Germany’s Fiscal Shift: It’s a Big Deal

Executive summary:

- Germany is taking the handbrake off its fiscal policy, and we believe this will have significant implications for European economic growth and financial markets.

- The direct growth impact of the fiscal package on German GDP will not be felt until 2026 due to implementation lags, but we expect there to be an enduring impact that extends beyond 2027, with spillover effects outside Germany.

- Financial markets cheered the arrival of the fiscal package. The German stock market index DAX had already outperformed global peers in 2025, but rose further on the news, as did the euro.

- In our view, a potential sell-off in European assets in response to trade war escalation would be a buying opportunity. We view capital repatriation to Europe as benefitting euro area stocks and the euro in the long term.

Donald Trump and JD Vance managed what neither the Covid pandemic nor the Russian invasion of Ukraine were able to: make Germany ditch its fiscal restraint to ramp up spending on defense and infrastructure.

The importance of reforming the so-called “debt brake” to allow for greater public investments can hardly be overstated. This blog looks at how the policy shift came about and its implications for European economic growth and financial markets.

A watershed moment

A pivotal moment in Germany’s reassessment was the televised meeting between U.S. President Donald Trump and Ukrainian President Volodymyr Zelenskyy on February 28, 2025. The encounter in the Oval Office quickly escalated into a heated exchange and signaled a shift in U.S. foreign policy priorities. It became clear to politicians in Berlin and Brussels that Europe could no longer rely solely on the American security umbrella.

For Friedrich Merz, the soon-to-be chancellor of Germany, this confrontation was a watershed moment. Europe’s largest economy had to assume greater responsibility for its own security and economic resilience. Having resisted a reform of the “debt brake” for years while in opposition, it took him four days to hammer out a deal to reform the balanced budget rule. His future coalition partner, the SPD, had already argued for a change to the budget rules to allow for greater investment in infrastructure and defence.

To implement the plan, constitutional amendments were necessary. Merz’s CDU/CSU (the Union parties) and the SPD secured last-minute backing from the Greens for the required two-thirds majority in Germany’s lower house, the Bundestag. In a break with convention, the three parties used their votes in the outgoing Bundestag to pass the package as they would not have had the required super-majority in the newly elected parliament.

- An exemption of defense spending (over 1% of GDP) from the debt brake, essentially uncapping defense.

- A €500bn infrastructure fund deployed over 12 years, of which €100bn will immediately be chanelled into the Climate Transition Fund (a concession to the Greens).

- The remainder of the fund is for additional infrastructure investments, with €300 billion for the federal government and €100 billion for state governments.

- State governments will be allowed to run annual deficits of up to 0.35% of GDP.

Debt brake origins

Instituted in 2009 amid the global financial crisis, Germany's debt brake was enshrined in the constitution to ensure fiscal discipline. This rule mandated balanced budgets for both federal and state governments, permitting only minimal structural deficits—capped at 0.35% of GDP for the federal government. The intent was clear: safeguard future generations from the burdens of excessive national debt.

