How long will DB funding relief last?

Since 2012 and the passage of MAP-211, single employer defined-benefit (DB) plan sponsors have experienced lower contribution requirements. Unlike prior funding relief measures, MAP-21 and its successors—HATFA 20142 and BBA 20153—focused on changing liabilities directly by allowing higher discount rates. Higher discount rates lead to lower liabilities and thus higher funded ratios (used for contribution purposes). In fact, many sponsors have seen funded ratios 20-25% higher than they would have been without funding relief. This has significantly decreased funding requirements, but how long will the contribution holiday last?

Background

In simple terms, DB funding requirements are designed to fully fund the plan on a rolling seven-year cycle. Plan actuaries discount liabilities using the 24-month average of corporate discount rates supplied by the IRS4. In 2012, in response to significantly reduced funded status due to lower discount rates, Congress passed MAP-21, which added a rule that the funding discount rate needed to fall within 10% of the 25-year average of corporate discount rates. Since corporate discount rates have been trending downward for decades, this immediately decreased funding requirements. Lower DB contributions translates to lower tax deductions and additional tax revenue, which is ultimately what helped the law to pass. To further boost tax revenue, Congress included future increases in PBGC premiums.

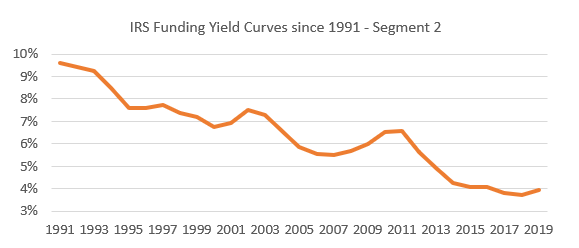

Corporate bond rates were much higher 25 years ago and have steadily declined over the that time, particularly since 2011, as shown in the following chart.

Figure 1: Source: IRS

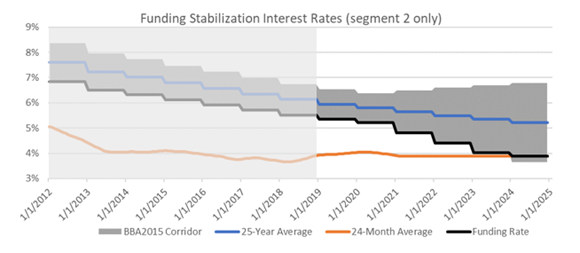

MAP-21 stated that the ±10% corridor would phase out to a ±15% corridor after one year, then to ±20% the next year and so on until a permanent ±30% corridor was in place. This meant that funding relief would have run its course by 2016. However, Congress delayed the corridor phase-out for three years with HATFA 2014 (retroactively for the 2013 valuation year), then an additional five years with BBA 2015. The full phase-out of the corridor is now expected in the year 2024, as shown here:

Figure 2: Source: IRS

Seven years after funding relief first passed, despite the 25-year average rate falling each year, underfunded DB sponsors (on an accounting basis) still enjoy low (or nonexistent) contribution requirements and higher funded ratios on a contribution basis. While this higher funded ratio does not change the marked-to-market funded ratio, and does not help reduce PBGC variable rate premiums, it has provided sponsors with flexibility on when to pay contributions. In response, contributions across the DB industry declined for several years, until 2017 when Congress passed tax reform, providing an incentive for sponsors to increase contributions much more than in previous years.

Looking ahead

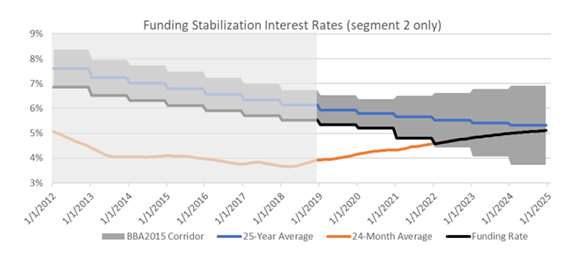

Given the declining pattern of 25-year corporate bond rates, and the expanding corridor starting in 2021, when can we expect that the effects of funding relief will wear away? The answer to this question completely depends on future corporate bond rates. If rates stay at current levels5, then it could be another four or five years until the standard 24-month average rate falls into the funding stabilization corridor, as shown here:

Figure 3: Based on IRS published rates and Russell Investments calculations, assuming that rates stay constant as current levels

The chart above illustrates approximately what the funding discount rate would have been without funding relief (24-month average), and what has actually been the funding discount rate since MAP-21 was passed in 2012. Once the 24-month average rate enters the corridor, then plan sponsors will effectively have funding relief behind them (though technically the ±30% corridor stays in place indefinitely, offering some ongoing downside management but also limiting upside potential for discount rates).

If we assume that future rates follow the median forecast using our strategic planning capital market assumptions, then the two rates could merge as early as 2022, as shown here:

Figure 4: Based on IRS published rates and Russell Investments calculations, assuming that rates follow the median capital market forecast

What does this mean for plan sponsors?

Regardless of the future path of corporate discount rates, sponsors can expect that funding discount rates will decline dramatically in the next three to four years, probably by as much as 100 basis points. This will lead to lower funded ratios used in contribution calculations, and potentially much higher contribution requirements than they are experiencing now. Absent another extension of funding relief (which is not currently being proposed in Congress), liabilities used for funding purposes will not look so deflated relative to marked-to-market measures, such as those used in accounting.

While methods for helping to manage downside risk in DB plans (such as LDI) have made practical sense for many years to help stabilize balance sheet (or economic) funded status, as contribution requirements start being more directly tied to marked-to-market measures, the plan assets will play a critical role in pursuing contribution stability and predictability. With higher contributions (necessitated through higher requirements) comes improved funding ratios, and sponsors will not want to lose the ground they have gained. We anticipate that sponsors will be even more keenly focused on adopting LDI strategies, following glidepaths and locking down fully funded plans in a hibernation state to maintain the funded status they have achieved.

1 Moving Ahead for Progress in the 21st Century Act of 2012

2 Highway and Transportation Funding Act of 2014

3 Bipartisan Budget Act of 2015

4 A full yield curve option without smoothing is available as well, but not used much

5 As of April 30, 2019 – the most recently published IRS rates