’Further hikes’ to come from the RBA

The Reserve Bank of Australia (RBA) increased the cash rate to 3.35% (from 3.1%) at the February meeting, in line with the market and our expectations. The commentary in the statement however was a surprise, with the RBA kicking the year off more aggressively than expected.

We had expected the RBA would hint we are nearing the end of the hiking cycle, in a similar vein to the approach taken by the Bank of Canada. However, the board have noted they think that ‘further rate rises’ will be needed over coming months.

The economic data since the RBA last met has been mild to disappointing. The Citi Economic Surprise Index chart below, shows how economic data has come in relative to economist expectations. A reading below 0 indicates that data surprised to the downside, and vice versa.

Source: Refinitiv Datastream, 4 Feb 2023

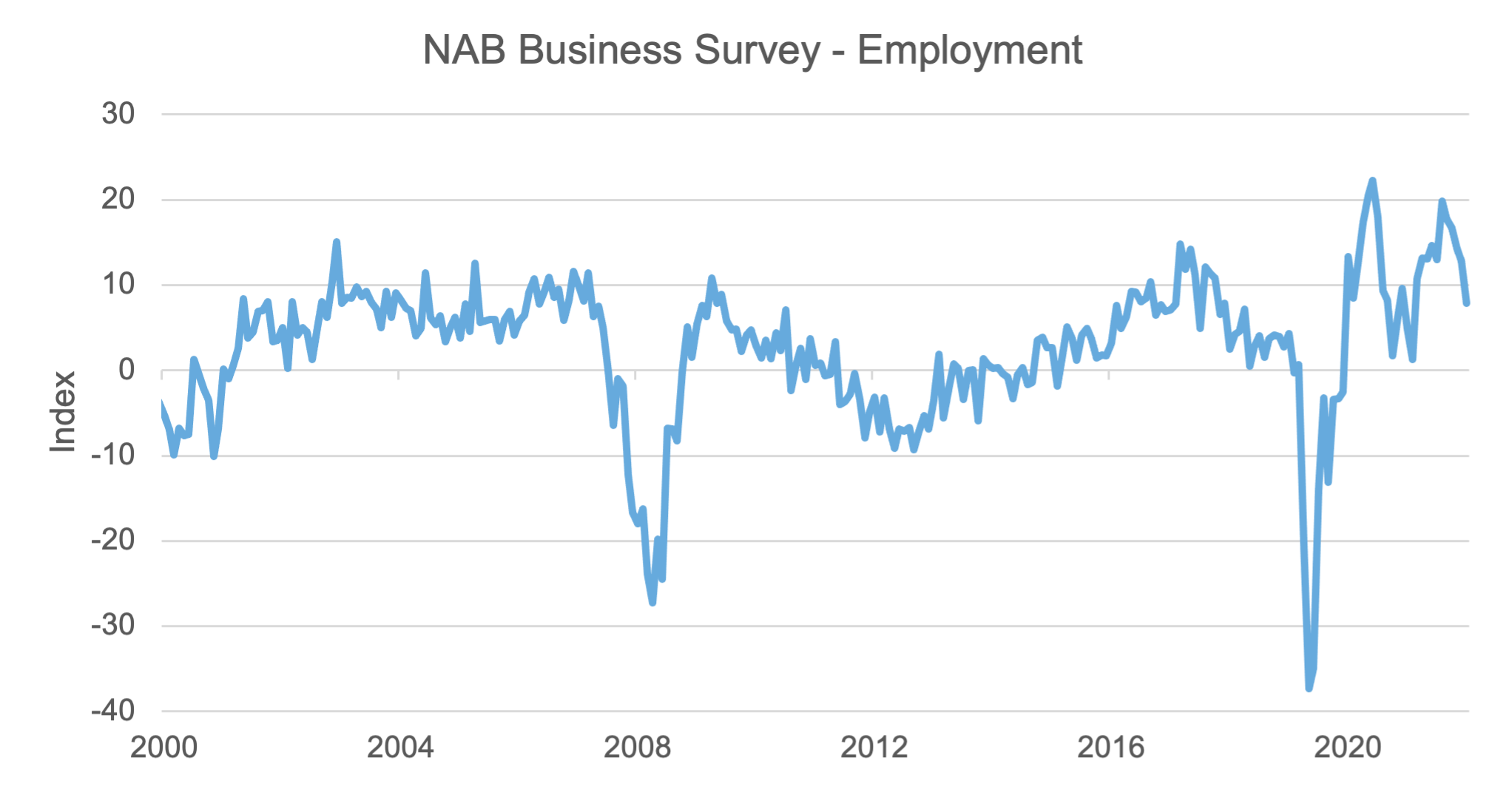

The labour market is tight, but outlook is softening

The labour market remains very tight, with the unemployment rate at 3.4%. However, forward looking indicators are showing that labour demand continues to cool – the most recent NAB Business Survey has come back quite sharply from the highs observed through the middle of 2022.

