Executive summary:

- Liability-driven investing (LDI) strategies can be effective at reducing volatility in funded status measures that are marked-to-market (MTM), such as GAAP and IAS accounting funded status, though results can vary.

- For other measures, particularly those used for calculating U.S. funding requirements, LDI is less effective at managing surplus volatility given the heavily-smoothed nature of the liability discount rates. Asset smoothing methods used in contribution requirement calculations can further misalign assets and liabilities.

- Pension plan sponsors with large allocations to LDI, and particularly those that are well-funded, can choose to adopt a full yield curve (FYC) approach for measuring funding liabilities. Doing so aligns the various liability measures used by their plan actuaries for accounting, funding and PBGC purposes, which leads to better-stabilized and predictable pension measurements in its various forms.

Background

U.S. corporate pension plan sponsors are required to measure their plan liabilities for a few important purposes. The most important of these are summarized in the following table:

EXHIBIT 1: COMPARISON OF LIABILITY MEASURES

LIABILITY MEASURE | PRIMARY PURPOSE(S) | DISCOUNT RATE METHODOLOGY & OPTIONS1 | OTHER CONSIDERATIONS |

| Projected Benefit Obligation (PBO) | Accounting | Current market "spot" rates | Some sponsors use selective bond markets, which can artificially increase the discount rate |

| Funding Target (FT) | Contribution requirements, benefit restrictions | 1) 24-month average, subject to corridor around the 25-year average2 2) Full Yield Curve (spot3) | Election change requires IRS approval |

| Premium Funding Target | PBGC Variable Rate Premiums | 1) Standard method (spot) 2) Alternative method (linked to Funding Target) | Election can be changed after 5 years |

Of the liability measures in Exhibit 1, the LDI strategy is most effective at addressing the PBO and PBGC "Standard method" measures since they are based on spot rates with a fairly predictable sensitivity to interest rate movements. LDI portfolios can be designed to closely match these liabilities' expected behavior, thus reducing funded status volatility. For plans that are in a "hibernation" state4 – fully funded, usually frozen, and with high allocations to LDI – this strategy has proven to be quite effective.5

The Funding Target used for contribution requirements has been much lower than the PBO for most of the time since 2012. This was when pension law changed with MAP-214, introducing a new type of funding relief. MAP-21,6 changed discount rates to be tied to a range around the 25-year average. Due to this, the Funding Target now shows very little sensitivity to ongoing interest rate changes. Until the end of 2022, the Funding Target's associated funded status, the FTAP,7 has been much higher than the PBO funded status since the 25-year average of rates was also much higher than the spot rates from 2012 to 2022. This provided plan sponsors with significant funding relief, given contribution requirements are directly tied to the FTAP (lower FTAP leads to higher contribution requirements).

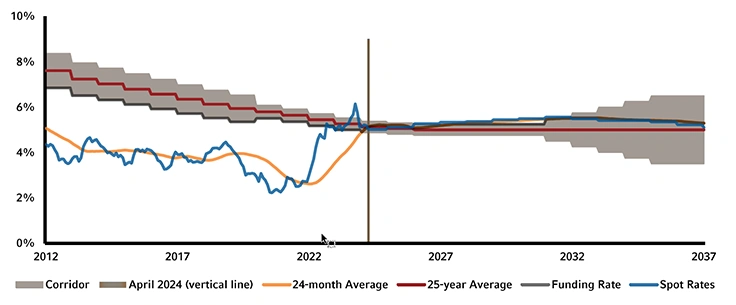

Exhibit 2 shows the historical and projected path of various discount rate measures, including the spot rates (blue line), similar to what is used for accounting, and the funding rate as shown in the black line. Observe the large gap between the black and blue lines that led to the significant difference between FTAP and PBO-funded status between 2012 and 2022.

EXHIBIT 2: COMPARISON OF FUNDING DISCOUNT RATES

(Click image to enlarge

Source: IRS and Russell Investments calculations. Only segment 2 shown. Future rates assumed to be the 50th percentile of Russell Investments Strategic Planning capital markets forecasts as of December 31, 2023.

