The Value of an Advisor: How advisors deliver value in challenging times

If there were ever a year when the value that an advisor provides their clients was clear, then 2022 was it. There was plenty of market turbulence as the Bank of Canada and other global central banks rapidly hiked interest rates to clamp down on rampant inflation. There were ongoing geopolitical tensions, easing of Covid-19 pandemic restrictions, protests in Iran, a reduction in oil production and China unveiled a new economic modernization plan. It was one of the few years in recent memory where both equities and fixed income declined simultaneously.

To say the least, it was a challenging year for investors! But at Russell Investments we believe that investors who worked closely with their financial advisor were able to navigate the turmoil more easily. And we believe that the guidance advisors provided represents significant value to the bottom line of investor portfolios.

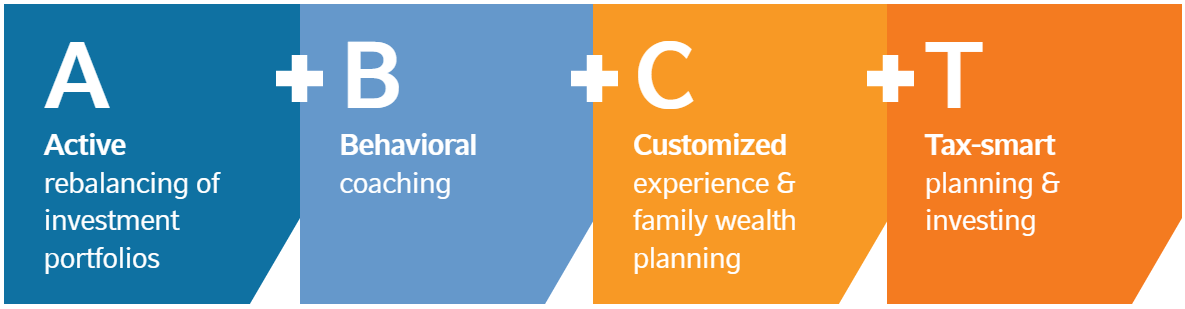

Every year we produce a Value of an Advisor study that quantifies the value advisors bring to their clients through a simple formula:

Our formula for 2023 is: A + B + C + T

Let’s look at each of those components and how an advisor who provides those services would have helped their clients through the turmoil of last year.

A is for Active rebalancing of investment portfolios

Markets can be volatile. And in 2022, they were not only volatile, but we also discovered that fixed income may not always play its traditional role as a counterbalance to equity, or a portfolio ballast in generating income. We found that inflation and higher interest rates have a different impact on different asset classes. In many ways it was an unusual year: it was only the third time in the last 50 years that both equities and fixed income declined.

This may seem like an argument against regular rebalancing. Historically, rebalancing to targeted weightings for different asset classes would typically cause an investor to sell equities and buy more fixed income. Usually that would help protect the investor from a drawdown in equities as bonds have traditionally been more stable. But in 2022, as both asset classes fell, the value of active rebalancing was not so much about improved performance nor less volatility – which are two of the potential benefits of rebalancing – but about maintaining the investor’s risk-return profile.

For example, a typical “balanced” portfolio of 60% equities and 40% fixed income purchased at the start of 2002 would have looked more like a growth portfolio by the end of 2022 if it had not been actively rebalanced over the period. That means it would be more susceptible to any future equity market drawdowns than the investor had originally intended. As the markets return to their traditional roles of equities providing growth and fixed income providing steady income, the unbalanced portfolio would no longer meet the investor’s risk profile.

Click image to enlarge

For illustrative purposes only. Not intended to represent any actual investment. Source: Russell Investments. Analysis based on data from 1/1/2002 - 12/31/2022. Initial asset allocation: 20% S&P/TSX Composite Index (Canadian equity), 20% S&P 500 Index (US Equity), 20% MSCI EAFE Index (Foreign Equity), and 40% FTSE Canada Universe Bond Index (Canadian Fixed Income). Indexes are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

Maintaining the allocation of assets within the original guidelines keeps the portfolio aligned with the investor’s stated risk tolerance and expectations for their money. This will help keep the investor on track and reasonably comfortable.

But we believe there are two reasons that many investors don’t rebalance their portfolios if left to their own devices:

- Because it’s an easy thing to forget to do. Investors know they’re supposed to do it. We also know we’re supposed to regularly change the batteries on our smoke alarms. But do we really do it?

- Because rebalancing essentially requires the investor to sell their winners to buy losers. Who wants to do that? For most people, it would go against their instincts.

This is why we believe rebalancing is such an important part of an advisor’s overall value. It ensures that the asset allocation of a portfolio remains close to its original target and therefore continues to reflect the investor’s desired risk profile.

B is for Behavioral coaching

We believe behavioral coaching is one of the most vital parts of the formula and where financial advisors add significant value for their clients. Left to their own devices, many investors buy high and sell low. Those kinds of behavioral mistakes can cost them.

Helping your clients avoid pulling out of markets at the wrong time and sticking to their long-term plan is one way that advisors provide substantial value.

