Special report: Does ESG spell the end for commodities? We don’t think so.

After extreme volatility in early 2020, commodities have logged a roughly 75% appreciation over the past 15 months.1This brings up two key questions:

- Is there any upside left to commodities, particularly given increasing environmental, social and governance (ESG) concerns among investors?

- Is the macroeconomic backdrop today similar to that of prior bull markets for commodities?

We believe that the answer to both questions is yes. To explain why, let’s start with a recap of what led to previous commodities supercycles.

The history of commodities supercycles

The first real supercycle in commodity demand started in the 1890s, following rapid industrialization and population growth in the United States. This cycle ended around the time of the first world war as the economic focus moved from industrialization to supplying the military. The second major upcycle for commodities resulted from post-war reconstruction demand in the 1950s, particularly in Germany and Japan. The most recent upcycle in commodities resulted from growth in China, sparked by the government’s goal of moving hundreds of millions of people from remote farming communities into urban developments. From the mid-1990s through roughly 2015, China’s growth led to incredible demand for raw materials to build housing, infrastructure and industrial facilities.

Is another supercycle in the works?

In our view, supercycle may be too strong of a word to describe the outlook for commodities, but we do believe a period of growth is likely. Why? We foresee another phase of rising commodity demand taking shape, driven by the need to maintain aging infrastructure as well as the increasingly urgent need to combat climate change. What’s more, we believe that this will likely be a long-term trend. Why? On the one hand, it’s clear that deferred maintenance on aging infrastructure needs to be done, and this work has political support, as it’s jobs-positive. On the other hand, investing to transition to carbon-neutrality also has increasing political and social acceptance, with the idea of climate neutrality as a national goal accelerating over the past year. Critically, both of these initiatives are highly commodity-intensive.

How the rise in ESG investing could impact commodity prices

In addition to the broad goal of climate neutrality, we believe that institutional interest in environmental, social and governance investing is also supportive to commodity prices. At Russell Investments, we’ve seen an increasing institutional focus on ESG matters, and we are closely monitoring the rapid development of ESG policies among our investment managers. By definition, this means increasing scrutiny on which public and private companies are taking climate change seriously (among other goals) and which ones are not. Investors are increasingly asking for and employing a farm-to-fork framework for analyzing raw material sourcing, renewable energy and supply chains—and the scrutiny is oriented toward both domestic and global supply chains.

The Wall Street Journal’s recent article, “How Much Carbon Comes From a Liter of Coke? Companies Grapple With Climate Change Math,” depicts this trend well—and we feel that such a trend will only continue to gain momentum. And with the U.S. Securities and Exchange Commission (SEC) working on climate-disclosure regulation, it seems that greenwashing could become a punishable offense. Would anyone have predicted this 10 years ago?

Example #1: Sustainability

In mid-July, the Office of Foreign Assts Control (OFAC) announced that it would be cracking down on American firms that do not certify that their supply chains are not tainted by forced labor or other human rights abuses. How does this lead to upward pressure on commodity prices? ESG’s focus on ethical sourcing directly leads to greater transparency for commodity production, and I believe that a likely side effect of this will be higher commodity prices as sustainable mining and processing processes become increasingly required—often ahead of the real economy’s ability to deliver the goods. Put another way, the pace of ESG awareness is advancing far more rapidly than advances in green commodity production technology.

This leads to lower spare capacity in most commodity markets, where older extraction and processing facilities have been closed (potentially following active ESG pressure or more passive capital starvation), while at the same time demand for many commodities is increasing as climate-neutral projects are increasingly sought-after and funded both privately and publicly. Interestingly, ESG as a concept is explicitly not concerned with commodity prices in its prescription for the transition path to green commodity production and climate neutrality. We see this as the greatest driver of higher commodity prices.

Example #2: EV batteries

The conflict between ESG theory and the reality of today’s global commodity sector is best illustrated by the electric-vehicle (EV) battery industry. The background for global battery demand results from net-zero commitments from countries that represent 54% of global greenhouse gas emissions.2 To power both electric vehicles and for stationary energy storage connected to solar and wind generators, Rystad Research has identified roughly 1.7 terawatt hours of demand for electric batteries by 2025, up from about 300 gigawatt hours today. This is nearly six times as much demand in less than five years, which is a huge incremental demand for nickel and other metals.

Today’s EV batteries are called NMC 811, which is an abbreviation for 80% nickel, 10% manganese and 10% cobalt. The first issue with acquiring the materials for these batteries is that nickel mining is concentrated in Indonesia and the Philippines, where ESG professionals have major concerns about processing, as high-pressure leaching leads to tailings, which are often disposed of into the ocean. Second, half of all battery-grade nickel processing is done in China, and by 2025 over two-thirds of all global nickel processing is predicted to take place between China and Indonesia.3 Rystad has also done asset-level research to identify companies like Tesla, CATL in China, Panasonic, LG Chemical, Volkswagen and others that have current programs underway to create the battery manufacturing plants to satisfy those battery demand figures.

