Despite TCJA, tax-aware investing still matters

The turn of the calendar to a new year serves as a subtle reminder that Tax Day in the U.S. is yet again approaching. While taxpayers will have additional time to file their taxes in 2018 (April 15 falls on a Sunday, so the official Tax Day is April 17), there is something much more unique about this year’s tax season.

That, of course, is the recent passing of the Tax Cuts & Jobs Act by Congress in December of 2017, effectively changing tax rates for both households and businesses across the U.S. These changes will likely continue to garner attention in the media and from investors alike, despite not being in force until next tax year. What is clear, though, is that taxes will continue to have an impact on taxable investment portfolios. One of our key missions at Russell Investments is to help more investors and advisors understand this impact—and manage it intelligently.

The turn of the calendar to a new year serves as a subtle reminder that Tax Day in the U.S. is yet again approaching. While taxpayers will have additional time to file their taxes in 2018 (April 15 falls on a Sunday, so the official Tax Day is April 17), there is something much more unique about this year’s tax season.

That, of course, is the recent passing of the Tax Cuts & Jobs Act by Congress in December of 2017, effectively changing tax rates for both households and businesses across the U.S. These changes will likely continue to garner attention in the media and from investors alike, despite not being in force until next tax year. What is clear, though, is that taxes will continue to have an impact on taxable investment portfolios. One of our key missions at Russell Investments is to help more investors and advisors understand this impact—and manage it intelligently.

Tax impact in 2017

Capital markets posted some of their strongest returns in recent memory in 2017. At the same time, many mutual funds had quite large taxable distributions. As a result, many investors didn’t get to keep as much of their portfolio returns as they had earned. Let’s try to put some numbers to this:- The average capital gain distribution for those U.S. equity mutual funds and ETF’s that had a distribution was 8.4% of the fund’s Net Asset Value. This is up materially from 2016’s average of 5.6%.1

- This distribution was split, on average, between 20% Short-Term Capital Gains and 80% Long-Term Capital Gains—which was also higher than last year. In 2016, the proportion of short-term to long-term capital gains was 11% to 89%, respectively. Remember, short-term capital gains are typically taxed at a higher rate, compared to long-term capital gains.

Looking Ahead

At Russell Investments, we do not have a crystal ball to predict capital gain distributions for 2018. However, applying 2017’s average capital gain distributions and the new 2018 tax rates to the same hypothetical investment scenario as above shows that tax-sensitive investing is likely to remain relevant for many investors: Assumed investment: $500,000 Capital gain distribution: 8.4% Taxable distribution: $42,000 Federal tax due**: $11,424 The lower tax rates only reduce the federal taxes due by $218, or 1.87%. That’s because the long-term capital gains rate didn’t change at all in the TCJA and the short-term rate only came down from 43.4% to 40.8%. True, it’s a reduction. But it’s not large enough to justify disregarding taxes when creating an investment plan.Potential long-term benefits of tax-sensitive investing

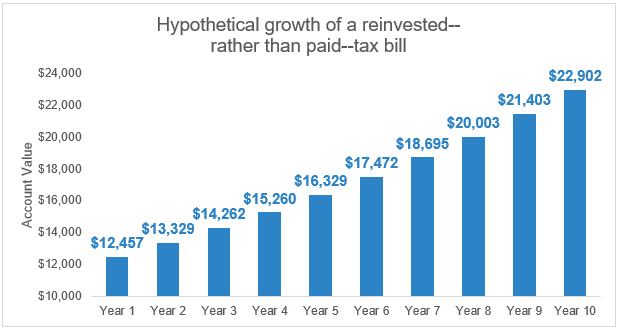

Five-figure tax bills aside, continually facing large taxable distributions, such as the one in 2017, can have a material impact on the long-term wealth of investors. Therefore, we at Russell Investments believe taxes can be managed—through active tax-loss harvesting (not just once a year) to minimize short-term and long-term capital gain distributions, minimizing wash sales, managing holding periods, and focusing on qualified versus non-qualified dividend distributions. These tools can help lower tax liabilities today and allow for additional portfolio growth over the long run. Let’s consider our first scenario once again, where instead of paying a tax bill of $11,642, we invest those proceeds in a portfolio that averages a 7% annual return. Assuming no taxes are paid along the way, that investment would almost double over a 10-year time horizon to $22,902: Imagine what an additional $22,902 could do for your client’s investment goals: Could it could help fund their child’s education? A down-payment on a home? Help them remain comfortable in retirement?

Taxes aren’t simply percentages and unpleasant conversation topics to survive once per year. They can be actively managed to help your clients reach their goals—and you to reach yours.

Imagine what an additional $22,902 could do for your client’s investment goals: Could it could help fund their child’s education? A down-payment on a home? Help them remain comfortable in retirement?

Taxes aren’t simply percentages and unpleasant conversation topics to survive once per year. They can be actively managed to help your clients reach their goals—and you to reach yours.

Bottom Line

Recent changes to tax legislation may cause some investors to place less value on the benefits of tax management going forward. The numbers show that this is a false sense of security. Taxes will likely continue to materially affect after-tax wealth for many nonqualified investors. Thankfully, tools and strategies designed to minimize this impact exist and may help create greater after-tax wealth for investors and advisors alike.1 Source: Morningstar and Russell Investments calculations. Includes all open-ended U.S. equity mutual funds and ETF’s to include active and passive funds, and all share classes, in the Morningstar U.S. Fund Large Blend, U.S. Fund Large Growth, U.S. Fund Large Value, U.S. Fund Mid-Cap Blend, U.S. Fund Mid-Cap Growth, U.S. Fund Mid-Cap Value, U.S. Fund Small Blend, U.S. Fund Small Growth, U.S. Fund Small Value universes.

* Federal tax due calculation assumes 8.4% distribution is taxed as 80% LTCG / 20% STCG. LTCG taxed at 23.8% (20.0% + 3.8%) and STCG taxed at 43.4% (39.6% + 3.8%).

** Federal tax due calculation assumes 8.4% distribution is taxed as 80% LTCG / 20% STCG. LTCG taxed at 23.8% (20.0% + 3.8%) and STCG taxed at 40.8% (37.0% + 3.8%).