Equities are expensive. Bond yields are low. How can income needs be met? Enter model strategies.

For the final wave of baby boomers entering retirement over the next decade, a portfolio capable of producing steady income is paramount. You may have heard variations of these questions from your clients who are thinking about retirement: How much income can I take today? How do I increase the chances that my portfolio will continue to grow and produce income in the future? How do I manage the appropriate level of risk?

Threading the needle between those objectives is hard enough. Today’s environment adds low interest rates, uncertainty about the timing of future rate increases and the possible need to generate income for a long period of time. It’s easy to understand why the search for a consistent and reliable stream of income may be one of the biggest challenges facing advisors.

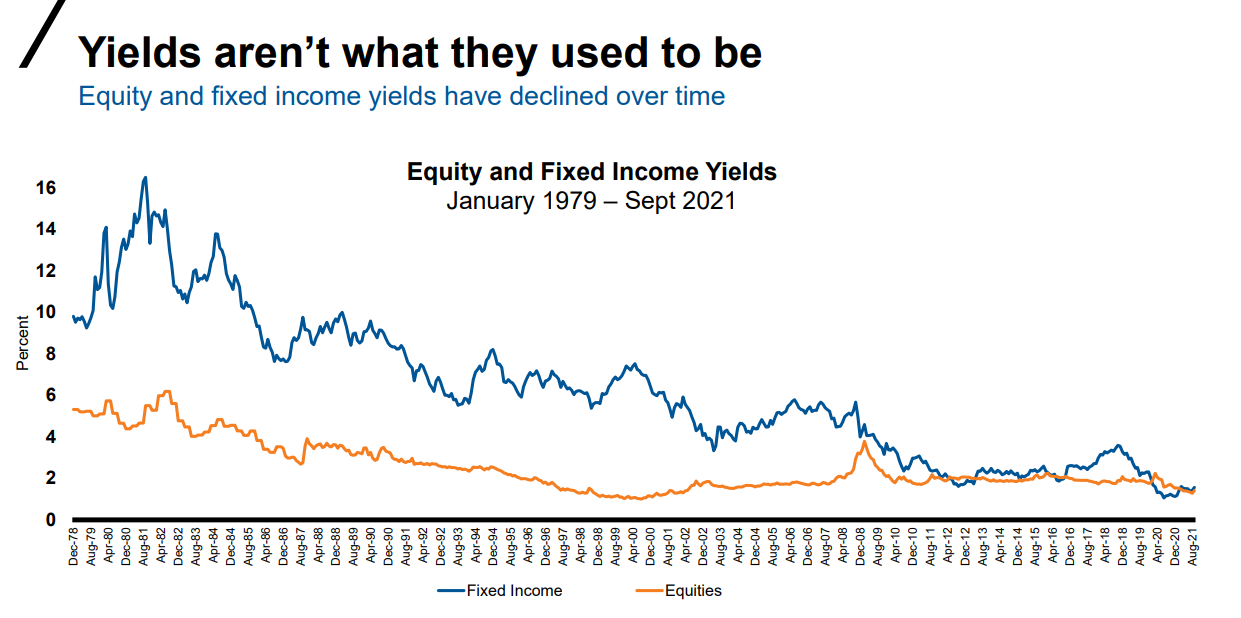

Income-seeking investors have encountered an interesting yield environment and increased risk for an extended period of time. Gone are the days of the early 1980s when investors could earn an 8-10% yield on a 60% bonds/40% equities portfolio1, or even the mid-2000s, when the 10-year U.S. Treasury yield stood at 6+%. Today’s 10-year Treasury yield hovers around 1.5%, similar to the dividend yield of the S&P 500 Index (see chart below). Investors probably need to look at broader opportunities for sources of income.

As an advisor, how can you help these clients? How do you generate income for them?

