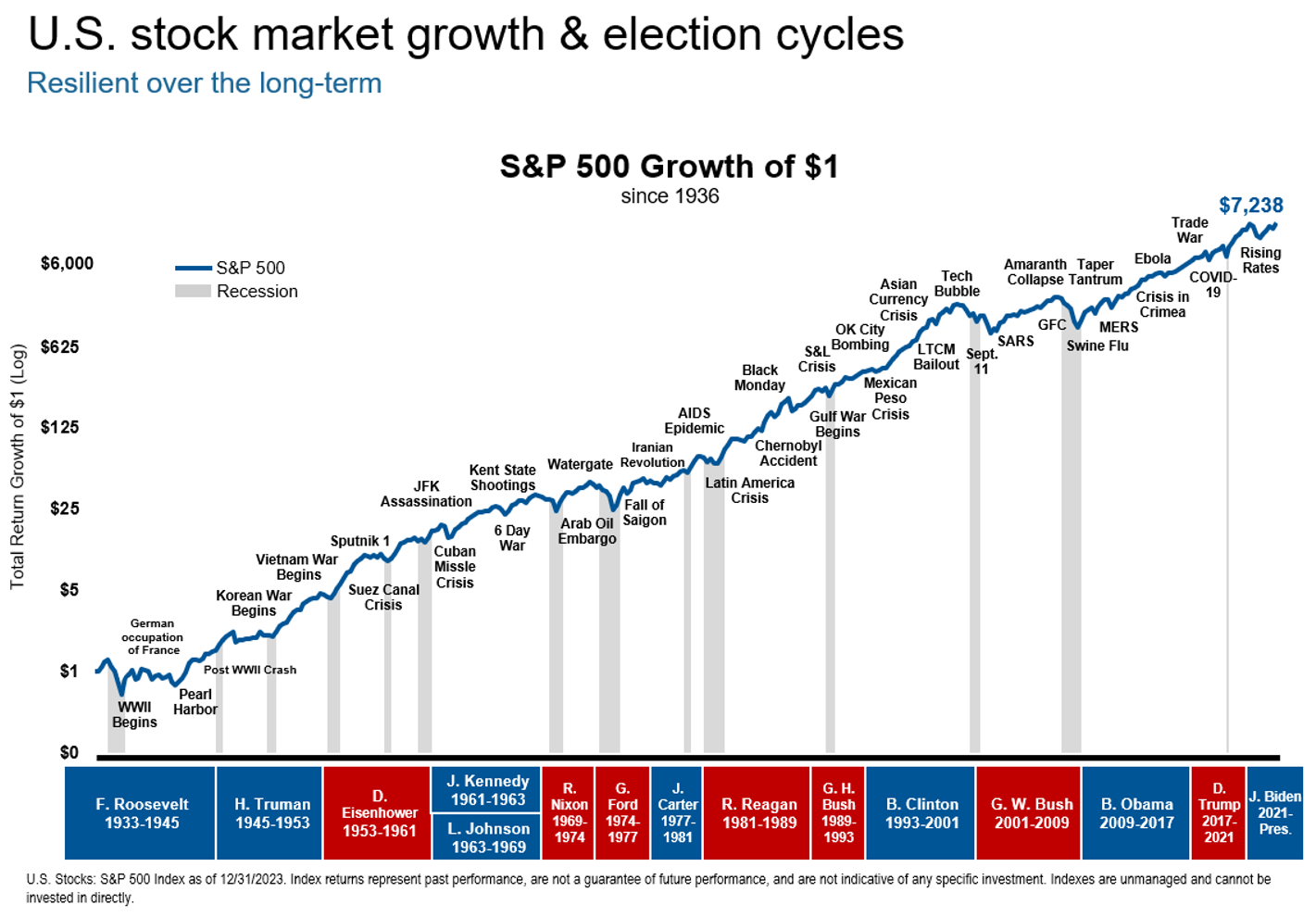

5. Election year concerns: The myth of market timing

The leadup dominates the news headlines to this year's elections, and how do investors often react in election years when they let their emotions rule? They raise the level of cash because they're concerned – especially if the election results might not be what they hoped for. It's important to realize that our preferred party wins the election almost 50% of the time in our lives, and 50% of the time, it loses. The chart below shows that markets go up more than 70% of the time, regardless of which party is in office. A fun activity is to ask your client to pick out the year they were born on the chart. Look at how many events and different administrations they have experienced. Did any of these changes in administration cause them to move their portfolio around? What's a better thing to do? Stay the course and accept that the political party you support may win or may lose, but the markets will most likely continue their upward tendency.

(Click image to enlarge)

By now, you've probably grasped the real hero in this financial rollercoaster – adhering to the plan! Whether you choose to rev it up or dial it down, remaining invested has historically led to positive results. Many investors may struggle to resist the urge to sell when the market takes a downturn. After all, their portfolio is expected to fund their future goals and dreams. This is where you, the financial advisor, can help your clients look at historical trends and challenge their skepticism. You can help them navigate turbulent markets. Do they still have doubts? Ask them to re-read the story of the Magnificent 7 over the two very different years of 2022 and 2023. The resounding lesson from this narrative? Discipline and sticking to the plan.