For PBGC premium purposes, plan sponsors have two options for setting discount rates – the Standard method (spot rates) and the Alternative method (24-month average6). Sponsors can elect to change this method after five years. At some point, most sponsors have elected to change from the Standard to the Alternative method or vice versa to reduce PBGC premiums. In the Exhibit 2, the orange line shows what the Alternative method discount rate would have been, while the Standard method would have been the blue line.

Given the significant increase in rates in 2022, all these measures are now similar (see current rates at the vertical line), and if spot rates were to rise above the corridor, the FTAP would actually be lower than the PBO funded status and could lead to contribution requirements even when on a marked-to-market (MTM) basis, the plan is fully funded.

Electing the full yield curve

Sponsors can elect to use the "Full Yield Curve" (FYC) for contribution requirement purposes, which more closely follows the spot rates similar to what is used for accounting purposes. The election is effectively permanent,9 so sponsors should consider this a long-term strategic choice rather than a one-time tactical decision to reduce contributions or PBGC premiums in the near term only.

Making this election has historically been uncommon. Based on the most recent public information available, less than 1% of plan sponsors elected the FYC10. This will almost certainly increase now that rates have risen, and the case is more compelling. But it will still take some time for the trend to pick up.

Why would a plan sponsor choose to go to MTM for funding purposes? Because in combination with a high allocation to LDI and a well-funded position, electing the FYC is quite effective at stabilizing both FTAP-funded status and contributions. This means better predictability and lower chances of cash required.

To illustrate, see Exhibit 3 below, which shows the range of FTAP funded status under current discount rate assumptions (in blue) and under an FYC election (in orange). This assumes the plan is 100% funded, frozen and with 90% in LDI. While some uncertainty still remains due to equity risk and asset/liability mismatches, the range of outcomes narrows significantly when the FYC is elected. This is due to funding liabilities no longer being bound by a range of discount rates disconnected from current markets, allowing assets and liabilities to move more closely in tandem.

Exhibit 3: FTAP Funded status % | Portfolio: 10/90

Comparison of FTAP Projections with (orange) and without (blue) FYC election for 100% funded frozen plan with 90% in LDI.

(Click image to enlarge)

Another important takeaway from Exhibit 3 is the likelihood that the FTAP falls below 100% using the current discount method and by how much. Since contributions are generally required whenever the FTAP falls below 100%, the FYC election should lead to lower contribution requirements, shown in Exhibit 4 below (again, blue is the current method, while orange is the FYC). In fact, contribution requirements would be expected to be more stable, lower, and less at-risk for extremes.

Exhibit 4: CONTRIBUTIONS | PORTFOLIO 10/90

Comparison of Minimum Required Contribution projection with (orange) and without (blue) the FYC election, assuming the plan is 100% funded, frozen with 90% in LDI.

(Click image to enlarge)

Assessing tradeoffs

The effectiveness of electing the FYC will depend on a few important factors. We will focus on the impact of MTM-funded status and the overall allocation of LDI. We will assume for this purpose that the plan is frozen and does not currently hold any credit balances. We also assume plan expenses are paid from plan assets. These and other assumptions and factors will influence the impact of an FYC election, and we recommend long-term stochastic asset/liability modeling to assess the full effect of an FYC election.

Let's start with a 100% funded, frozen plan. At this stage, sponsors generally are trying to reduce the absolute amount of contributions they would need to pay, but also they would like to mitigate worst-case contribution outcomes. Exhibit 4 shows a range of portfolios, from 60% global equity and 40% LDI (60/40) to 10% global equity and 90% LDI (10/90). The orange series assumes that the standard discount rate method (tied to the 25-year average) is used, while the blue line is the same but with the FYC method.

In this exhibit, portfolios toward the left are less risky (i.e., better worst-case outcomes), while portfolios toward the top have lower average contributions. With this framework, we can compare portfolios to see which are less risky and require fewer contributions. Portfolios trending to the upper left are preferred.

EXHIBIT 5: 100% FUNDED, FROZEN PLAN, COMPARISON OF PRESENT VALUE OF FUTURE CUMULATIVE CONTRIBUTIONS

(Click image to enlarge)

The main takeaway from Exhibit 5 is that the FYC election for a 100% funded, frozen plan starts to make sense when the portfolio holds 70% or more in LDI. With less than 70% in LDI, the equity risk tends to dominate the risk and return potential.

