Value of an advisor: T is for tax-smart planning and investing

Executive summary:

- Taxes on our investments – on dividends, capital gains and so on – are an inevitable part of the investing process. But we believe there are ways to minimize those taxes.

- Tax-smart advisors who consider taxes throughout the investment process can add value to their clients’ portfolios. Fewer taxes mean more money remains invested to compound and grow.

- Tax-smart advisors can stand out from their peers which may help build their business.

Earlier this year I was at a children’s birthday party and had the chance to catch up with some friends I hadn’t seen in a long time. During our conversation the normal questions were asked: “Gen, you work in asset management, right?” Once I explained what I do, I got the usual response. “So honestly, do you think working with a financial advisor is worth it?” I told them about the value that advisors provide by helping investors remain in the market through difficult times, by actively rebalancing their portfolios, diversifying their investments, and how they can help reduce the bite that taxes take. Once taxes came into the conversation, one of my friends chimed in and said, “Ah, I hate paying taxes, but it’s the name of the game. You have to pay when you’re making money.”

I had to agree with her, to a point. Paying taxes isn’t an enjoyable part of the investment process. But it doesn’t have to be a necessary part of the investment process.

A tax-smart advisor can help investors by considering the impact of taxes throughout the investing process, so that the investors don’t pay more taxes than they need to every April. These advisors keep in mind that there is a myriad of taxes that can be triggered by our investments: taxes on dividends, on capital gains, on interest income, or on the sale of shares, for example. These taxes can create a tax “drag” on the portfolio that impede its growth.

That’s why we at Russell Investments believe that tax-aware advisors who structure a portfolio to help minimize investment taxes can provide significant value. Indeed, our annual Value of Advisor study finds that tax-aware planning and investing is an integral part of the value that advisors provide.

Value of an Advisor = A+B+C+T

This is the fourth and last blog in our 2023 series, discussing why Russell Investments believes in the value of advisors, based on this easy-to-remember formula:

Click image to enlarge

In earlier blogs, we discussed the value of active rebalancing, the importance of behavioral coaching and the customized wealth planning that many advisors are now providing for their clients and often, their families.

In this blog, we’re going to talk about the T in our formula – the value of tax-efficient planning and investing. Because it’s not about what the investors make. It’s about what they keep.

Investment taxes are more noticeable in a low return year

Earlier this year, you probably had clients who were shocked that they had to pay taxes when their 2022 investment statement was negative. They may have asked you: “You mean I have to pay taxes even though my account was down?”. That’s because taxes on non-registered mutual funds – those held outside a registered vehicle such as an RRSP, TFSA, or RRIF can be triggered in various ways that have nothing to do with the fund’s overall performance.

For example, investments which pay income as interest, such as Money Market funds or Guaranteed Investment Certificates (GICs), are taxed at an investor’s marginal tax rate. Out of the various types of distributions, interest is taxed the highest.

Mutual fund unitholders can also be taxed on a fund's dividends, whether they are received as cash or reinvested in additional shares. Eligible Canadian dividends are taxed favorably (through dividend tax credits), whereas U.S. and foreign dividend income are taxed as other income (at an investor’s full marginal rate).

Moreover, when the fund sells stocks or bonds that have a gain, that gain must be passed along to all unitholders of the fund (unless it can be offset by a realized loss in the portfolio).

Most funds distribute capital gains near the end of the year. This means with most mutual funds, there are some capital gains to report each year even if no units of the fund were sold.

Mutual funds are similar to stocks in that the investor is a unitholder. Normally, when an investor sells units of a mutual fund, they will be taxed on any gains made during the holding period. When units of a mutual fund are sold for more than was paid for them, that will result in a capital gain. Selling your mutual fund units is in your control.

Click image to enlarge

For illustrative purposes only. All examples shown are based on the following 2023 Ontario marginal tax rates for calculating the tax liabilities: interest income = 53.5%, Canadian eligible dividends = 39.3% and capital gains = 26.8%. *Eligible Canadian dividends are taxed favourably, US and foreign dividend income are taxed as other income (at an investor’s full marginal rate).

But as I told my friend, there are ways to minimize that tax bite. For example, an investor with a similar portfolio in tax-managed mutual funds could potentially pay little to no capital gains taxes. Tax-managed mutual funds are designed to reduce or eliminate capital gains and dividends distributions. Investors who hold these funds have control over the tax year in which capital gains are reported. For example, they can choose to sell their shares of the fund in a year when they may have less income from other sources.

