Can you hold, please?

The Bank of Canada (BoC) has officially abandoned their tightening bias, while maintaining their overnight benchmark interest rate at 1.75%. What does this mean?

In their March 6 meeting, the central bank concluded the “the timing of future rate increases” is uncertain. But in their April 23 meeting, such a reference towards “future rate increases” was dropped altogether. Instead, the BoC now believes “accommodative policy interest rate continues to be warranted”, in other words, that interest rates should remain low for now. This explicit shift in their forward guidance, coupled with a downgrade to Canada’s 2019 growth, ignited a rally in domestic bond yields and prompted a sell-off of the Canadian dollar (CAD).

What a difference a day makes. The chart below shows the Canadian yield curve1 on April 23 (blue line) versus April 24 (orange line). The yield on the 10-year Government of Canada bond (10Y) declined by 7 basis points (bps) to 1.676% and the yield on the 3-month Government of Canada bond (3M) closed at 1.675%, teetering on the verge of inverting. In fact, the 10Y-3M part of the curve briefly inverted on April 24 and could do so again. An inverted yield curve is often viewed as the harbinger of an economic downturn.

Source: Russell Investments

Indeed, the dovish (less aggressive) forward guidance was accompanied by a larger than anticipated downgrade to the growth outlook for Canada in 2019. The BoC now believes growth will come in at 1.2% in 2019 versus their prior estimate of 1.7%. The downgraded outlook was in part due to trade uncertainties hindering domestic investment more so then they previously expected (keep in mind the USMCA2 hasn’t yet been ratified by either the U.S., Mexico or Canada as yet), weaker housing market trends (though they believe households are adjusting), and softer foreign demand (due to weaker global conditions) weighing on export growth. BoC’s updated assessment, however, is now within Russell Investments’ forecasted range of 1% to 1.5% for 2019 gross domestic product (GDP) growth as noted in our 2019 Global Market Outlook – Q2 Update. Meanwhile, inflation is not a concern with core Consumer Price Index (CPI) measures generally around the 2% level and in-line with expectations.

Despite this downshift, the BoC continues to expect a healthy pick-up in growth over the second half of 2019 and a strong enough transition into the new year that their 2020 growth estimate of 2.1% is unchanged versus their previous Monetary Policy Report (MPR). Nevertheless, the BoC have come around to the view that a weaker growth profile for 2019 has widened the output gap3. Moreover, they revised down their “neutral” policy range by 25 bps at both ends, to a range of 2.25% to 3.25% versus 2.5% to 3.5% previously. In other words, the current policy rate of 1.75% is 50 bps, or two hikes4, away from “neutral”.

Considering the dovishness of their statement and accompanying MPR, what we can conclude is the BoC is now in a holding pattern for the rest of this year. Any change in policy, therefore, will be dependent on new economic data. However, if we deduce what they are messaging from their projections, which is for a strong pick-up over the second half of 2019 and 2%+ GDP growth in 2020, they are likely leaning towards the next move to be a rate increase at some point in 2020. The markets, however, are unconvinced. And in fact, pundits place the odds at 50% for a rate cut by year-end5.

Here’s what we think will happen:

- Although an interest rate cut can’t be completely ruled out, our central scenario is for a policy hold this year. So long as that view comes to fruition, and the markets abandon the idea of a potential rate cut, yields could move higher from current levels. Keep in mind the yield on the 10-year Government of Canada bond was at 1.82% in mid-April.

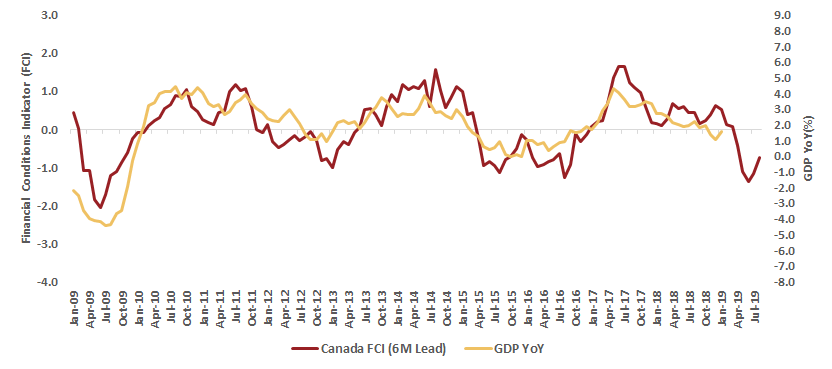

- We also believe growth should improve over the second half of 2019. The fact that we are seeing a tentative turnaround in our Canadian Financial Conditions Indicator (FCI), shown below, has been a welcoming trend. Where we differ is the sustainability of that strength into 2020. BoC believes growth next year will be 2.1%. This seems much too strong without a resurgence in exports and business investments. Thus far there is no reason to believe an upside breakout in either is forthcoming.

FCI based on data available as of 4/23/2019, projection to August 2019.

While we take some comfort in seeing improvement in the FCI, we will hold judgement on its sustainability. We believe the key risks are in the housing market, where residential construction activity has decelerated; as well as slowing personal consumption due to the elevated level of household indebtedness.

These concerns lead us to conclude the BoC will be sidelined for the foreseeable future. If pressed to make a call on the next move, however, it is more likely to be an interest rate cut.

1 A yield curve shows the difference between bonds of different maturities. It “inverts” when bonds with longer-term maturities offer lower yields than bonds of shorter-term maturities but similar credit quality. This is an indication that investors are concerned about the longer-term growth prospects for the economy.

2 USMCA=U.S., Mexico, Canada Agreement, the intended successor to the North American Free Trade Agreement.

3 The difference between between actual and potential economic output.

4 The Bank of Canada typically implements any change in its key policy rate by increasing or decreasing the rate by 25 bps, or 0.25%.

5 Source: Thomson Reuters DataStream as of April 23, 2019.