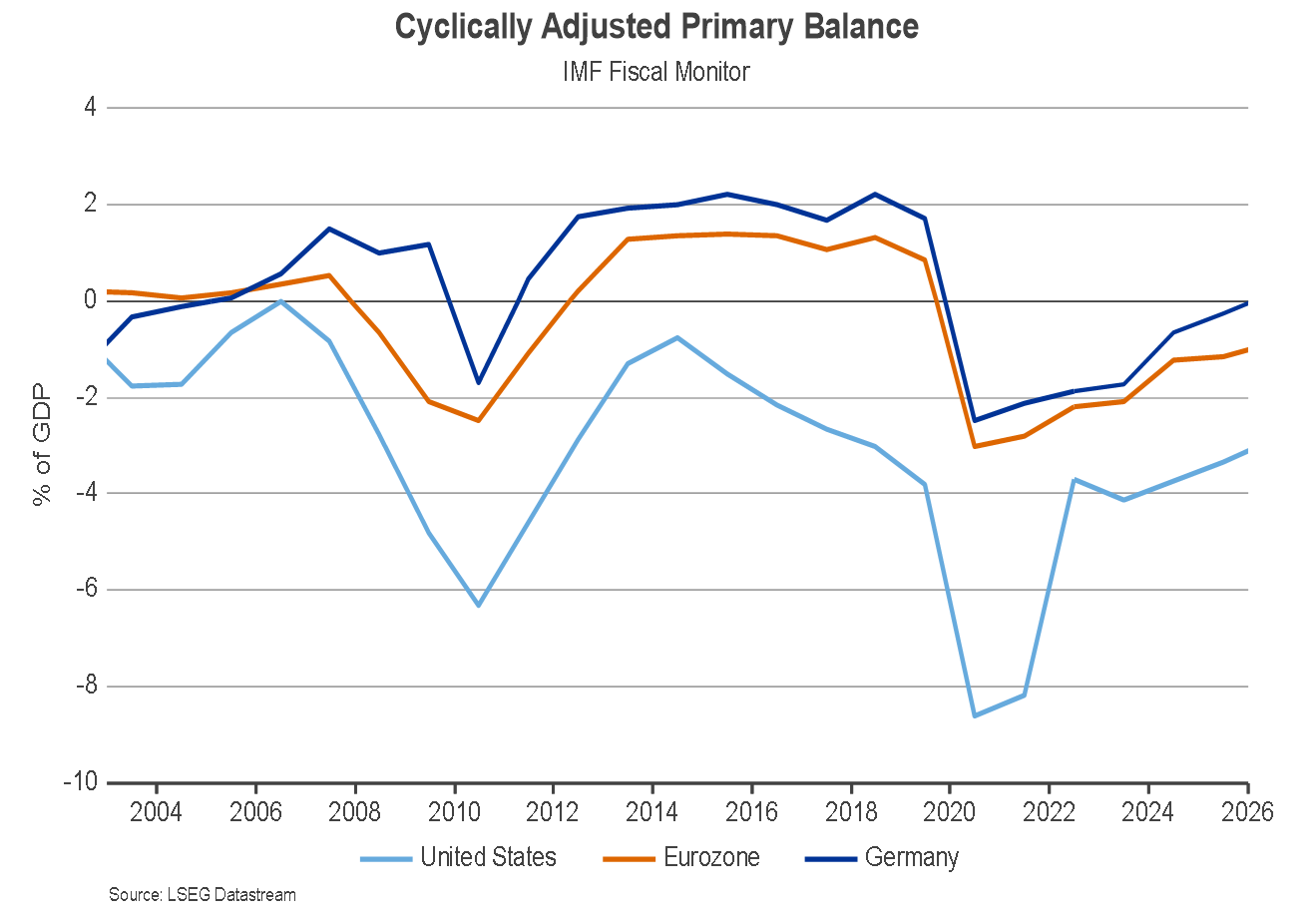

Germany has long been a proponent of fiscal restraint under the EU’s Maastricht rules, but its own debt brake went further than that. Despite having comparatively low and stable government debt of 60% of GDP, Germany ran substantial primary budget1 surpluses between 2011 and 2020. Berlin loosened the debt brake in response to the Covid pandemic and Russia’s invasion of Ukraine, but this was only a temporary departure from fiscal discipline.

Fiscal restraint in Germany vs largesse in the US

The chart above contrasts that restraint with fiscal largesse in the US, with the divergence starting at the onset of the 2007-2009 Global Financial Crisis. Looser fiscal policy arguably contributed to faster economic recovery from the pandemic but also left the United States with debt-to-GDP of around 120% (although some of the debt is held by the Federal Reserve and other government agencies).

Impact beyond growth

The direct growth impact of the fiscal package on German GDP will not be felt until 2026 due to implementation lags. Defense procurement has a long lead time and arguably a low multiplier of about 0.5, i.e. for €1 of defense spending GDP grows by €0.5. This is because some defense procurement will benefit military equipment producers outside of Germany. Infrastructure spending has a higher multiplier but also takes time to come to fruition. Therefore, the fiscal package will have no noticeable growth benefit this year. For 2026 and 2027, investment banks have penciled in an increase of 0.5% to 1.0% for Germany GDP growth.

My own sense is that the ripple effects from the fiscal package will have an enduring impact that extends beyond 2027 and have spillover effects outside Germany. The most under-appreciated aspect is on international capital flows. Since German unification in 1991, the country has run large, growing trade surpluses and persistently exported capital abroad. The U.S. has been a favorite destination for German and European capital. In recent years, euro area investors piled into the surging American stock market. A looser fiscal policy in Germany (and the euro area at large) will absorb a greater share of domestic production, reduce trade surpluses, and lower capital outflows. In addition, a greater sense of European solidarity may develop following the Trump administration’s foreign policy pivot, leading to “Buying European” and “Investing in Europe” movements.

