The coming fall of PPA funded status

The year 2022 was brutal for asset returns across most asset classes. A traditional 60/40 portfolio of global equities and aggregate bonds would have lost 16% during the year.1 Remarkably, pension funded status on a mark-to-market or accounting basis stayed about the same during 2022 for many plan sponsors, as pension liability values declined dramatically due to much higher discount rates. In a way, this made the asset losses during the year more palatable, but that's not the complete picture.

Background

Pension actuaries value liabilities for two broad purposes: 1) accounting and 2) funding. For accounting, liabilities are valued using current corporate bond rates. This is typically the rate used for daily monitoring and glidepath purposes as well.

For funding, the discount rate is heavily smoothed over time as required by pension law. Under this method, the discount rate must be within 5% of the 25-year average of corporate bond rates.2 This rate-setting process has had two immediate effects: 1) funding discount rates have been much higher than the concurrent market would have implied over the last ~10 years, and 2) rates are far more predictable than they would be otherwise.

The fact that discount rates are much higher for funding purposes has led to a significant decline in contribution requirements and fewer instances of "benefit restrictions" that may have limited the payment of lump sums or the ability to purchase annuity contracts from insurers.

Is this really pension funding stabilization?

Rates becoming more predictable was part of the design of this legislation, which is—somewhat ironically this year—termed pension funding stabilization, but it was really pension funded status elevation. It is helpful to have stable liabilities when assets are growing, which can boost funded status (on this basis), but in a year where portfolios lost 15% or more in value, a stable liability measure also leads to entirely unstable funded status. It is worth acknowledging that despite the large drop in funded status for funding purposes, it remains higher than if pension funding stabilization had not been introduced. Using a basis that is keyed off 25-year averages leads to the inability of investment managers to hedge changes in liabilities with liability-driven investing (LDI) strategies, making contribution requirements less predictable. In reality, the hope of this funding legislation was to make funding requirements lower, and using a higher, smoothed discount rate does typically accomplish this purpose. However, if rates were to move above the corridor, it is unlikely that sponsors would appreciate the rate stability.

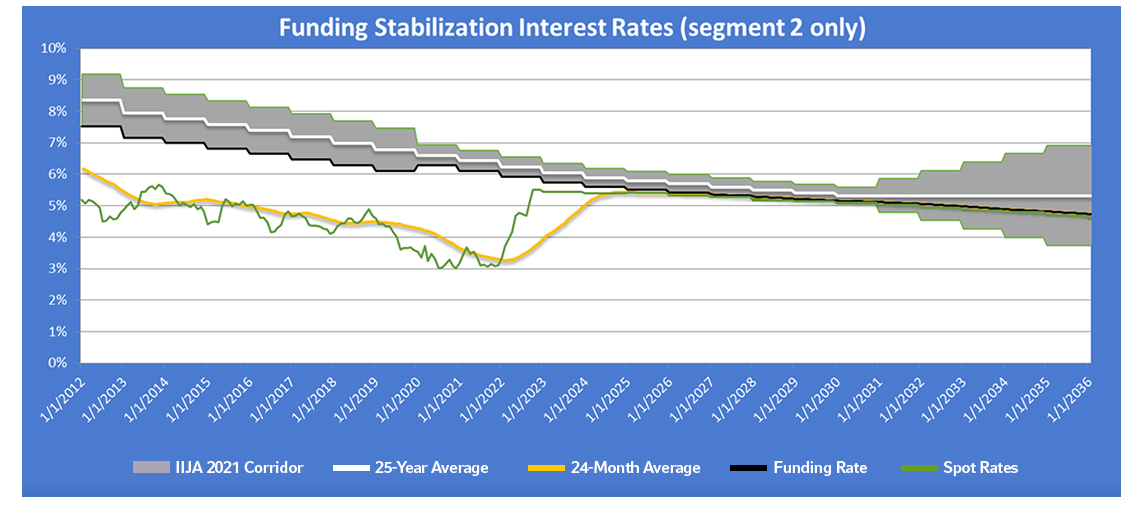

The exhibit below shows the history of funding discount rates since pension funding stabilization was first introduced with MAP-213 in 2012. The dramatic jump in spot discount rates over 2022 is evident, nearing the 2023 corridor. For the first time, rates used for funding purposes may intersect with spot (market) rates in the next year or two. This means that funding and accounting funded statuses are expected to converge, rather than the funding funded status being elevated relative to the market-based accounting funded status.

Click image to enlarge

2023 funding reports will be different

What do the 2022 asset losses all mean for pension plan sponsors? In short, they will lead to a higher probability of contribution requirements and benefit restrictions. In my experience, sponsors don't appreciate being caught by surprise, and this is one surprise everyone should try to get in front of.