Here’s the problem: Globally, the world produces 2.5 million tons of nickel a year, most of which goes into stainless steel.4 By 2025 we’ll need another 1 million tons of nickel just to satisfy the battery demand, and this does not address the increasing demand for stainless steel due to the passage of new infrastructure bills. By 2028, the globe could need 2 million additional tons of nickel a year for batteries, given net-zero targets. That’s a huge change in demand, particularly at a time when investors are increasingly focused on ethical sourcing. With ESG-driven pressures from investors to concentrate on the ethical production of nickel rising at the same time as social and political demand for batteries to solve net-zero targets, it’s not hard to see how nickel prices could adjust upward. It’s equally important to understand that this constructive ESG supply/net-zero demand argument exists not only for nickel, but for virtually all of the metals that go into batteries. Arguments for the bulk of the industrial metals complex are also similar.

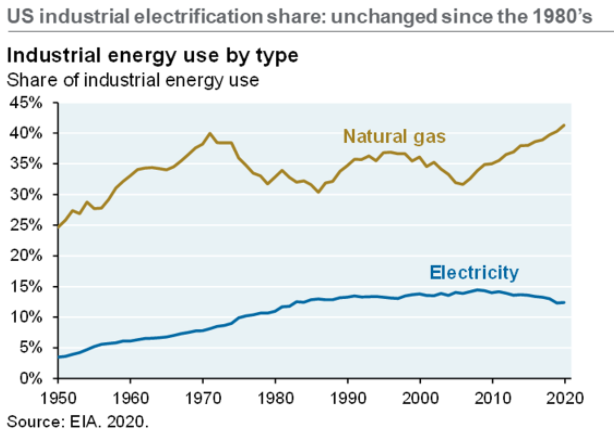

Another factor behind the potential for rising commodity prices: Electrification

Let’s broaden out the constructive argument for commodities beyond metals. A major change that’s required to achieve climate neutrality is the electrification of industry. In 2020, the Department of Energy (DOE) and Princeton estimated that the process of electrification across industry will require roughly 100,000 gigawatt miles of transmission lines in just the next 10 years in the U.S. alone, which is 50% more transmission lines than currently exist. Another 180,000 gigawatts of transmission lines in the U.S. would then be needed in the following 10 years, and so on.

Click image to enlarge

This same research has calculated that industry will increasingly be powered by solar and wind, and that we’ll need to ramp up from about 250 gigawatt hours of wind and solar capacity installed in the U.S. today to something like 1 terawatt of combined wind and solar capacity in 10 years. This data is summarized in research published by The Global Infrastructure Hub, a team funded by the UK, Australia, Canada, Germany, Mexico, China, Korea, Indonesia, Singapore and others, which calculated that US$94 trillion in investments are needed globally over the next 20 years in order to achieve sustainability and climate neutrality (starting at about US$3.2 trillion this year and ramping up to US$4 trillion a year by 2031). The energy component of the Global Infrastructure Hub’s research totals some US$920 billion in global energy investments needed in 2022 alone, and the transmission lines, solar and wind generators are part of this. We think about these investment figures relative to their impact on higher demand for mineral content in this infrastructure, the power demand to produce and transport this infrastructure and the labor cost that goes into it.

Where will the funding for clean energy come from?

Let’s talk about where the funding will come from for the projects required for climate neutrality. Axios recently reported that Jigar Shah, who heads the DOE’s loan programs office, wants to grow the loan program from US$200 billion a year up to US$1 trillion a year to achieve U.S. climate goals. So that’s going to be loan guarantees for new projects across advanced nuclear, carbon storage, EV and battery manufacturing, critical mineral sourcing, extraction, etc. Thinking practically about this, we need to change the way most industry is powered, what kind of cars we drive, the power used in global shipping and so on. That’s a lot of change. And polls consistently show that most individuals aren’t willing to pay extra in taxes or fees to achieve climate neutrality. In a 2019 survey, for example, Toluna found that just 37% of consumers would pay up to 5% more for environmentally friendly products. What this means is that, in all likelihood, governments will need to find another way to incentivize changes in consumer behavior. This will probably result in additional large government-sponsored projects, such as the DOE’s loan programs office.

