Active management outlook: Skilled stock pickers separate themselves in periods of heightened volatility

Is the outlook for active management still favorable?

In a previous article we highlighted the gauges we look at to monitor the active management environment and discussed how this could play out in a risk-managed multi-manager fund. We expressed optimism in the opportunity set, and the ability for active management to generate excess returns coming out of the pandemic. While ensuing market dynamics proved to be beneficial for active managers, the world remains stuck in a prolonged COVID-19 recovery period, with persistent market uncertainty and ever-evolving market dynamics that continue to challenge our thinking.

In this article we will highlight why we remain optimistic of the active management environment and the ability to generate excess returns through a multi-manager approach. Ultimately, we believe the current uncertainty, falling cross sectional correlations and the possibility of market volatility present a unique opportunity for active managers, regardless of underlying style preference.

Uncertainty is for certain

The number of concerns among investors are endless, though the top of the list includes inflation, stagflation, corporate earnings and the green energy transition, all of which carry a large degree of complexity and uncertainty. JP Morgan strategists expect a rebound in stocks, driven by favorable risk/reward dynamics1, while strategists at Morgan Stanley expect corporate profit margins to contract into 2023 due to sticky cost pressures and receding demand.2 UBS has acknowledged economic data remains uncertain, warning investors that markets may remain volatile in coming months.3 What do we take away from these mixed signals? Uncertainty is for certain—but with uncertainty comes opportunity.

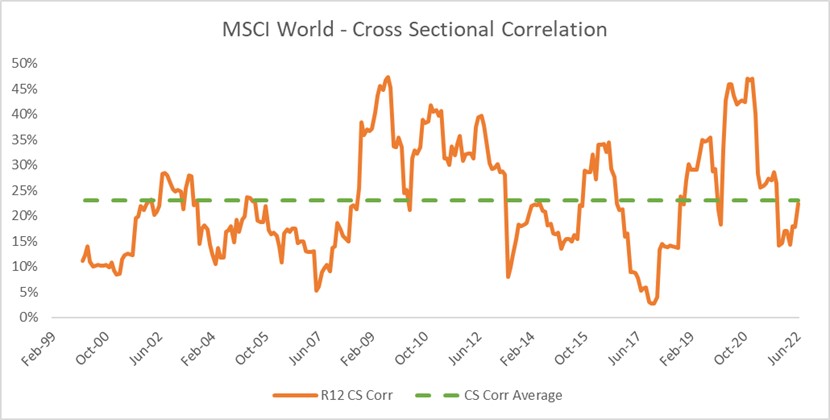

Falling cross-sectional correlations lead to broader opportunity set for stock-pickers

As covered in our previous article, we monitor cross-sectional correlations as one of our gauges for the active management environment. Since early 2021, cross-sectional correlations have continued to fall, increasing the breadth of idiosyncratic opportunities for active managers. Current market dynamics have led money managers to emphasize the importance of finding companies with competitive advantages and defined moats, along with the ability to pass pricing on to end consumers. We believe the ability to identify these characteristics, during a time with increased breadth, creates an increasingly favorable opportunity for active managers to generate excess returns—particularly if we experience heightened volatility moving forward.

