Getting income from a portfolio is easier these days but risks remain. Model portfolios may be the answer.

Executive summary:

- Historically low interest rates in recent years made it difficult for investors who seek yield from their investment portfolios

- Rising rates in today's fixed income markets have led to more attractive bond prices and higher yields, alleviating some of the challenges facing income investors

- However, higher rates haven't eliminated all our income challenges as higher inflation has reared its ugly head. Advisors seeking to generate income and maintain spending power for clients may benefit from a professionally managed, diversified income model to meet those objectives.

Managing portfolio income has been challenging over the past decade or so as bond yields were historically low. This environment led some investors to seek income by tilting toward riskier assets as they reached for yield. However, bond yields are now beginning to normalize back to levels that offer higher yields and more attractive valuations than we've seen in years. This should allow investors to think along the lines of traditional, more core bond-oriented income portfolios, or does it?

In a low interest rate environment, the strength of a professionally managed, multi-asset income model is the inclusion of international stocks, global infrastructure, and high yield bonds provide higher yields than from core bonds alone. Now that core bonds are providing higher levels of income, are there still potential benefits to including these other risky assets in a diversified income solution? We still strongly believe "yes" and here's why.....

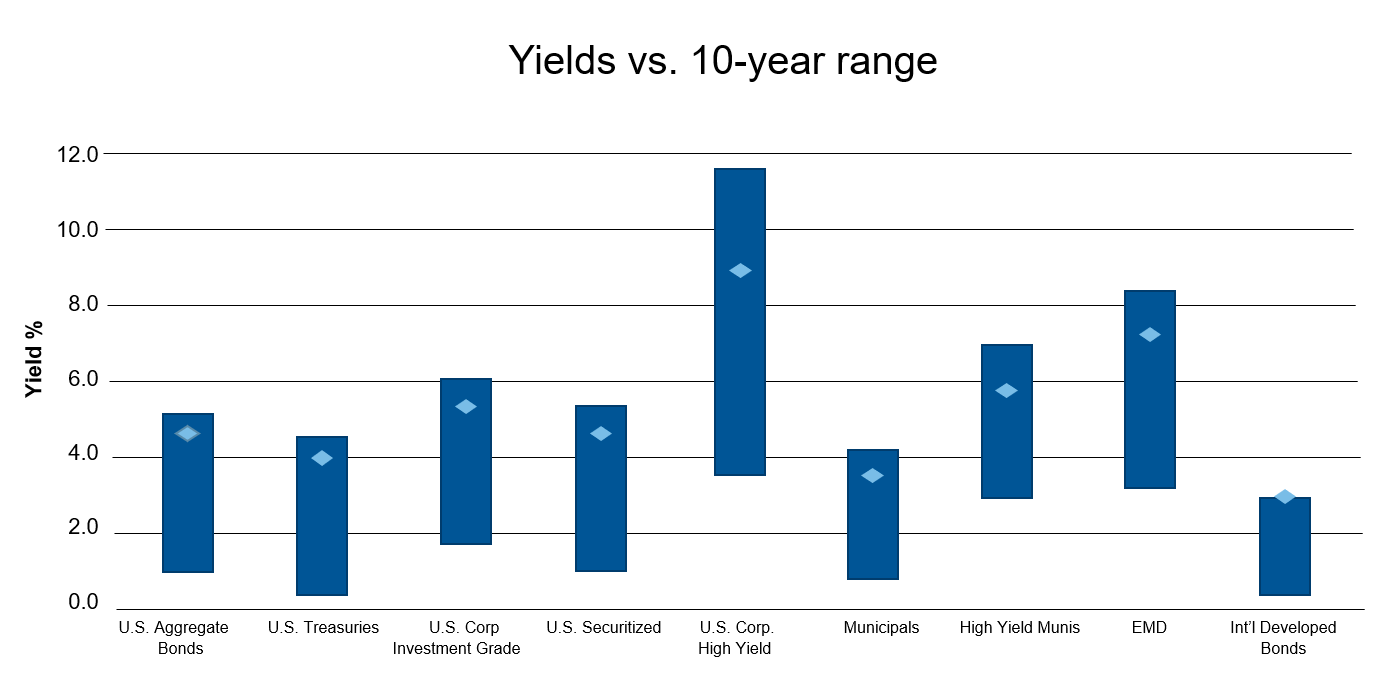

Today's higher rates and better valuations provide a higher core bond income stream than we could have obtained 12 – 18 months ago. Most fixed income asset class yields are at the high end of their 10-year range, offering not just more income opportunity, but also more cushion to offset price volatility. If today's yield levels were the only concern of income investors, then a simple core bond solution could still fit the bill.