Most of the economists we’ve spoken with generally agree, noting that we'll probably continue to see the government's influence increase over time in order to effect change—as the public increasingly votes for representatives who push for climate neutrality, leading to large spending programs. Ultimately, our belief is that increased interest in ESG investing, coupled with public awareness of the need for climate change, should lead to heightened demand for commodities to transition to a climate-neutral global economy.

The outlook for oil and natural gas

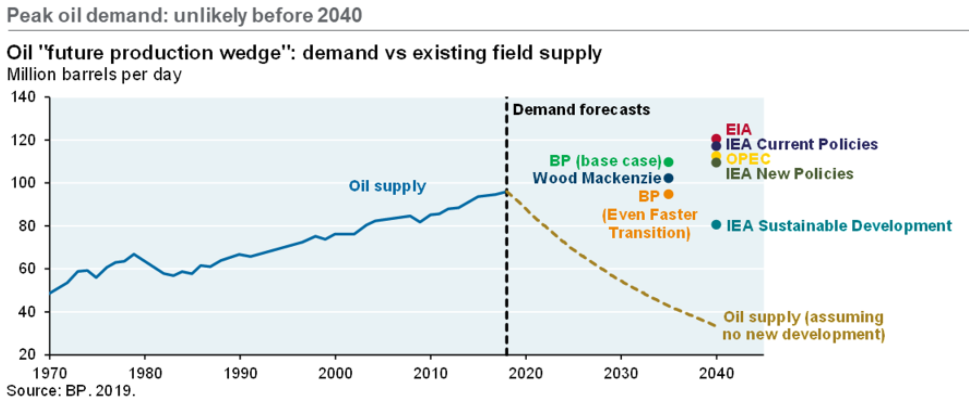

Let’s move on to oil, where visibility on longer-term supply is an interesting guesswork and demand is equally difficult to forecast long-term. Notably, capital expenditures across the oil industry in 2021 are half of the level seen in 2014. While this sounds great in the context of the climate debate, due to the time lag between planning and funding projects to transition to green energy, oil demand is expected to grow by roughly 7 million barrels per day (mmbpd) between 2022 and 2030. At the same time, non-OPEC supply is projected to easily decline by 13 mmbpd, due largely to the normal decline rates experienced by producing assets in the United States, Russia, China and Norway.

It is possible that this 20-mmbpd gap could be filled by non-OPEC sources, predominantly through enhanced recovery techniques lifting reserve growth from existing fields. However, this approach is a short-duration investment which produces more oil in the near-term while risking a more rapid reduction in total recoverable oil from the existing oilfields. Zero Hedge reported that capital expenditures by U.S. energy companies recently hit the lowest level since 2004, with the ratio of capital-expenditure-to-depreciation falling to 0.44, i.e., only 44% of depreciated assets were replaced. This suggests that oil prices may spike before alternative energy sources are widely available.

Natural gas is in a similar predicament. Quebec recently rejected a liquefied natural gas (LNG) export project, citing environmental concerns. One result of the underinvestment is a shortage of gas in Europe, where Britain recently measured at just 29% of capacity compared with 52% in 2019, the year before the pandemic struck. At the same time, it has been reported that Royal Dutch Shell plans to exit its California-based oil and gas producing joint venture with Exxon, while Shell, Chevron and others are reportedly divesting numerous assets this year, including oil and gas fields in the Permian region of Texas. Reasons given include an effort to focus on renewables, or to focus on higher-performing assets. What does this mean? In short, it’s that the first movers to transition to clean energy will gain a positive reputation with the public, while the laggards will likely profit from the (likely) growing undersupply of oil due to underinvestment.

Click image to enlarge

The overarching story is highlighted by JPMorgan, which in its July 2021 commodities report suggested that ESG and the focus on climate-neutrality is reducing traditional energy supply at a faster rate than renewable energy can supply into growing global energy demand. The net effect is that prices can go higher.

The bottom line: ESG investing isn’t the death knell for commodities. In fact, it may be the opposite.

As pressure to combat the intensifying climate crisis mounts, the demand for materials needed to produce alternative energy sources is likely to accelerate as well, far outstripping supply. At the same time, the global reliance on traditional energy sources, such as oil, will likely remain elevated due to the amount of time it takes for alternative energy sources to come online—and prices can stay elevated or rise further due to an expected diminishing supply of traditional fuels as more companies invest in and transition to cleaner alternatives. Together, we believe that these widening mismatches in supply and demand—fueled by a skyrocketing focus on ESG factors and climate neutrality—are likely to boost prices for commodities in the coming years.

1 Source: Bloomberg Commodity Index

2 Source: World Resources Institute

3 Source: Rystad Research

4 Source: https://nickelinstitute.org/about-nickel-and-its-applications/#03-nickel-mining-production