June swoon: U.S. stocks slip into bear-market territory as inflation concerns rattle investors

After months of hand-wringing, U.S. indexes are now in bear-market territory across the board, down 20% from their most recent highs. The downdraft has been led by mega-cap tech, which has plunged 33% from its recent high. The concentration of the market cap of the S&P 500 Index in those mega-cap tech stocks has also led the U.S. equity benchmark into bear-market territory1. As of this writing, it is down 22% from its 52-week high, set on Jan. 3.

Inflation worries continue to spook markets

The principal driver of the ongoing weakness in markets continues to be inflation, which has haunted investors for the past several months. Initial observations of very high inflation spooked markets at the beginning of this year, triggering a decline that lasted through early March. The outbreak of the war in the Ukraine in late February helped contribute to this weakness, but ultimately its market impact dissipated. Most of this year’s market drop took place between early January and early March, with the S&P 500 Index closing down 13.5% on March 8. Since then, U.S. equity markets have largely been range-bound, occasionally teetering on the edge of bear-market status before rallying to higher ground.

The May U.S. inflation numbers changed that. Most market observers, us included, felt that March’s headline CPI (consumer price index) number of 8.5% would represent peak inflation. And for a while, that seemed to be the case, with year-over-year price increases slowing to 8.3% in April—still intolerably high, but in alignment with the narrative that inflation was slowly backing off. Last Friday’s reading of 8.6%, however, has caused the market to re-evaluate expectations.

The Fed’s commitment to lowering inflation

Statistically, May’s headline number wasn’t significantly any different than March’s—after all, it was only 0.1% higher than the 8.5% reading most had considered to be the peak of inflation. But the report demonstrated that inflation remains stubbornly high—and it’s this persistence of elevated pricing pressures, month in and month out, that now has the market spooked.

Where do all these observations lead us? Frankly, right to where we’ve been all along. We have known for quite a while that:

- Inflation is intolerably high.

- The U.S. Federal Reserve (Fed) is committed to bringing it down.

Friday’s May inflation report told us what we already knew: that bringing inflation down to a tolerable level—around 2%—is not going to be easy. Slowing down an overheated labor market to control inflation has a very large chance of spurring a recession. We think the Fed has been clear that it views inflation, and not a recession, as the greater threat to the U.S. economy. Why? Because while recessions hurt, they usually don’t last very long. Inflation, on the other hand, hurts and can last a very long time.

The recession/inflation balancing act

From my vantage point, this latest selloff is being driven by the market now understanding, to a greater degree, the difficulty of the task the Fed has before it. In other words, the Fed is already 75 (soon to be 125-150) basis points into the rate-hiking cycle, and inflation is still rising.

Investors should also recognize that the news cycle associated with successfully bringing inflation down will in itself be scary. Why? The Fed is trying to lower persistent inflation by cooling the economy—in particular, the demand for labor. The component of inflation that causes the most concern for the Fed is wage inflation, and that, too, is at an intolerably high level of 6% currently. What this likely means is that, if the Fed is successful in slowing demand, we’ll likely see a barrage of negative headlines related to slowing revenue growth, lower earnings growth, weaker GDP (gross domestic product), hiring freezes and so on. The market’s concern will then likely shift to fears that the Fed may go too far in its efforts—that if the central bank slows the economy too much, revenues will fall, earnings will plummet, hiring freezes will turn into layoffs and the economy will roll over into a recession.

While all of this may very well happen, right now the fundamental economic data does not depict this. The U.S. unemployment rate is very low, at 3.6%. Current purchasing’ managers indexes (PMIs) are in expansionary territory and 390,000 jobs were added to the U.S. economy in the last month—and 6.5 million in the last year. In addition, corporate revenues rose in the first quarter, while earnings growth for the S&P 500 was up 9% on a year-over-year basis.

Right now, markets are caught in a tug-of-war between what may happen in the future—as a result of what the Fed does to control inflation—and what the current underlying economic data depicts. Today, as markets tumble, the what-may-happen-down-the-line scenario is winning out, but things could easily reverse tomorrow, as it will likely take a year-plus for all these projections to actually play out in reality.

It’s also important to keep in mind that the market looks ahead and discounts current stock prices by what it thinks will happen in the future. Currently, it looks as if investors believe that future bad news is more important than the current economic good news—and that’s what’s driving markets into bear-market territory. To be frank, it is very rare for a market to hold bear-market territory levels without a recession following in relatively short order. Our view is that the most likely start of a recession is mid-2023, meaning that if we’re correct, there’s a chance the market could rally on the good news that a recession does not seem imminent.

One last point to consider here is that the market has already priced a mild recession into stock prices. In other words, if there is a recession, by how much more would equities actually sell off? It’s also worth pondering how bad the recession could be. Now, clearly short-term market returns can and likely will get worse if a recession actually occurs, but if the recession is relatively shallow, how long will it last? Could it only be for a few months? And if the market feels the next recession will be a shallow one, how bad would those short-term losses be?

Of course, we can’t answer burning questions like these with 100% certainty, but we do have some thoughts on the likely severity of a recession—were it to hit in the next year. Consider, for instance, that most deep and long recessions—i.e., the Global Financial Crisis—are a result of U.S. consumers (whose spending powers 70% of the nation’s economy) carrying too much debt going into the recession. That is not the case today. In fact, the overheated economy we are now currently experiencing is the result of consumer balance sheets actually improving during the pandemic-induced recession. Recall that consumers received large amounts of stimulus, yet could not leave their homes to spend the money. When consumers did start spending, a huge demand shock to inflationary pressures occurred. The result is that the U.S. consumer is actually in good financial condition today. This, in our opinion, bodes well for the severity of the next recession, and may help to put a floor on how far stocks fall in that scenario.

