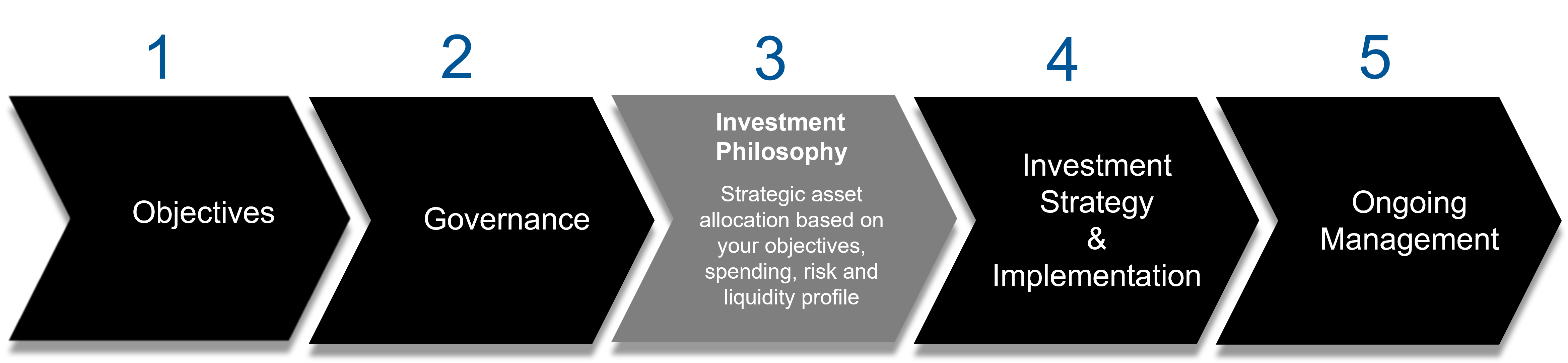

Step three: Investment Philosophy – a road map for the effective management of an investment program

The five essential steps of an investment program.

Click image to enlarge

In this article, we’ll take a look at the three key components of mapping an investment philosophy and why this is important for reaching your investment program goals.

1. Defining your investment beliefs

Investment beliefs are a key driver of an investment program, acting as the compass that helps you choose one road over another. Once defined, these beliefs support the development of your strategic asset allocation.

Identifying clear investment beliefs gives your organisation the necessary framework to quickly and confidently take action in an uncertain market. These beliefs also catch investment portfolio inconsistencies that may impact performance and push your objectives off the map.

To define your investment beliefs, begin by reflecting on objectives and needs of your organisation. Every not for profit organisation (NFP) operates in a slightly different landscape, so you need to consider your specific circumstances.. For example, you might include:

- spending policy

- liquidity requirements

- risk tolerance

Next, consider your specific circumstances. Every NFP operates in a slightly different landscape, meaning your investment beliefs should work in tandem with every other aspect of your organisation — not just the financial division. Once this has been addressed, you’ll determine the spending policy that fits your NFP.

Spending Profiles

A spending policy is key to determining the pattern of distributions from your investment program. Most NFPs consider both the level and stability of their spending over time. Even if your organisation has a steady hand on the wheel of your spending policy, flawed liquidity management could cause you to veer off the road.

Liquidity Profiles

To understand your liquidity profile, it's useful to make another map. This one keeps track of the sources, timing and flexibility of cash inflows and outflows. It gives you the visibility necessary to match liquidity requirements with the liquidity profile of your investments.

You’ll also need to view the full environment of your portfolio, which means considering both normal and stressed environments. For each asset class, identify the liquidity expectation in normal environments, then compare it against the estimated downside experience in stressed markets.

Risk Tolerance

Ultimately, an investment approach should deliver the returns you need within a tolerable level of risk. Fortunately, one of the benefits of the global financial crisis is clarity: Many NFP boards and finance/investment committees are now better able to articulate how much loss they can tolerate. When determining yours, consider these questions:

What is your capacity to tolerate loss?

This hinges on, among other things, the flexibility of a spending program and access to new

assets from your fundraising activity.

What is your willingness to tolerate loss?

Simply put, this means asking yourself whether you’ll be able to sleep at night if you take certain risk. Keep in mind that each member of a finance or investment committee and board will have subjective judgments which may not align with the overall opinion of the group.

2. Building a strategic asset allocation

The next tool you’ll need to map your investment philosophy is a Strategic Asset Allocation (SAA), which may have a significant impact on total returns for a portfolio.

An SAA determines how much you ultimately allocate to specific asset classes over the long term. In many ways, it’s like a set of road signs on your map: It indicates how you must proceed to align with your goals, spending policy, risk/return profile and liquidity needs.