Now, what if the plan were better funded, assuming 110% on an MTM basis? At that point, the risk of falling below 100% funded (and having contribution requirements) is relatively low if the funded status can be effectively stabilized. Exhibit 6 shows this.

Exhibit 6: 110% FUNDED, FROZEN PLAN, COMPARISON OF PRESENT VALUE OF FUTURE CUMULATIVE CONTRIBUTIONS

(Click image to enlarge)

In this scenario, the benefit of the FYC election is clear. Given the overfunded position, a 10/90 portfolio that effectively stabilizes funded status11 with the FYC election is far and away the most efficient portfolio. This case would be even more compelling as the funded status further improves.

Let's take a step back and consider the effectiveness if the plan is less well-funded at 90%. Here, contribution requirements would be required regardless, and the FYC election helps stabilize funded status but does not necessarily improve funded status over time. It does, however, help avoid extreme funded status declines attributed to asset/liability mismatches.

Exhibit 7: 90% FUNDED, FROZEN PLAN, COMPARISON OF PRESENT VALUE OF FUTURE CUMULATIVE CONTRIBUTIONS

(Click image to enlarge)

In Exhibit 7 we see less benefit to the FYC election, as it would likely be advisable to retain more than 30% in return-seeking assets at this funded level (unless the sponsor was committing to fund the deficit). We would generally not recommend electing the FYC unless the sponsor strongly desires liability alignment and commitment to contribute.

Other considerations

While the case for electing the FYC may seem compelling, where could it go wrong? Sponsors should consider the following before making this election.

- Timing. The election cannot be reversed without authorization from the IRS. A long-term perspective is important. Some sponsors may prefer to "wait and see" if rates rise to a level where the discount rate mismatch is problematic and consider this election again at that point.

- Asset method. We recommend that during this election, the sponsor also remove asset smoothing from the Actuarial Value of Assets calculation to better align assets with liabilities12. The minimum required contribution itself will still allow for 15-year amortizations of funding deficits.

- Asset/liability mismatches. These will remain present and could be the primary driver of funded status changes. These include liability gains and losses during actuarial valuations, which can come from demographic experience, changes in assumptions, or changes in methods.

- Credit migration. Within the LDI, credit downgrades/defaults not made up for with active credit management or other excess returns could lead to deterioration of funded status. In addition, equity risk taken to help generate returns to offset asset/liability mismatches or plan expenses can also have adverse effects on funded status.

- Law changes. Pension law could change and alter the 25-year average corridor to simply being a floor, which would impact this analysis. We have yet to see this law change proposed, but it is possible.

Conclusions

For sponsors with well-funded, frozen plans and high allocations to LDI, we see a strong case for electing the Full Yield Curve to calculate funding liabilities. Doing so would synchronize all the liability measures, stabilizing expected contributions and reducing funded status volatility.

1 All discount rates are based, to some extent, on high quality U.S. corporate bond yield curves.

2 25-year average floored at 5.0%.

3 The Funding Target version of the spot rate is actually averaged over the month but remains highly correlated to the PBO version, which is typically set on the last day of the month.

4 Owens, J. (2023). A guide to pension plan hibernation. Russell Investments Viewpoint. Available at: https://russellinvestments.com/-/media/files/us/insights/institutions/defined-benefit/a-guide-to-pension-plan-hibernation.pdf

5 Owens, J. (2021). DB plan hibernation: Does it really work? Russell Investments Blog. Available at https://russellinvestments.com/us/blog/db-plan-hiberation.

6 Moving Ahead for Progress in the 21st Century Act.

7 Funding Target Attainment Percentage.

8 Technically, this method aligns with the Funding Target, except for the 25-year smoothing constraint. See Barry M. (2024). Three issues corporate plan sponsors should be aware of in 2024. Russell Investments Blog. Available at: https://russellinvestments.com/us/blog/plan-sponsors-2024-issues.

9 The IRS would have to approve any change, or Congress would need to update the law.

10 Based on 2022 5500 filings. The most recent data is as of the beginning of 2022 and prior to the large rate rise seen that year.

11 See end note 5.

12 Note that this election is also effectively permanent, requiring the approval of the IRS to change.