Tax-managed mutual funds aren’t the only way an advisor can help their clients reduce the taxes they pay on their investments. For example, an advisor who understands the different rates of taxation on different types of distributions can ensure that interest income is sheltered in a registered account. Or they can help structure a portfolio so that the distributions received from non-registered accounts are composed of Return of Capital.

Advisors who consider the impact of taxes on investments can bring a lot of value to an investor. An active tax-managed investing approach has the potential to lead to a much better after-tax outcome. We call the return that is lost to taxes “tax drag.” Tax drag is not only a burden that weighs on returns over time, but also an indicator that portfolios are not deploying proper strategies. A tax-aware advisor can both identify the problem as well as the solution.

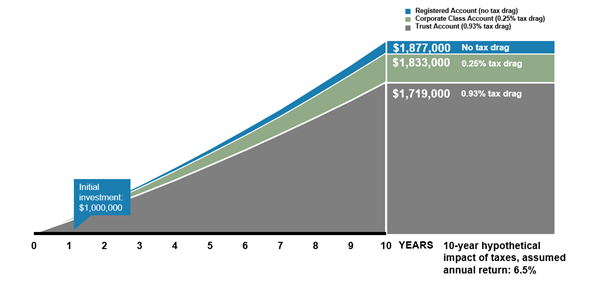

Let’s look at the graph below to see how tax drag impacts returns. A registered account is shielded from taxes until the funds are withdrawn, so investments held in one have no tax drag. Corporate class funds are structured so that the majority of distributions are in the form of Return of Capital. They do, however, pay taxes at the corporate level so there is a minimal tax drag on the investor’s returns. And a regular mutual fund, or trust account, has a larger tax drag. The graph shows how that drag could weigh on a portfolio over time.

Click image to enlarge

Source: Russell Investments

Assumptions: C$1 million investible amount. 6.5% rate of return for “Registered Account”, 6.25% rate of return for “Corporate Class Account”, 5.57% rate of return for “Trust Account”.

After-tax distributions are re-invested.

Tax “drag” is the difference between the returns on the “Registered Account” versus “Corporate Class Account” or “Trust Account”.

For illustrative purposes only, Not intended to reflect any actual portfolio or Russell Investments Canada Limited product. Percentages represent the difference in the gross return and after-tax return for trust and corporate-class mutual funds.

Tax-managed mutual funds typically use tax-management techniques such as tax-loss harvesting, avoiding superficial losses and tax-smart yield management—all with goal of helping to reduce the tax bite on a portfolio.

At Russell Investments, we have beaten the drum on how important tax-managed investing can be, because of its potential to help investors keep more of what they make. We believe this allows advisors to better serve their clients and may help advisors to set their practices apart.

When that fellow mom asked if a financial advisor was worth the cost, I pointed out that a savvy and tax-aware advisor can help her save more in taxes than she would pay in the advisor’s fee. I could see her doing the math in her head. And then she asked me if I knew any tax-smart advisors.

Understanding your client’s tax-sensitivity level

Are you a tax-smart advisor? To help you decide if you have a robust tax-smart investment approach, ask yourself these five questions:

- Do you know each client's marginal tax rate?

- Do you deliberatively offer distinct investment solutions for taxable and non-taxable assets?

- Do you explain to clients the benefits of managing taxes?

- Do you collaborate with local CPAs to minimize tax implications?

- Do you regularly review your clients' T3, T5, T5008 and other tax forms which cover distributions, income and capital gains (or losses)?

Communicating your value all year long

More importantly – do you talk about taxes with your clients all year, not just in April? At Russell Investments, we believe every season is tax season. For example, investors traditionally receive their T3, T4 and T5 forms, early in the year, while it’s still winter. Most tax filing deadlines fall in the spring, and we believe that after those deadlines have passed, it’s a great time for advisors to conduct a review of their tax status with their clients. This could offer the opportunity to structure their investments in a more optimal way to hopefully pay fewer taxes next year. In the summer, advisors have the opportunity to build relationships with Chartered Professional Accountants and review their clients’ portfolios for taxable assets that could benefit from tax management. And in the fall, advisors can discuss the potential impact of capital gain distributions on their clients’ investment returns and look for ways to address that impact.

Bottom Line

I think I was able to convince my friend that a financial advisor is worth the cost, even if all the advisor does is help the investor pay fewer taxes on their investments.

And there’s another thing to bear in mind. Using a tax-managed approach can help you stand out from advisors who don’t. We believe helping clients improve their after-tax wealth can be a great way for those tax-smart advisors to reinforce their value while potentially gaining new business. I’m pretty sure my friend is going to mention our conversation to her friends, who in turn may want to find a tax-smart advisor.

To learn more about the 2023 Value of an Advisor Study, click here.