Volatile times call for currency management

Volatile times call for currency management

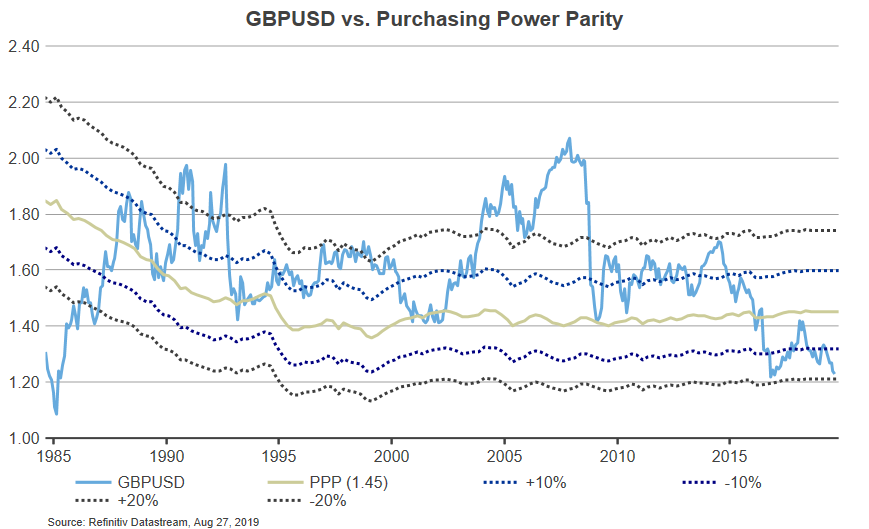

As the clock ticks down towards another Brexit deadline, the British pound has had several bouts of prolonged volatility since the vote in 2016, recently hitting a forty year low against the dollar.

-

Higher interest rates in the United States have supported the greenback

-

Brexit uncertainty has weighed on the pound

It’s difficult to know what the future will bring. Many investors won’t try to make money forecasting exchange rates buffeted by numerous political and economic variables.

However, investors who invest internationally don’t have any choice but to think about currency. Allocating to foreign assets allows investors to reap the benefits of international diversification, but also exposes them to currency risk. For example, a sterling-based fund which invests in global developed-market equities implicitly holds a long position in a currency basket consisting of roughly 67% U.S. dollar, 11% euro, 8% Japanese yen, 4% Canadian dollar and some other currencies1. That currency exposure is often a by-product of the equity position, not a clearly articulated investment which investors expect to earn returns from.

With sterling trading at historically low levels vis-à-vis the U.S. dollar, now is a good time for UK investors to assess the impact that currency exposures have on their portfolio risks. Investors that have so far been currency-unhedged and therefore benefitted from the strength of the U.S. dollar may consider hedging now to lock in these gains. Leaving currency risk unmanaged is not the best long-term choice, in our view.

Static or dynamic currency management?

Setting a strategic hedge ratio - and sticking to it - is a sensible approach to currency management. When compared to an unhedged position, static hedging often reduces unrewarded risk without giving up expected return (when looking at an appropriately long period).

Finding the optimal hedge ratio is difficult and can vary by asset class and base currency. Based on our analysis, we often recommend fully currency-hedging global fixed income portfolios to sterling- and euro-based investors. In international equity portfolios, it can strategically make sense to hedge currency exposures partially.

A different approach is to allow the currency hedge ratio to be flexible over time, with the aim of generating excess returns over a passive hedge. Hedge ratios can be adjusted to valuations, interest rates and other factors that drive currency returns. This dynamic currency hedging can turn the incidental currency risk from international assets into a rewarded source of risk.

When it comes to currency, don’t forget costs

Unmanaged foreign exchange (FX) transaction costs can easily erode returns generated by a hedging programme. Over the last decade, allegations of collusion and manipulation have been levelled at banks and other middlemen in the FX markets. In 2014, the Financial Conduct Authority (FCA) in the UK imposed fines totalling £1.1 billion on five banks for failing to control business practices in FX trading. The alleged market abuse resulted in higher transaction costs for investors.

Consequently, investors must carefully manage costs and maintain appropriate governance by taking the following steps:

-

Ensure their currency manager has a deep counterparty panel that allows them to access competitive quotes and liquidity. Competition allows the manager to complete trades and diversify exposure.

-

Insist on time-stamps for all transactions. Time-stamps allow an independent transaction cost analysis provider to assess the execution quality.

-

Employ an independent FX transaction cost analysis (TCA) provider. An FX TCA is an excellent tool that allows investors to understand execution costs and slippage. At the end of the day, what gets measured gets managed.

The bottom line

Investing internationally means currency is in play. It is unavoidable. Allocating to foreign assets may reap the benefits of international diversification, but also means exposure to currency risk. It’s time for European investors to assess the impact of currency.

________________________

[1] Based on market capitalisation weights. Source: MSCI, Russell Investments Calculations, as of 29 August 2019.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.