Source: Refinitiv Datastream, 24 January 2023

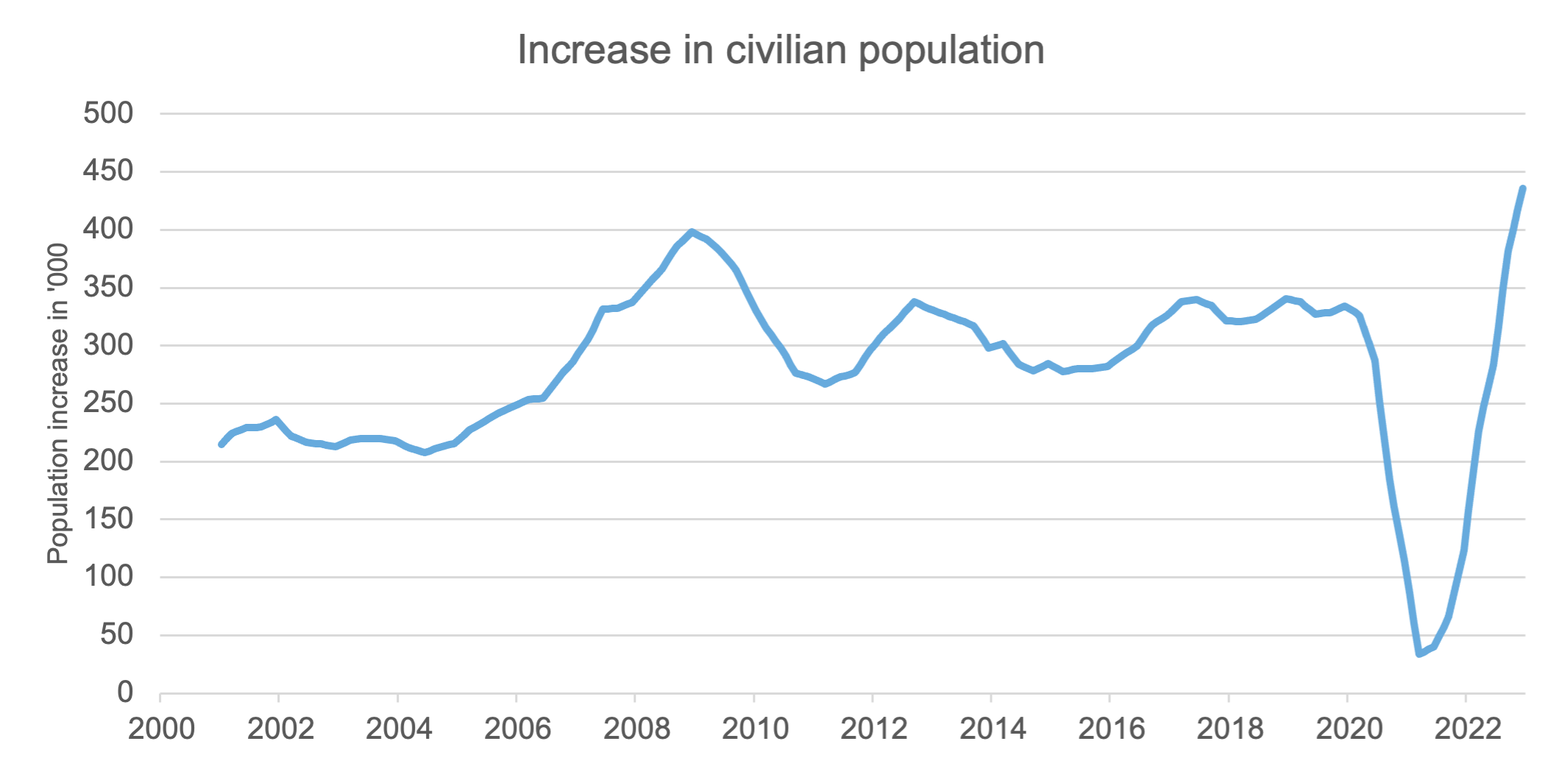

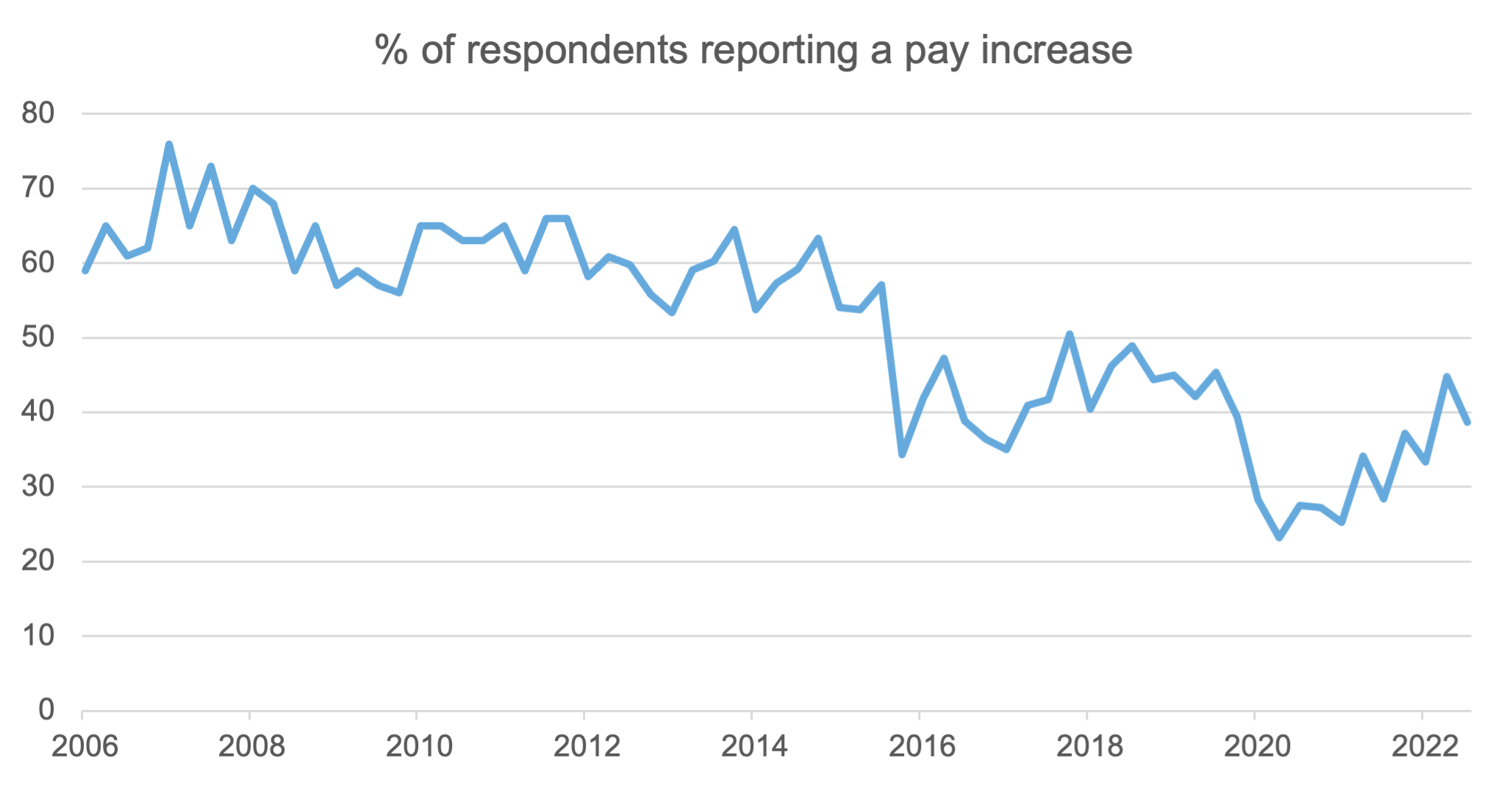

On the supply side, net migration has rebounded in a very strong way and is likely to remain this way through 2023. These two factors are likely to alleviate some of the tightness in the labour market and reduce the pressure on wage growth. In fact, the RBA themselves are forecasting that the unemployment rate will rise from 3.4% to 3.75% by the end of this year. Indeed, we have already seen a decline in the percentage of people reporting a pay increase through the December quarter.