Click image to enlarge

Source: Barclay's Live Data. Indices referenced: Bloomberg U.S. Aggregate Index, Bloomberg U.S. Treasury Index, Bloomberg U.S. investment Grade Corporate Index, Bloomberg U.S. Securitized Index, Bloomberg U.S. High Yield Corporate Index, Bloomberg Municipals Index, Bloomberg High Yield Muni Index, Bloomberg Emerging Market Hard Currency Aggregate index, Bloomberg Global Aggregate ex. USD Index. Data is based on 10-year range ending 12/30/2022 and are based on the yield to worst.

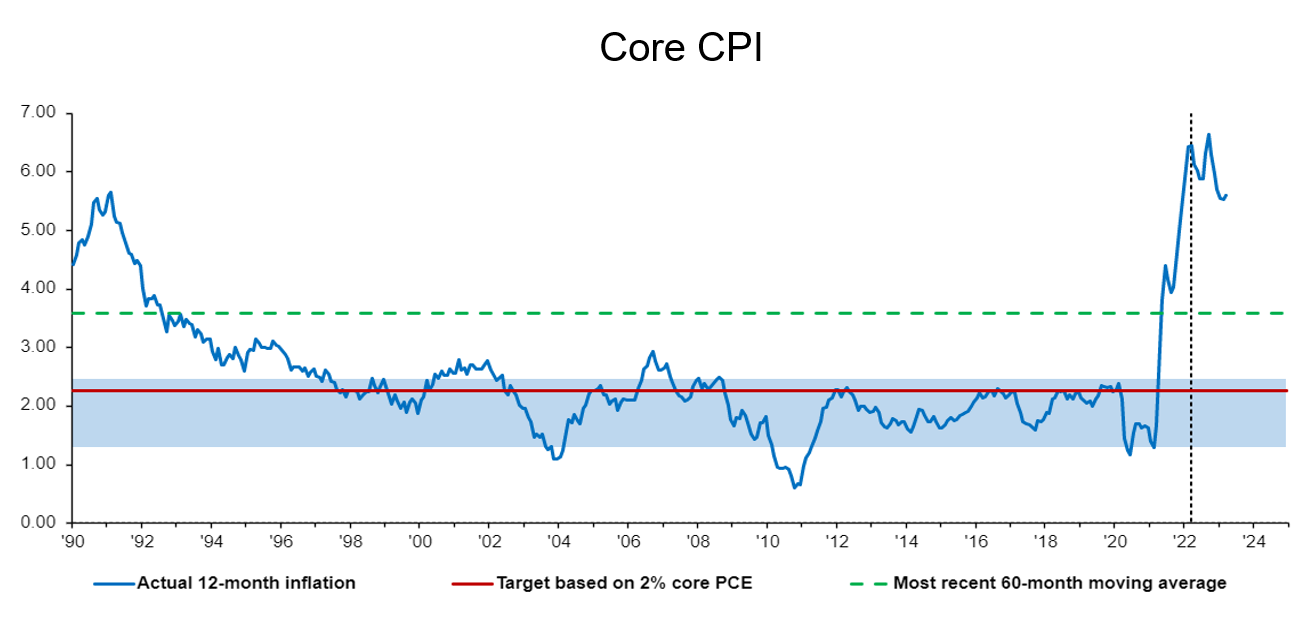

However, higher yield levels do not mean that risk has been removed. Inflation pressures are lurking, and inflation can be the enemy of income-seeking investors. In an ideal world, the cash flow generated by an income portfolio maintains its spending power through the years. Investors seeking to make their investment income endure – for example, during retirement — need to consider their portfolio's ability to grow that cash flow faster than inflation. That's why a diversified income strategy may be a useful option in an inflationary environment.

Click image to enlarge

NOTE: Shaded range indicates 25th to 75th percentile of the 1-month growth rates computed over the past 10 full calendar years.

Source: U.S. Bureau of Statistics, March 31, 2023

How can inflation risks be managed?

Diversifying the sources of income can help manage inflationary risks. An allocation to core bonds (Treasuries, investment-grade corporate bonds) can help provide a foundation to a portfolio now that yields have increased, and adding additional asset classes can help generate incremental yield as well as the opportunity for total return to keep pace with inflation.

