What's driving the demand for listed infrastructure?

The U.S. House of Representatives recently passed a US$1 trillion bill to rebuild the nation’s ageing infrastructure. The new investment in infrastructure over the next five years, includes replacing and upgrading of bridges, roads, railways, public transportation, broadband, water and energy systems, and the energy grid. Meanwhile, the easing of the COVID pandemic is likely to spur increased air travel and the need to efficiently transport goods requires continual investment in infrastructure.

As the outlook for infrastructure investing improves, we have updated and republished a popular blog from a couple years ago on the factors driving demand for listed infrastructure. While the environment has changed in the past two years, these factors remain as relevant as ever.

Why listed infrastructure? Let’s follow the logic chain: Equity-market volatility, low fixed-income yields and increased economic uncertainty all stand as potential stumbling blocks that threaten to derail even the best-laid of plans. Amidst all of this, the value of investments that can offer potential for greater diversification and downside management—and also serve as additional sources of income as well as opportunities for growth over time—is becoming increasingly clear.

Perhaps nowhere is this more apparent than in the listed infrastructure asset class, which continues to draw the attention of investors seeking to capture its potential benefits in multi-asset portfolios. This is due in part to the increasing mainstream appeal of infrastructure investing, which has evolved significantly since the early 1990s. Back then, the market capitalization of the broad universe of publicly traded infrastructure companies was approximately US$500 billion. Today, it stands at approximately US$1.7 trillion.1 What exactly is powering this increased demand for listed infrastructure? We believe there are six key factors responsible.

1. Access to a global growth opportunity

Upgrading the world’s infrastructure will likely be a dominant theme over the coming decades. In fact, per a McKinsey Global Institute estimate, a staggering US$69 trillion will need to be spent on critical infrastructure by the year 2035 to keep up with projected global demand. In addition, given the cash-strapped positions of many governments and municipalities, there’s likely to be an increasing reliance on private capital to finance infrastructure spending needs.

Click image to enlarge

Source: McKinsey Global Institute, October 2017 “Bridging global infrastructure gaps”.

All figures in USD.

In addition to high-level spending requirements, there are also several structural growth themes at play across the infrastructure investment universe. For example:

Airports: Commercial air travel was severely impacted by the COVID-19 pandemic. It’s expected by 2023 that passenger numbers will reach pre-COVID-19 levels. Looking beyond, global air passenger growth could be in the range of 1.5 - 3.6% over the next 20 years.2

Wireless towers: Global growth in the demand for wireless data continues at a seemingly insatiable pace. Contributing factors include working from home during the pandemic, requiring increased support for stronger and faster internet connectivity, the implementation of 5G networks, increased smartphone usage, data-intensive applications that utilize live-streaming and/or video. Consider that in the U.S. alone in 2020, mobile wireless data traffic had a 208% increase since 2016, and Americans have driven a 108x increase in mobile data traffic over the past decade.3

Renewable energy: Limiting climate change, reducing carbon dioxide emissions and improving energy efficiency is also creating significant investment opportunities. Bloomberg estimates US$11.5 trillion will be invested in new power generation from now through 2050, with a significant portion of that being directed at renewables.4 At the United Nations energy summit in September, 2021, more than US$400 billion in new finance and investment was committed by governments and the private sector during the UN High-level Dialogue on Energy.5

In each of the examples above, owners of critical infrastructure assets are poised to benefit from positive structural trends. Given that sourcing growth opportunities in this late-cycle economic environment has become increasingly challenging, infrastructure presents a compelling choice.

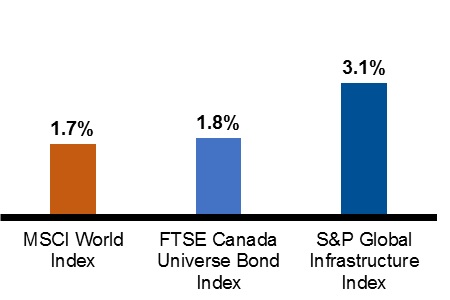

2. Enhanced yield potential relative to equities and bonds

While infrastructure investments have historically provided a relatively high dividend yield, just as importantly, they’ve also exhibited predictable and resilient cash flows. This cash flow resiliency across differing economic environments, as well as the ability to generate a steady income stream, is due to the fact that infrastructure assets provide essential services and typically operate in monopoly-like competitive positions.

Yields as of September 30, 2021

Source: Russell Investments, Bloomberg, FTSE and S&P Indices. Indexes and/or benchmarks are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. MSCI World Index represents world stocks, FTSE Canada Universe Bond Index represents Canadian government bonds, S&P 500 Global Infrastructure Index represents global infrastructure.