Contribution requirements are designed to fully fund defined benefit plans over a 15-year period. The amount the plan sponsor pays is directly related to how well funded the plan is based on the smoothed rates shown above. The funded status on this measure almost universally declined during 2022, although funded status calculations for funding purposes will not be finalized until later in 2023.4 For clients that were just above 100% on a funding basis as of January 1, 2022 (for calendar year plans), they may find they have a contribution requirement in 2023, when they might not have in recent years. If the plan was underfunded, the minimum required contribution will likely increase.

Benefit restrictions were first introduced in the Pension Protection Act of 2006 (PPA). They were designed to prevent sponsors from making large payouts while the plan was poorly funded. Specifically, plans that are certified as being less than 80% on an "AFTAP"5 basis would not generally be allowed to pay full lump sums6 or purchase annuity contracts until funding improves. In the more extreme cases, if a plan falls below 60% funded on an AFTAP basis, it must immediately cease benefit accruals, effectively freezing the plan.

The AFTAP basis used for benefit restrictions is also determined with smoothed discount rates, which has led to higher AFTAPs and very few plan sponsors being subject to restrictions since 2012. Some less well-funded sponsors that either have an ongoing lump sum plan benefit option or were planning on a pension risk transfer (either lump sum window or annuity purchase) in 2023, may be restricted from doing so without contributing to certify an AFTAP above 80%, or separately fully funding the impact of the risk transfer.7

What can plan sponsors do?

While the hit on plan assets was large in 2022, most sponsors will not feel the full impact of the loss in 2023. This is because PPA allows for some asset smoothing—up to 24 months—with the smoothed asset value8 required to be within 10% of the fair market value. This will lead to using an asset value for determining funding requirements that is higher than the fair market value.

Also, even if contribution requirements do increase in 2023, they will not be fully due until 8 ½ months after the end of the plan year (mid-September of 2024 for calendar year plan years), although some quarterly contributions may be required throughout the year. This gives some time to budget for the cash needed. Also, many sponsors have built up credit balances (either carryover or prefunding balances) that can be used to satisfy contribution requirements. In addition, credit balances may be waived to help improve the funded status measure used in these calculations.9

We should also note that the calculation of the PBGC variable rate premium is different from the calculation of funding liabilities, as only a small amount of smoothing (up to 2 years) is allowed. In general, plan sponsors will not see as much of an impact on this measure in 2023. If sponsors have chosen the standard method of determining the PBGC liabilities (that uses spot discount rates), then this funded status measure will likely align with accounting funded status.

The impact on investment strategy

The case for an LDI approach to investing to stabilize and preserve funded status is well established. This approach is effective at achieving its objectives when the liability measurement is directly tied to a market-based discount rate approach, as is used for accounting. This approach does not, however, reduce funded status volatility for funding-related measures that have rates that are nearly known years in advance.

This distinction is less relevant for well-funded plans since the plan is unlikely to have contribution requirements regardless of the volatility of the funded status. For poorly funded plans, however, this disconnect can lead to contribution surprises. The best defense against this is to fund the plan more sufficiently, and to establish a well-diversified portfolio that will provide a stable investment return over time.

Ultimately, the economic cost of the plan—used for risk transfers, the balance sheet, and PBGC purposes—is based on market-related measures. This does not mean ignoring the impact of funding requirements—sponsors should be mindful of what contributions may be expected, but the ability to stabilize contribution requirements under current pension law is limited due to the nature of the liability calculation.

Moving forward

A significant uptick in asset returns in 2023 could reverse the impact of 2022's losses. However, this should not be counted on, and plan sponsors should be aware of what contributions could be required in the future under a range of potential scenarios, and consciously consider if they have the most appropriate investment and funding strategy in place relative to their objectives.

1 Assumed 60% in MSCI All Country World Index (ACWI) and 40% in Bloomberg US Aggregate Bond Index.

2 The 5% bands around the 25-year average would expand in 2031 until eventually reaching 30% bands. The bands used to be 10% until this changed with ARPA legislation in 2021.

3 Moving Ahead of Progress in the 21st Century Act.

4 The final funded status as of January 1, 2023 will take months to complete as part of the annual valuation cycle.

5 Adjusted Funding Target Attainment Percentage.

6 Partial/bifurcated lump sums may still be possible.

7 There are some timing considerations on the AFTAP and resulting benefit restrictions. For example, the AFTAP in place for the first three months of the year equals the previous year's AFTAP, and until the end of the ninth month, the actuary can assume the AFTAP is 10% lower than the previous year's AFTAP. By the end of the ninth month, however, actual data must be used.

8 Known as the Actuarial Value of Assets.

9 This is due to credit balances being required to be subtracted from the assets prior to the calculation of the funding deficit and FTAP/AFTAP.