Source: Refinitiv Datastream, 19 January 2023

Source: Refinitiv Datastream, 15 December 2022

Household spending continues to soften

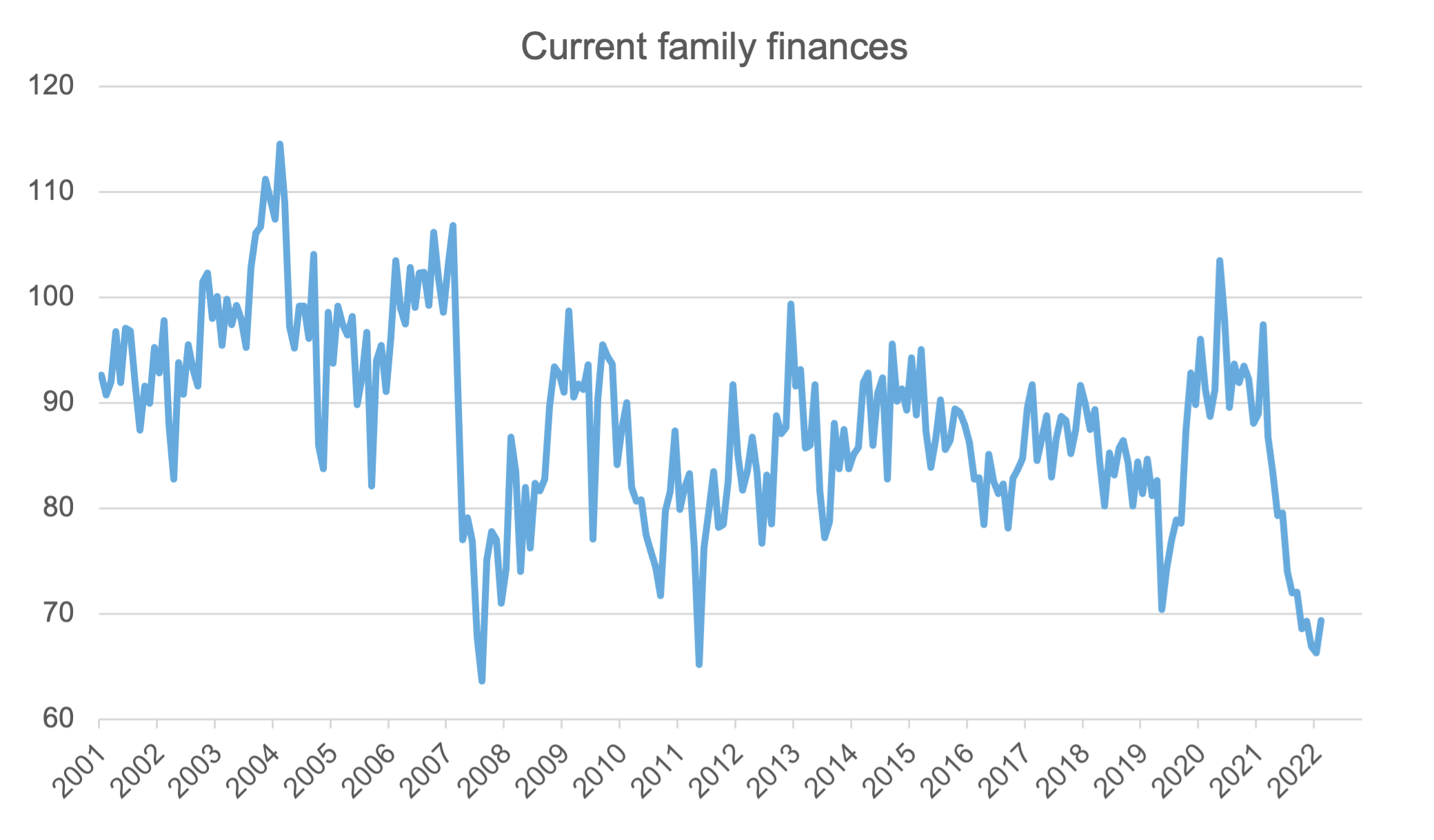

One of the key uncertainties for the RBA this year is the response from households to higher interest rates and higher spending. There is a very large portion of fixed rate mortgages that are due to expire this year, and for these households it is going to lead to a significant increase in mortgage repayments – thus leading to a reduction in disposable income. We can see the hit to household finances from the interest rates and inflation to date through the Westpac Consumer Confidence which surveys current family finances. A reading below 100 indicates net pessimism – the most recent reading was at 70.

Source: Refinitiv Datastream, 17 January 2023

The December retail sales print was also very negative. However, we would like to see another month of data to get a clearer reading as we suspect there are some issues with adjusting the data seasonally. This is being driven by more money being spent in November during Black Friday sales, and this is causing a complication with the data.