Bands, also called ranges or limits, are often set around the SAA to help your portfolio stay on the map. Should a portfolio start to deviate outside these bands in response to changing market conditions, periodic rebalancing can bring it back on track.

It’s important to remember that an SAA is there to keep you on the road toward your long-term objective. Take care not to undermine it with short-term, reactive decision-making. Get the foundation right first, then stick to it.3. Document in an Investment Policy Statement

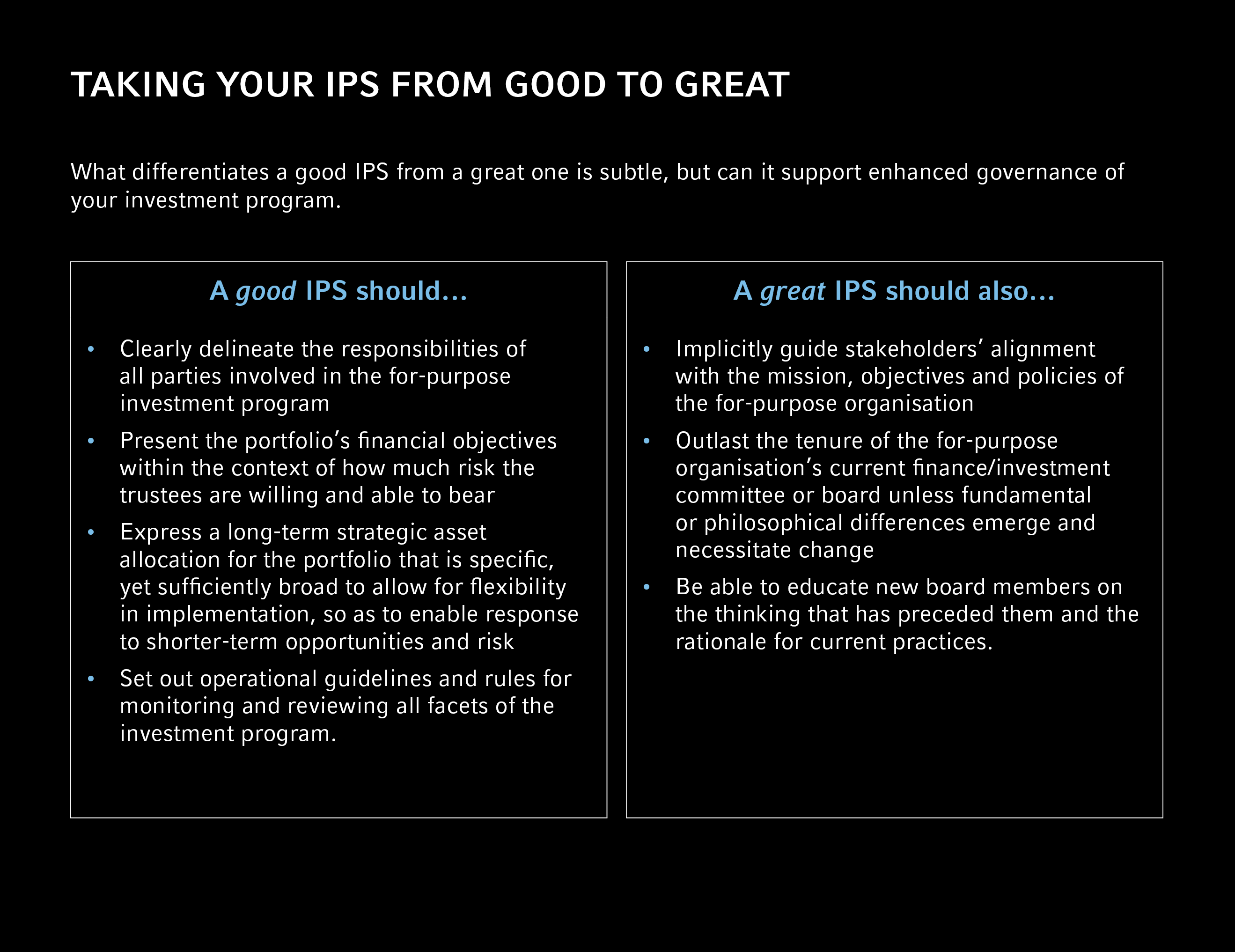

The Investment Policy Statement (IPS) captures your beliefs and expectations, like saving a road map with the appropriate route highlighted. It also provides long-term, strategic guidance on how to align your NFP’s mission, objectives and policies. The IPS can be an important tool for educating new key stakeholders on the purpose of the investment program, and it helps sustain your organisation's mission over time.

Click image to enlarge

Like any journey, having a clear destination is a necessary precursor to success. Focusing on defining an investment philosophy can help you navigate today’s market environment and create a road map for the effective management of an investment program.