Neighborhood watch: Impact on Canada of U.S. election

U.S. elections are of global relevance and perhaps even more so for Canada due to our close economic ties. While certain loose ends still need to be tied up, Democrat Joe Biden has been proclaimed President–elect; however, he may be governing with a divided Congress. Republicans are likely to hold on to a slim majority in the

Senate—depending on the outcome in Georgia’s two runoff elections in January—while the Democrats maintain control of House of Representatives. A divided, or a gridlocked, Congress means measured policy changes in 2021. Specific to Canada, we believe the biggest impacts a potential Biden presidency will have on Canada is in trade, energy and fiscal stimulus. We review the implications below.

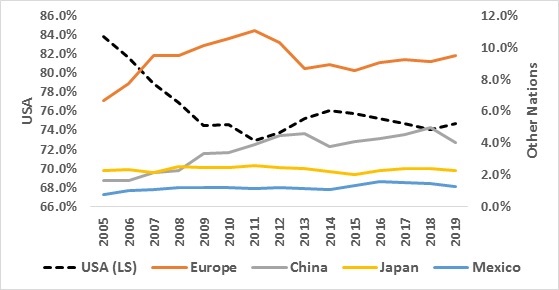

- Trade1– The ratification of a new North American trade agreement, the CUSMA, the successor to NAFTA, means U.S.-Canada trade tensions won’t dominate the next presidential cycle. Trade, nonetheless, is a focal point. Buy America policy geared towards resurrecting U.S. manufacturing was an objective under President Donald Trump and is expected to remain so under a Biden administration. This means Canada must continue to diversify its trading partners. To that end, some progress has been made but much work remains. As Chart 1 shows, U.S. share of Canadian exports has declined to 74% in 2019 from a high of 84% in 2005. Still, Canada is deeply dependent on the U.S. as a destination for its exports. Trade tensions may not resurface. However, the need to deepen the penetration of Canadian exports into Europe and Asia is essential.

Chart 1: Canada exports by region

Click image to enlarge

Source:Statistics Canada, Russell Investments. Annual data as of 2019.

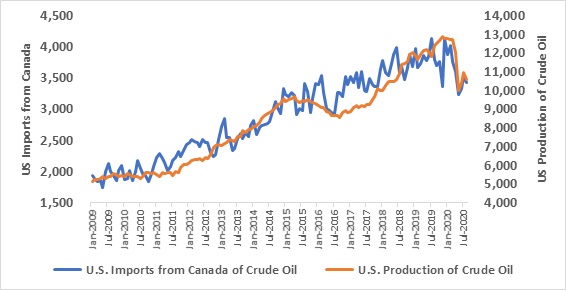

- Energy – Two trends upending the Canadian energy sector is the push towards renewables and the U.S.’s transformation into an oil-producing force. Despite these trends, U.S. dependence on imported Canadian crude oil has not lessened. See Chart 2. Notwithstanding the demand destruction due to COVID-related lockdowns and the subsequent reduction of economic activity, U.S. production has increased alongside imports of Canadian crude oil. It is worth noting, however, Canada (and Mexico) have benefited from the loss of heavy crude supplied by Venezuela to U.S. Gulf Coast refineries. Nonetheless, sustained demand is reassuring, considering 98% of Canadian crude oil exports are destined for the U.S. Still, there are concerns both immediate and longer term:

- The fate of the Keystone XL pipeline will once again be in flux. President-elect Biden has threatened to reverse President Trump’s approval of the elusive project. The completed pipeline is deemed an essential conduit necessary to release landlocked Canadian crude oil to U.S. refineries.

- The push towards renewables and electronic vehicles is a structural trend which may accelerate under a Biden presidency.

- Stimulus – Fiscal stimulus in the U.S. helps the Canadian economy, but the net effect might not be as strong as the headlines suggest. Based on Capital Economics2 estimate, fiscal stimulus that boosts U.S. GDP (gross domestic product) by 1% may raise Canada’s GDP by a more modest 0.1%. In other words, for U.S. stimulus to be of consequence north of the border, it must be substantive. With the odds tilted toward a gridlocked Congress, the likelihood of significant fiscal stimulus boosting U.S. growth has declined, and therefore any effect on the Canadian economy may be tempered. The burden then falls on the Canadian government to provide the necessary fiscal support the economy requires.

President Trump’s openness towards the energy sector improved the U.S.’s attractiveness relative to Canada as a destination for energy investment. The decision by Encana (now Ovintiv) to move its headquarters from Alberta to Colorado epitomized that sentiment. Paradoxically, a new political environment in the U.S., one potentially more hostile toward carbon emitters, could change sentiment toward Canada as a destination for energy investment. Or, at a minimum, it could force Canadian energy companies to reconsider their U.S. investment plans in favor of Canada.

Chart 2: U.S. imports of Canadian crude oil vs U.S. crude oil production

Click image to enlarge

Source:US Energy Information Administration, Russell Investments. As of August 2020. Oil data quoted in thousand barrels per day.

What seems clear is the impact of a Biden presidency on Canada is not straightforward. At a minimum, the Biden-Trudeau relationship may be less fractious considering the two have developed a rapport from President-elect Biden’s tenure as the vice president under the Obama administration. Ultimately, what might be more impactful is how Canada can adjust, adopt and improve competitiveness in a changing landscape.

Market Implications

The prospects of a gridlocked Congress mean major policy changes are looking less probable. As we discussed above, the net impact of a new administration in the White House is a nuanced one for Canada. The path forward then for the markets will depend on the business cycle. We believe the global economy is in early stages of an economic recovery with exceptional support from global policy makers. Although the virus remains the greatest threat to the recovery, the positive vaccine news from Pfizer on November 9, 2020 and from Moderna on November 16, 2020 is encouraging. Equity markets bottomed March 23rd, 2020 with the pandemic trade emerging victorious as technology–themed large cap companies were rewarded.As the recovery continues, we believe a reopening trade will emerge. Greater mobility that implies broader economic activity is likely to favor the value factor and cyclical sectors. Expanding global growth should also benefit international markets.

A pro-cyclical outlook also supports the Canadian dollar. A strong currency improves purchasing power of Canadian businesses and households, but it can also be a hindrance to the competitiveness of Canadian exports. This will not be lost on the Bank of Canada (BoC). A CAD/USD exchange rate that becomes too restrictive will likely be matched with a response from the BoC. Restating the obvious, both fiscal and monetary policy will be central to the outlook.

The elections were a source of potential volatility. With that now in the past, the focus is on the business cycle recovery, which is in the early stages—a phase that tends to be supportive of financial markets.

2 Capital Economics, Canada Economics Update, October 27, 2020.