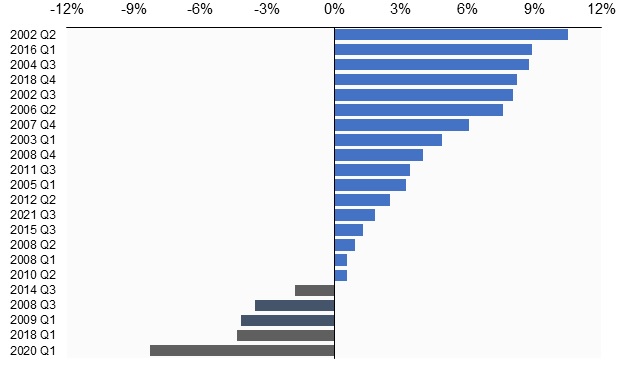

3. Diversification and downside protection

As a defensive alternative to equities, exposure to infrastructure can help manage total portfolio volatility, given its forecasted low correlations to stocks, bonds and real estate. Since 2001, infrastructure securities have outperformed global equities during 17 of the 22 quarters where the MSCI World Index experienced a negative quarterly return. On average, the S&P Global Infrastructure® Index has outperformed global equities by 3% per quarter during negative quarters. It’s this downside management and the potential to avoid the impact of negative compounding (remember, a $1,000 investment which loses 50% of its value has to return 100% to attain its original value) that is likely capturing the attention of investors.

Outperformance of S&P Global Infrastructure® Index (USD) Net Returns vs. MSCI World Index during quarters of negative equity market performance

Click image to enlarge

Source: Russell Investments; as of September 30, 2021. Russell Investments calculations. Indexes are unmanaged and cannot be invested in directly. Past performance is not indicative of future results. Returns in USD. MSCI World Index represents global equities and S&P Global Infrastructure Index represents infrastructure.

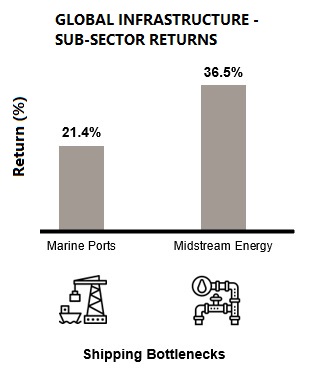

4. Uncertainty reigns

Global supply chain bottlenecks are reaching historic levels and have contributed to shortages of raw materials including energy (natural resources and infrastructure pipelines), shipping delays & record shipping container rates (with marine port backlogs & Industrial REIT warehouses benefiting). Given infrastructure assets can provide potential protection against inflation, help to provide essential services and have resilient cash flows, it stands to reason that they’re poised to do better than more cyclical investments in these uncertain times.

Supply/demand bottlenecks hit historic levels, benefiting infrastructure

Click image to enlarge

Source: Morningstar Direct, Factset. 2021 Year-to-date as of September 30, 2021, in USD. Infrastructure: S&P Global Infrastructure Index. Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly.

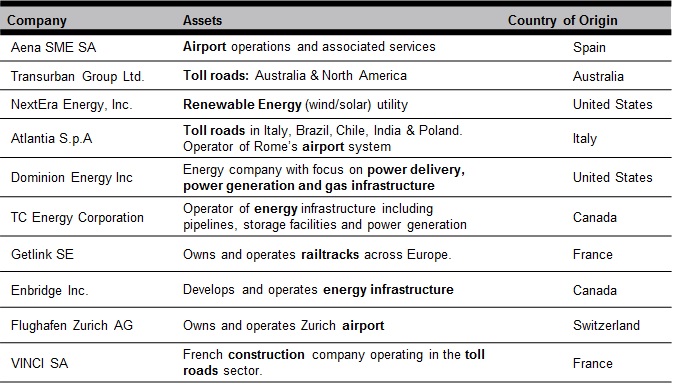

5. Access

A key feature of listed infrastructure is its ease of implementation. When compared to investing in infrastructure via private markets, potential benefits to investors include:

- Appropriate levels of geographic, sector and asset level diversification.

- Liquidity*. This enables the active management of an infrastructure portfolio to:

1. Potentially generate excess returns through stock and sector selection.

2. Provide ongoing risk management. - Lower fees.

Furthermore, many of the world’s leading infrastructure companies and assets are accessible only through public markets. For example, consider the chart below:

Click image to enlarge

Source: Russell Investments. *Liquidity is the ability for assets to be converted into cash and made available for reinvestment. This material is not an offer, solicitation or recommendation to purchase any security.

6. Private-market demand for listed infrastructure

Privatization of government infrastructure assets, larger private sector involvement in new projects and a significant replacement cycle present the potential for high growth in the global listed infrastructure asset class over the coming decade.6 While listed infrastructure indices are often highly concentrated in a few sectors such as utilities, power generation, and oil and gas equipment and services, these are still some of the sectors which private markets may access.

Bottom line

As we emerge from the COVID-19 pandemic, we anticipate increased air travel as borders reopen around the globe. The recent US$1trillion bill passed in the U.S. will desperately help rebuild an aging infrastructure network rife with the need for upgrades, and ultimately support supply-chain issues we are facing today in getting goods from A to B.

With ease of access and the potential for steady returns, we believe there’s no time like the present to consider exposure to listed infrastructure in a multi-asset portfolio.

1 Source: S&P Global Infrastructure Index as of October 29, 2021

2 Source: https://www.iata.org/en/publications/store/20-year-passenger-forecast/

3 Source: CTIA 2021 Annual Wireless Industry Survey, July 2021

4 Source: Bloomberg NEF, New Energy Outlook 2019, June 2019

5 Source: United Nations Sustainable Development Goals – Energy Summit, New York City, September 2021

6 Source: First Sentier Investors, “Global Listed Infrastructure”