Market reaction

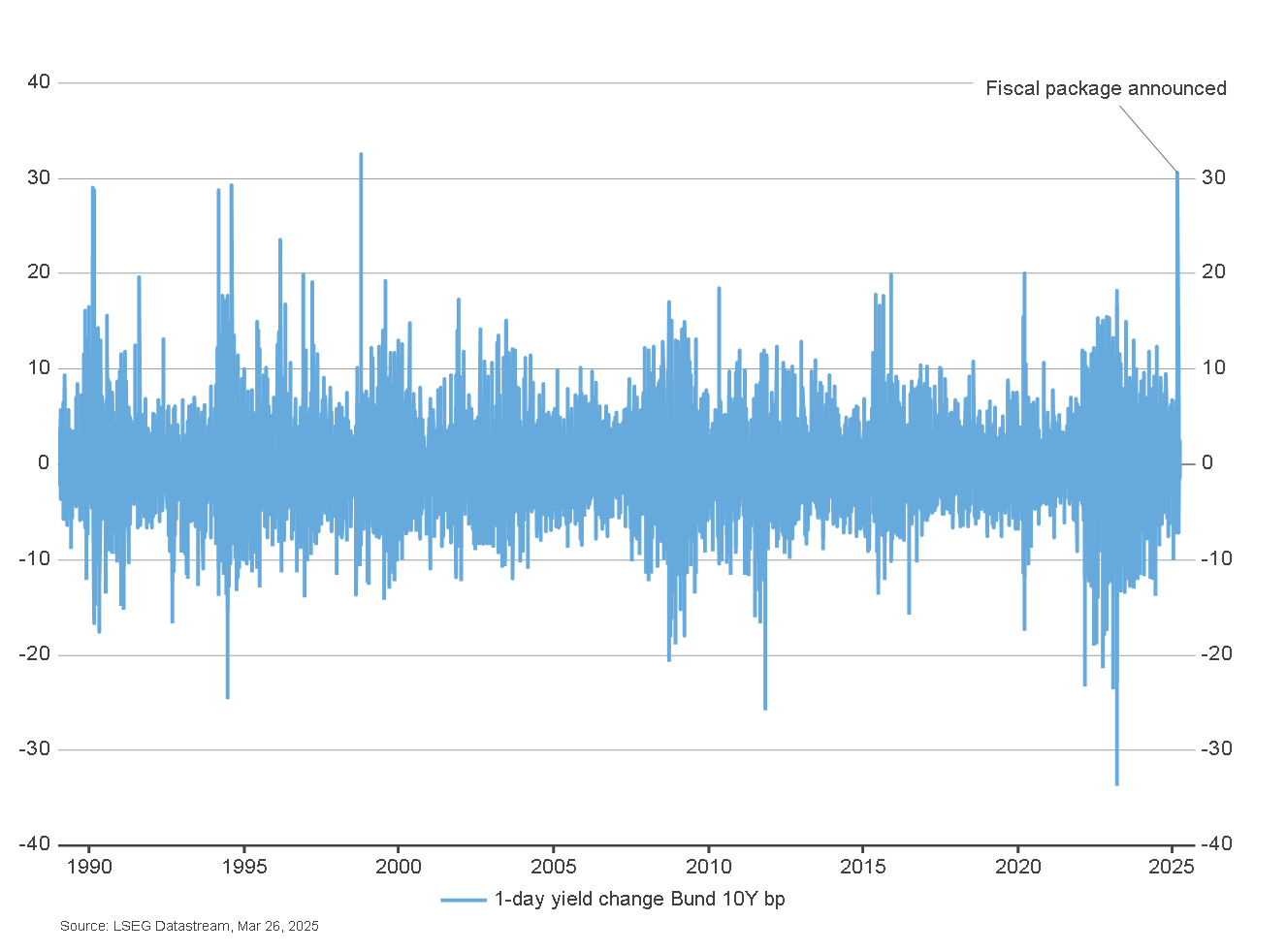

Financial markets cheered the arrival of the fiscal package. The German stock market index DAX had already outperformed global peers in 2025, but rose further on the news, as did the euro. The biggest movers by far were German government bonds (Bunds). On the day of Merz’s announcement, the yield on 10-year Bunds rose by nearly 30 basis points (see chart), the largest one-day increase since 1998. The cross-market price behavior suggests that market participants see the fiscal package boosting German growth and inflation substantially.

Bunds: Largest 1-day yield increase since 1998

For now, the rise in the German stock market and the EUR/USD exchange rate may have gone too far, too fast. The threat of new tariffs being slapped on the EU by Donald Trump on 2 April will shift attention to the short-term risks for the European economy. A potential sell-off in European assets in response to trade war escalation would be a buying opportunity, in our view. We view capital repatriation to Europe as benefitting euro area stocks and the euro in the long term.

The bottom line

Germany is taking off the fiscal handbrake. It’s hard to overstate the importance of this shift. While the direct growth impact from increasing public spending will only kick in next year, the confidence and capital flow effects work immediately. Together with the U.S. administration’s foreign policy pivot, loosening the fiscal shackles is likely to lower Europe’s trade surpluses and capital exports.

For markets, the impact of Germany’s fiscal shift could be most profound and enduring in international capital flows, diverting money away from U.S. capital markets and into investments in Europe.

1 The cyclically adjusted primary balance is a measure of a government's fiscal position that removes the effects of the business cycle and debt interest payments, providing a potentially more accurate picture of structural fiscal health.