Municipal high yield bonds: Why they’re more relevant than ever for your portfolio

The road leading to the recent tax policy change had many investors expecting that large reductions in U.S. personal income tax rates would make tax-exempt municipal bonds virtually obsolete.

The reality proved to be far from the case, as income tax rates were only modestly lowered—while at the same time municipal bond supply took a hit, as the disallowance of advanced refunding municipal bonds is expected to decrease overall supply by 10-15% annually.1 Thus, with retail demand expected to hold while supply is decreasing, it behooves investors to continue searching for their optimal tax efficient portfolio, which would include municipal high yield bonds.

What are municipal high yield bonds? A brief look under the hood

Most think of municipal debt as only high quality and, when you consider the entire muni universe, that’s broadly true, with high yield only 3% of the approximate $3.9 trillion muni market.2 This small market size of $100 billion as of March 1, 2018, means that most high yield municipal bond funds blend in 40-60% investment grade tax-exempt debt, as a high yield-only muni fund would be too illiquid and lack appropriate diversification.

Key sectors in high yield municipal debt are tobacco settlement (where states have securitized future settlement payment from tobacco companies), general obligation (supported by broad tax authority of local authorities), and industrial development bonds (supported by revenue generated from specific economic activities like waste disposal or manufacturing).

Looking for income? Municipals may out-yield corporate bonds on a taxable-equivalent basis

One area that continues to draw investors’ attention is the ability of their investments to generate income, especially in this low yield environment. As we’ve noted in the past, municipal high yield bonds may provide an attractive option for investors. The average yield-to-maturity (YTM) as of August 31, 2018, across Morningstar’s list of covered municipal high yield mutual funds is 4.8%3—the taxable equivalent of which (assuming the new 40.8% highest tax bracket) is 8.1%.4 This compares quite favorably to U.S. high yield corporate bonds, the market of which has a YTM of 6.5%.5 This difference is even starker when you factor in that all of the corporate bonds in this example are sub-investment grade, while the municipal high yields funds tend to include some amount of investment grade positions.

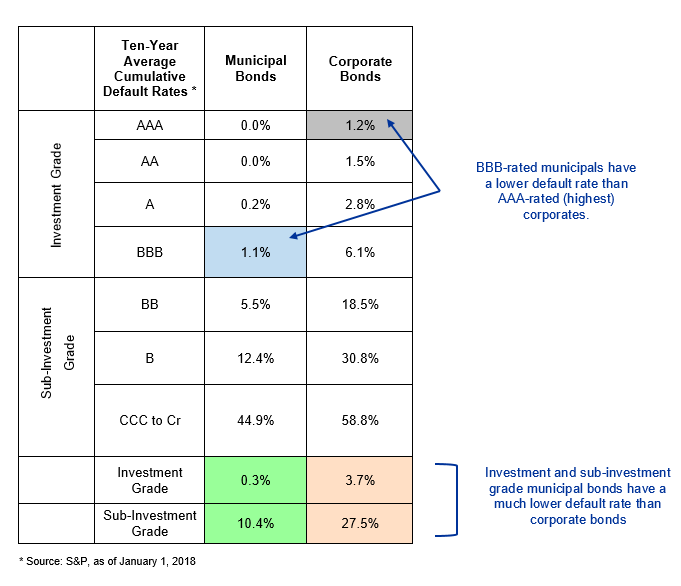

Credit quality: Municipals have the advantage

We believe defaults in corporate bond space are expected and are a matter of course. Corporate issuers may willingly stretch themselves financially, knowing that they can default, restructure and re-enter the capital market to again issue debt. However, this is not generally the case for tax exempt bonds. Municipal issuers are very reliant on the bond market. This (plus attendant political issues) makes them very reluctant to miss payments and risk cutting themselves off from lenders. It is for these reasons that defaults rates for municipals—for a given level of credit quality/rating—are much lower versus corporates.

Bottom line: Municipal high yield bonds shouldn’t be overlooked in your allocation decision

Many investors are searching far and wide for attractive returns in the current low rate environment, often stretching for yield and taking risks that may go uncompensated. Tax-managed investors searching for attractive risk-adjusted returns might consider municipal high yield as part of their overall portfolio solution. The power of tax-exemption has resulted in historically competitive risk-adjusted returns for tax-sensitive investors. Coupled with valuations (relative to corporate bonds) that are appealing in the current market cycle, favorable historical default rates, and tax-equivalent yields that would require taking on much more risk to achieve in the corporate high yield market, we believe municipal high yield is worthy of consideration as a strategic allocation in your portfolio.

1 Source: Goldman Sachs Assets Management

2 Sources: Municipal Securities Rulemaking Board (MSRB); Bloomberg (Bloomberg Indices).

3 Source: Morningstar Direct data through 8/31/2018 (for the average of the municipal high yield universe Morningstar covers).

4 Source: Morningstar Direct data through 8/31/2018 (for the tax equivalent yield of the aforementioned Morningstar universe average).

5 Source: Morningstar Direct data through 8/31/2018 (for the average of the U.S. high yield Corporate universe Morningstar covers).