Why investors should be alert but not alarmed in 2018

To put the current situation in perspective, Global Head of Investment Strategy, Andrew Pease, provides his view of global markets. Andrew lists three scenarios that he sees as most likely and provides a framework to help investors make their own calls.

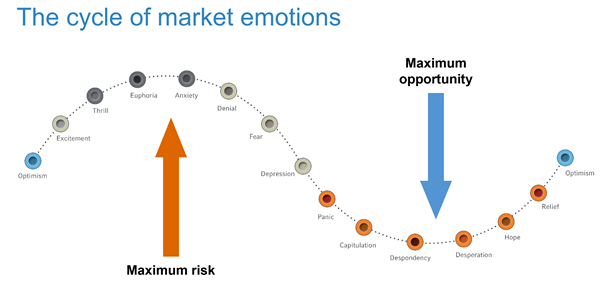

“Markets are certainly starting to feel a little euphoric, but we don’t think we’re in the danger zone just yet”.

The concern that investors may have climbed from optimism, excitement and thrill to outright euphoria – which is as good as things get before turning into fear, depression and panic – stems from the fact that the U.S. economy has been expanding for some time.

In addition, that the star economist Robert Shiller’s S&P 500 cyclically adjusted price to earnings ratio is close to 35 times. The only other times we have seen U.S. equities so expensive were in 1929 and 2000.

However, while this is a reason to be alert, there are other factors that should temper investors’ levels of alarm. In particular, the spread between U.S. 10-year and two-year bonds is still fairly benign, the companies in the S&P 500 are making exceptional profits and the indicators are not yet pointing towards a recession.

So, where to from here?

-

Markets grind higher

The U.S. Federal Reserve (the Fed) tightens interest rates three or four times by the end of 2018, the yield curve flattens and global equity markets rise, but slowly, in the face of headwinds. There’s a risk of an equity bear market from late in the year, and Europe, Japan and emerging markets outperform a soft S&P 500 in the U.S.

-

We see a blow-out rally

Despite their current lofty heights, markets continue to surge due to a dovish stance from the Fed. Growth also continues and inflation remains in check. In this scenario, the U.S. dollar is weak, emerging markets do well and everyone from journalists to taxi drivers are euphoric.

-

The Fed blows it

The potentially negative path is that the Fed misjudges and tightens interest rates too much, crippling an already sluggish U.S. economy. The key concept to watch here is ‘R-star’ –the estimated neutral level of interest rates when a country has full employment. If it turns out that the proper R-star is lower than the rate the Fed moves towards, then it’s quite possible that the U.S. market already peaked in January 2018.

Advice for investors is to be ‘leaning out’ as the risks increase. They should base their strategies on three building blocks with differing time horizons.

The first building block is to consider the macro-economic cycles that influence asset classes. The second – but least important – is to focus on valuations and the return potential across asset classes. The third is to factor in market sentiment by looking at price momentum versus contrarian indicators that could signal that assets have been overbought or oversold.

Focussing closer to home but with a ‘view from London’ Andrew’s view is that the Australian housing marketing is “an accident waiting to happen” and that foreign investors see the whole of Australia as a ‘China play’. His own view is that the Australian dollar is a great shock absorber that should protect local markets, that the S&P/ASX 200 is reasonable value and that if Australia is to have a recession, it will be brought on by its own Fed – the Reserve Bank of Australia.

See Running with the bulls: 2018 Global Market Outlook for further reading.