The bottom line

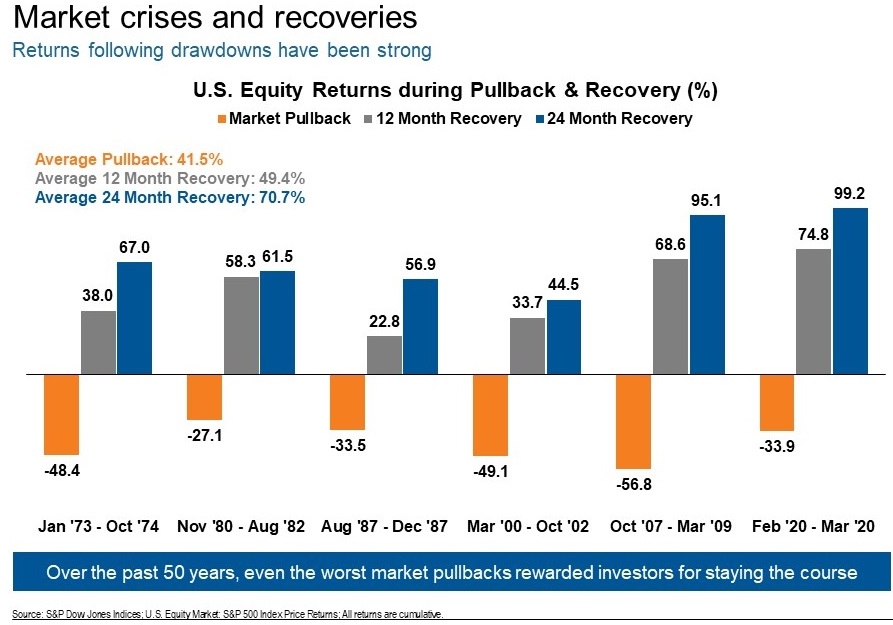

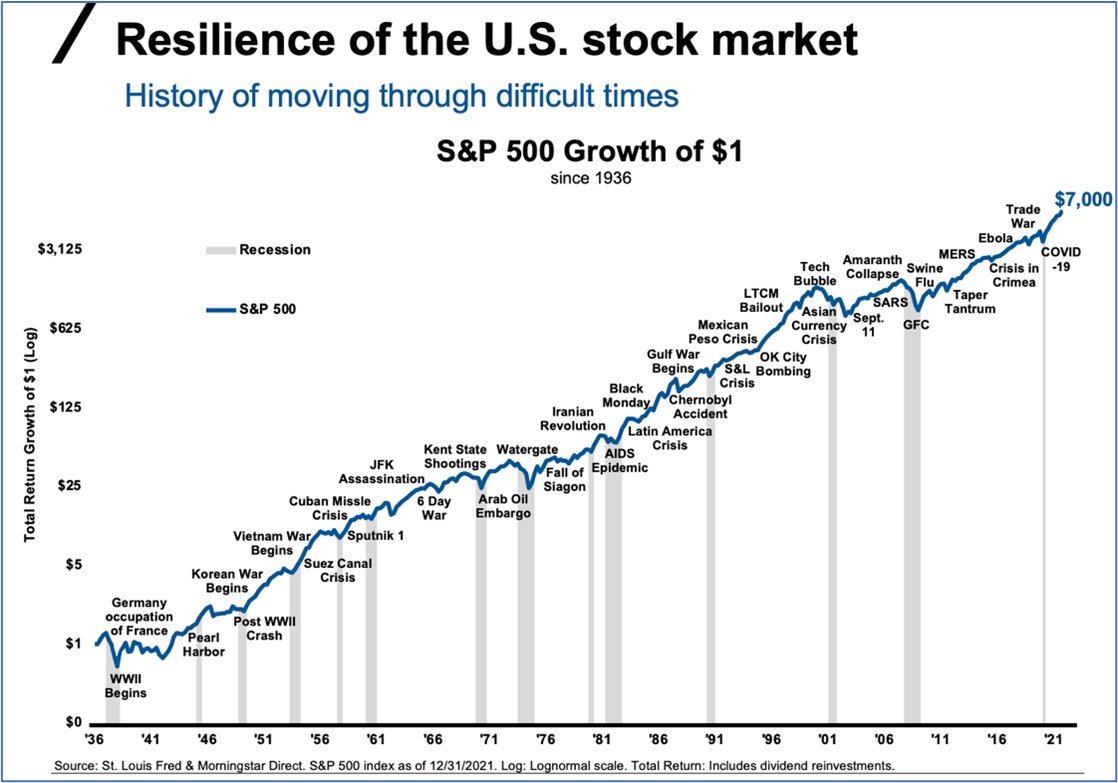

Unless you have a strong belief that you know which side will win, when it will win and how it will win, betting big on a specific outcome seems perilous. Remember that you have both an investment policy and a plan that were built specifically to fall back on during times of great uncertainty. This is one of those times. We know that staying disciplined in times of market turbulence is very difficult, but in order to make a move, investors should be confident that they see something that the market is not seeing right now. In our opinion, that is a very high bar to meet in times like these. At this point, the market has likely priced much of the unsettling things mentioned in this article already. Better to stay calm—and stick to your plan.

1In USD as of June 13, 2022.