Skilled stock pickers separate themselves in periods with elevated volatility

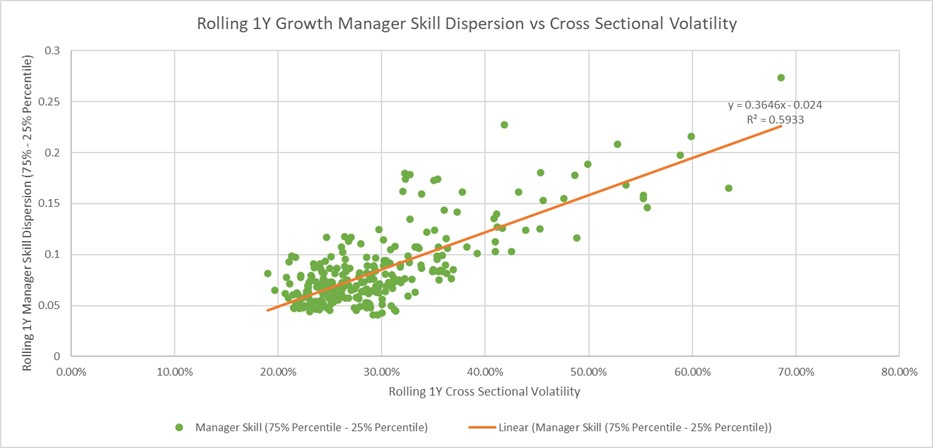

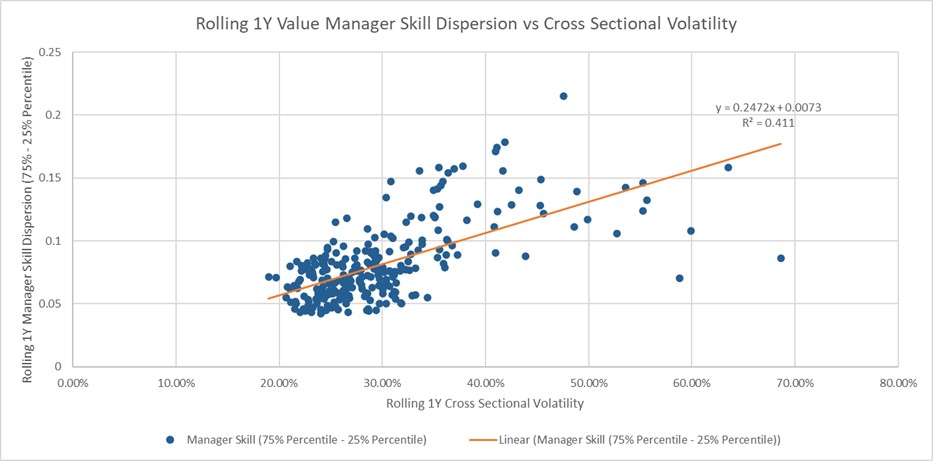

The combination of high uncertainty and falling cross sectional correlations presents a compelling landscape for stock pickers, particularly skilled stock-pickers in periods with elevated volatility. The charts below illustrate the difference in excess returns among global large cap managers performing in the 75th percentile vs. the 25th percentile, in relation to cross-sectional volatility dating back to 2000.4 In periods with heightened volatility, skilled stock-pickers tend to add additional value relative to peers compared to periods with standard market volatility. And this isn’t just true for a small subset of the market—both value and growth universes exhibit similar trends.

This is an extremely important phenomenon for several reasons:

- Avoiding value AND growth traps (yes, growth traps are a thing too!) is important.

In periods of higher volatility and uncertainty, stocks without the right fundamentals to succeed will be exposed for all to see. This underscores the importance of having a value manager that understands why a company is trading cheap and why it might rebound, as well as having a growth manager that truly grasps expected drivers of future expansion to justify a stock’s current valuation.Skilled stock pickers clearly have the edge here—the charts below show that money managers who possess skill across the growth and value spectrum add meaningfully to excess returns in times of greater volatility.

- Identifying skill in a money manager is hard

Just like picking good stocks is hard, so is picking good stock pickers. Many factors go into a successful money manager research process. If you don’t have robust manager research in-house, partnering with a firm that does is paramount to success.

- Timing managers and styles is even harder.

We believe that a multi-style, multi-manager approach is your best path to success in navigating the troubled waters that are certainly still ahead of us.

A skilled multi-style, multi-manager portfolio: Less filling AND tastes great!

A multi-manager approach is often viewed as a means of diversification and risk mitigation (i.e., less filling). What’s often underplayed is the excess return potential (i.e., tastes great), driven by the ability to tap into differentiated expertise in subsets of the market. This is especially relevant (and exciting) in an environment like the present, where we believe active management will benefit from broad tailwinds, regardless of style preference. The ability of skilled stock-pickers to generate excess returns in their specific subset of the market provides benefits that can be additive when combined with other style experts. We’ll expand on these benefits in a forthcoming article.

The bottom line

With uncertainty comes opportunity. And while the active management environment has improved since COVID-19, we believe the market continues to present favorable dynamics for active management moving forward. An increasing opportunity set, and the possibility of increasing volatility presents tailwinds for stock-pickers and provides a broader opportunity for skilled stock-pickers to differentiate themselves from peers. Ultimately, we believe that investors can enhance their excess return potential through a multi-manager approach, and we remain optimistic in the ability of skilled managers to generate excess returns through bottom-up stock selection, especially during times of uncertainty.

1 Source: eVestment universe, Russell Investments, SS&C, MSCI