Diversification can be a first step to seeking additional yield while addressing some of those market fears. Investing in different asset classes beyond traditional equities and investment grade or government Treasury bonds can provide great sources of income. For example, global listed infrastructure, emerging markets debt, high yield bonds and MLPs (master limited partnerships) can offer higher yields than traditional stocks and bonds. Generally, yields improve when you move out on the risk spectrum. However, adding these alternative asset classes to a portfolio, while potentially helping improve income, may also lead to higher volatility, as demonstrated in the following chart.

Click image to enlarge

Cash: S&P 0-3 Month T-Bill Index; U.S. Treasuries: Bloomberg U.S. Treasury Index; Credit: Bloomberg U.S. Credit Index; Long Treasuries: Bloomberg Long U.S. Treasuries Index; Global Infrastructure: S&P Global Infrastructure Index; U.S Aggregate Bonds: Bloomberg U.S. Aggregate Bond Index; Global REITs: FTSE EPRA/NAREIT Developed Index; Emerging Market Debt: Bloomberg Emerging Markets Debt Index; U.S High Yield: Bloomberg High Yield Corporate Index; Global High Yield: Bloomberg Global High Yield Index; MLPs: Alerian MLP Index. Index returns represent past performance, are not a guarantee of future performance and are not indicative of any specific investment.

Some of these assets have provided one-year results that are scary, especially to those more conservative investors entering retirement years. This is where diversification and portfolio management expertise become invaluable to the process. Combining these higher income-producing assets into a portfolio mix that can generate a consistent income stream and a more consistent return pattern is the key to helping income investors meet their financial goals. If you’re not thinking about this today … you should. Your clients approaching or in retirement are likely to be focused on preservation of wealth while sustaining and generating income.

What’s the solution?

As an advisor, how do you best approach this challenge of managing income portfolios? Many of these asset classes (global infrastructure, emerging markets debt, etc.) are not typical exposures found in a lot of investor portfolios, especially more conservative ones seeking income. The risks and performance patterns of these asset segments are unique and it may take time for you to come up to speed. It takes a while to better understand the characteristics and best ways to implement such strategies. For example, how much of the portfolio? How big an allocation? What correlations are there with other asset classes? And, active or passive? Advisors have a couple of options: rapidly ramp up that learning curve, on top of all other client activities, or look to partner with an outsourced investment provider.

Consider partnering with a provider that can provide model strategies designed to generate income. These models can make it more practical to implement an income outcome-oriented approach across the client base:

- Models can free up advisors' time for additional consulting on financial needs.

- Models are engineered toward designated investment outcomes and avoid artificial performance chasing.

- Models are insightfully diversified, creating a more consistent return pattern that keeps investors from making bad moves during volatile times.

- Models are designed to manage the downside risk, which we believe leads to better investment outcomes.

As our colleague Mike Smith has noted: “Model strategies grant advisors the advantage of providing professionally managed investment solutions while refocusing the time and resources necessary to nurture and grow client relationships—the lifeblood of any practice.”

Studies have shown that advisors who outsource investment management to an asset manager like Russell Investments can save 7.7 hours a week on research and stock picking (among other tasks).2 That gives them an extra day every week to better engage with clients, uncover hidden assets, retain assets with existing clients or close new business—not to mention the time available to invest back in a better work-life balance or their families.

The bottom line

In today’s low interest-rate environment, it’s challenging to create a portfolio that meets investors’ income needs. Advisors can help achieve this through adopting a models-based approach targeting current and future income needs—specifically, a model strategy that provides exposure to a diverse combination of income-producing and growth assets that can navigate the challenges confronting investors looking for long-term income production. For advisors with clients that would benefit from such portfolios, Russell Investments has solutions to aid in that transition.

1 Hypothetical portfolio represented by 60% Bloomberg U.S. Aggregate Bond Index, 40% S&P 500® Index.

2 Source: https://static.twentyoverten.com/5e0f642709752828dbb0c6e0/-mjyNOiwG/Outsourcing-Money-Management-article4.pdf, AssetMark, 2019.