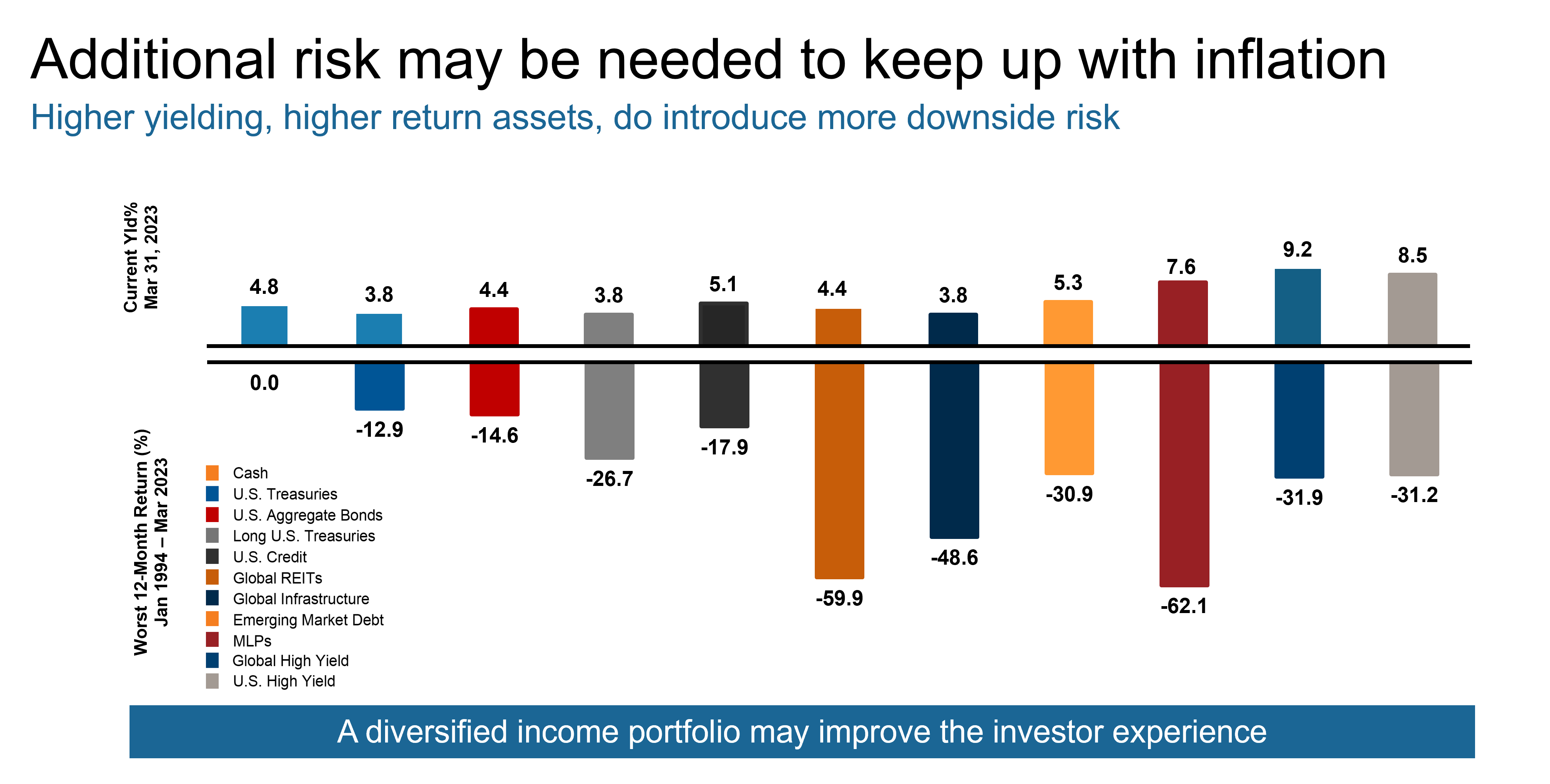

Some examples of asset classes that can provide additional sources of income yield as well as less correlated sources of total return include listed infrastructure, global real estate, emerging market debt, dividend growth stocks, high yield bonds, and preferred securities, among others.

Click image to enlarge

Cash: S&P 0-3 Month T-Bill Index; U.S. Treasuries: Bloomberg U.S. Treasury Index; Credit: Bloomberg U.S. Credit Index; Long Treasuries: Bloomberg Long U.S. Treasuries Index; Global Infrastructure: S&P Global Infrastructure Index; U.S Aggregate Bonds: Bloomberg U.S. Aggregate Bond Index; Global REITs: FTSE EPRA/NAREIT Developed Index; Emerging Market Debt: Bloomberg Emerging Markets Debt Index; U.S High Yield: Bloomberg High Yield Corporate Index; Global High Yield: Bloomberg Global High Yield Index; MLPs: Alerian MLP Index. Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

While those alternative sources of income can round out an income-oriented portfolio, risk remains as some assets tend to be much more volatile than core bonds. Looking at higher-yielding asset classes historically, we can see that while yields have improved, there can be times of significant negative performance. which makes having a professional active manager monitoring and providing risk management is critical to the potential success of an income-oriented portfolio.

The bottom line is that bond yields have improved, and income-seeking investors can once again generate much higher income from less risky assets than what was previously possible. That said, inflation can eat into the ongoing spending power of the cash flow generated from the income portfolio. Adding diversified sources of income to core bonds through additional higher-yielding asset classes may help investors meet their long-term income and spending needs. Adopting a models-based approach that offers professional asset allocation, active security selection, and risk management can help both advisors and their clients reach their spending and financial goals.