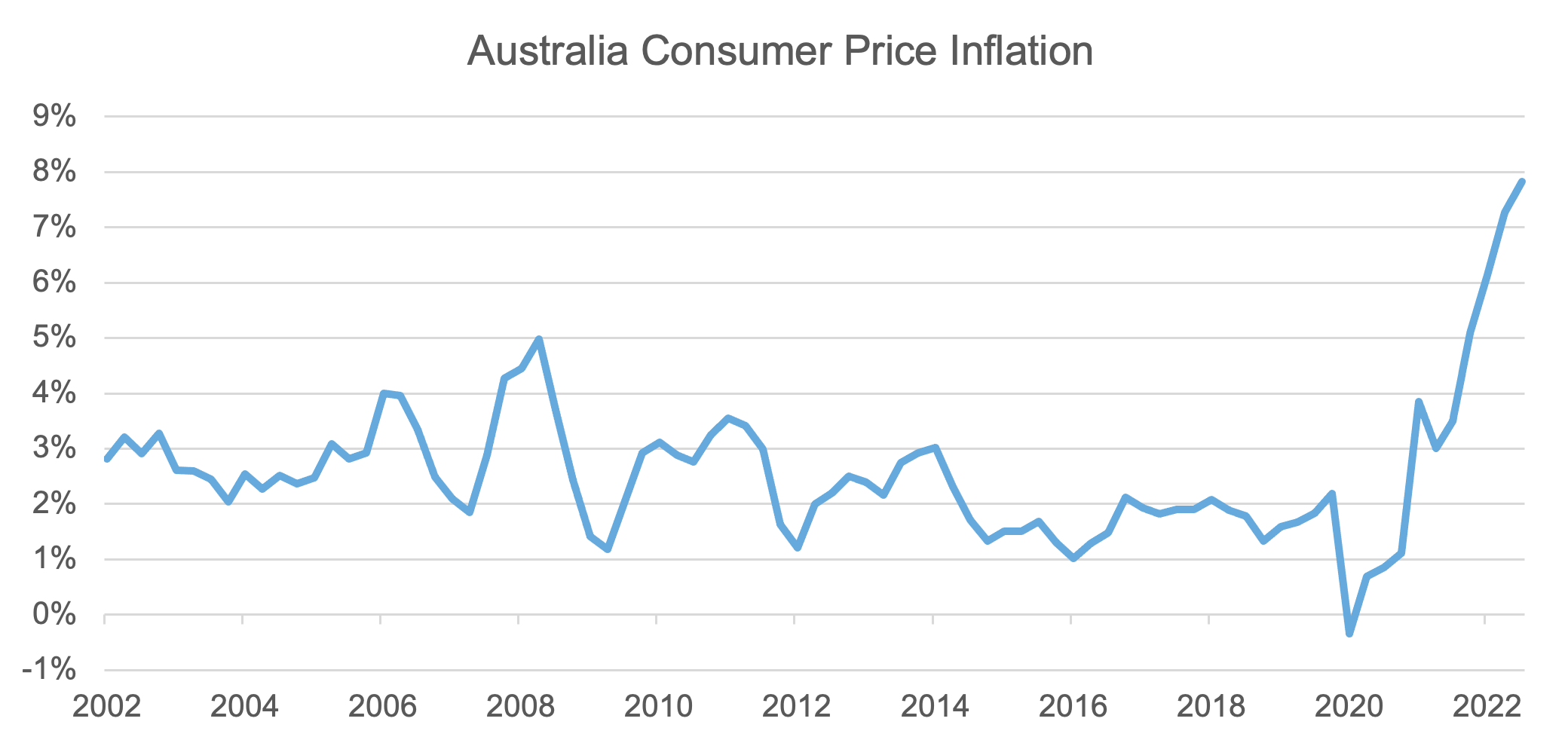

Inflation is still too hot, but is going to come down

The December quarter inflation print was higher than expected and was the catalyst for the RBA’s more aggressive tone. There are certain parts of the inflation basket that will remain elevated for longer, particularly rent prices, given the increase in immigration and limited supply (especially in major cities). However, the durable goods piece and other services are likely to come down over the year and this will mean that overall inflation will move in the right direction for the RBA albeit still above the target. More importantly, medium-term inflation expectations remain well-anchored to the RBA’s inflation target, which minimises the potential for a sustained inflation outbreak.

Source: Refinitiv Datastream, 25 January 2023

The RBA will keep raising rates, but are likely to be more data dependent than market expects

Given the strong rhetoric from the RBA, we believe that there is likely to be at least one more rate hike which will probably arrive in March. The market is pricing that the RBA cash rate will get to 4.1% (another three 25bp hikes from here) – whilst the risks of that outcome have clearly risen given the outcome of the February meeting, , we believe the RBA will remain data dependent and that any softness in incoming data (especially on the labour market and household spending) will see a shift in tone.

The economy should weather the rate rises

We believe that the risk of a recession in Australia is lower than the major developed markets, even with this higher rate path from the RBA. Australian fixed income continues to offer attractive value in our opinion, and we believe Australian government bonds will provide diversification benefits in the face of a worse economic outcome or further equity market volatility.