Let’s look at the graph below. It shows how important it is to remain invested through thick and thin. Investors who fled the market when the Covid-19 pandemic began to spread in March 2020 had a hard time finding a new entry point over the following year as stocks rebounded quickly. By the end of 2022, those who had remained invested through the ups and downs were ahead of those investors who initially succumbed to fear, but eventually returned to the market. And those who retreated when the pandemic emerged and never returned? Well, the real value of their initial investment was squeezed by the soaring cost of inflation in 2022.

Click image to enlarge

Fear impacts opportunity

Source: Morningstar Direct. As of December 31, 2022. In CAD. Balanced Portfolio: 60% MSCI World Index & 40% Bloomberg Canada Aggregate Bond Index. Cash: S&P Canada Treasury Bill Index. Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly. The performance shown does not include fees and other costs that would have reduced returns.

This is where you, the advisor, can be a valuable guide. Your role as a behavioral coach can go a long way to keeping your client invested and focused on the long term, rather than falling prey to their emotions when markets get volatile.

C is for Customized client experience and family wealth planning

Just as advisors guide their clients through volatile markets, they also guide them through their life changes and shifting priorities. And that has in turn broadened and deepened the services many of you provide today, especially since client expectations for service and personalization have grown.

We all like to feel special and we all love the personal touch. Part of the appeal of going out for coffee is hearing the barista call out our name, knowing that coffee was made to our personal preferences. And what is more personal than finances?

People’s lives usually become more complex over time and so do their needs. Advisors add considerable value by doing the hard work of shepherding a strategy from origination to outcome. Depending on the client’s personal circumstances, preferences and considerations, there can be a broad mix of complex factors that require expert knowledge and advice to evaluate the choices and trade-offs at play.

You may be regularly adjusting your clients’ investment plans to align with their changing needs as they move from accumulation to preservation to distribution. This may require consultation with the client’s spouse and potentially also with their children, depending on the nature and size of the assets.

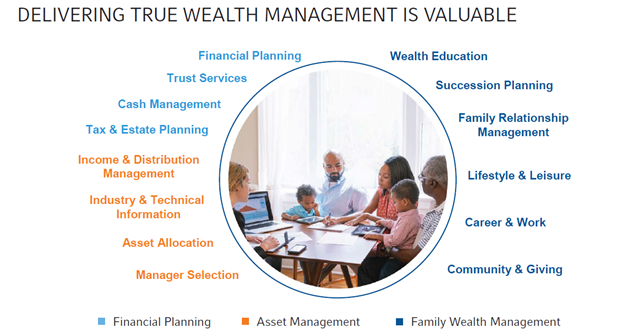

Moreover, in order to ensure a client’s personal needs are fully met, many advisors are calling upon a network of experts – such as estate lawyers, accountants or lifestyle consultants – to ensure the financial plan encompasses all aspects of the investor’s life.

The graph below shows all the services a holistic wealth advisor may now provide. The services listed in orange are what an advisor originally provided and what robo-advisors now offer at a very low price. Those in light blue are what a financial planner can provide, while those in dark blue are the broader and more customized services that many advisors now offer. We believe each holds value for an investor.

Click image to enlarge

T is for tax-efficient investing

It’s one thing to pay taxes on investments when markets have risen and the typical balanced portfolio has enjoyed a healthy return. But when portfolios decline – as many did in 2022 – and taxes are still due on those investments, well, that can feel particularly galling.

Without proper tax management, many investors may pay more taxes than they need to every April. And who wants to do that? There is a myriad of taxes that can be triggered by investments: taxes on dividends, on interest, on capital gain distributions, or on the sale of shares, for example. Tax-aware advisors who structure a portfolio in a tax-efficient manner and choose solutions that help minimize investment taxes can provide significant value

When you build and implement a personalized, comprehensive and tax-efficient portfolio for a client, you may help them achieve better outcomes. Deferring taxes into the future has the potential to significantly compound returns over time.

Click image to enlarge

For illustrative purposes only.

All examples shown are based on the following 2023 Ontario marginal tax rates for calculating the tax liabilities: interest income = 53.5%, Canadian eligible dividends = 39.3% and capital gains = 26.8%

An active tax-managed investing approach has the potential to lead to a much better after-tax outcome. We call the return that is lost to taxes “tax drag.” Tax drag is not only a burden that weighs on returns over time, but also an indicator that portfolios are not deploying proper strategies. As a tax-aware advisor, you can identify both the problem as well as the solution.

Tax-managed mutual funds aim to minimize distributions from non-registered accounts and they are now available to Canadian investors. These funds typically use tax-management techniques such as tax-loss harvesting, avoiding superficial losses and tax-smart yield management—all with the goal of helping to reduce the tax bite on a portfolio. After all, it’s not what you make, it’s what you get to keep.

Using a tax-managed approach can provide significant value to your clients and help you stand out from your peers.

The bottom line

Market volatility, economic downturns, rising interest rates, inflation and uncertainty make today’s investing environment incredibly challenging. At Russell Investments, we believe investors who work with advisors can more easily navigate that environment.

And we believe that working with an advisor may help investors increase the value of their portfolios. Through actively rebalancing portfolios to maintain the investor’s desired risk profile, through behavioral coaching, customized wealth management and tax-smart investing, advisors can help guide investors along their journey to financial security. We believe that has value.