DB plan discount rates are setting new historical lows

Due to declining treasury rates and tighter spreads, defined benefit (DB) plan sponsors are facing the lowest discount rates in the modern era. This has led to increased liability valuations, and thus lower funded status for many plans. This hurts the balance sheet and a variety of other measures that can influence the extent and timing of contributions, the level of Pension Benefit Guaranty Corporation (PBGC) premiums and whether risk transfer can be pursued. But to what extent will the recent fall in discount rates really impact sponsors? That depends on which measure you are focused on.

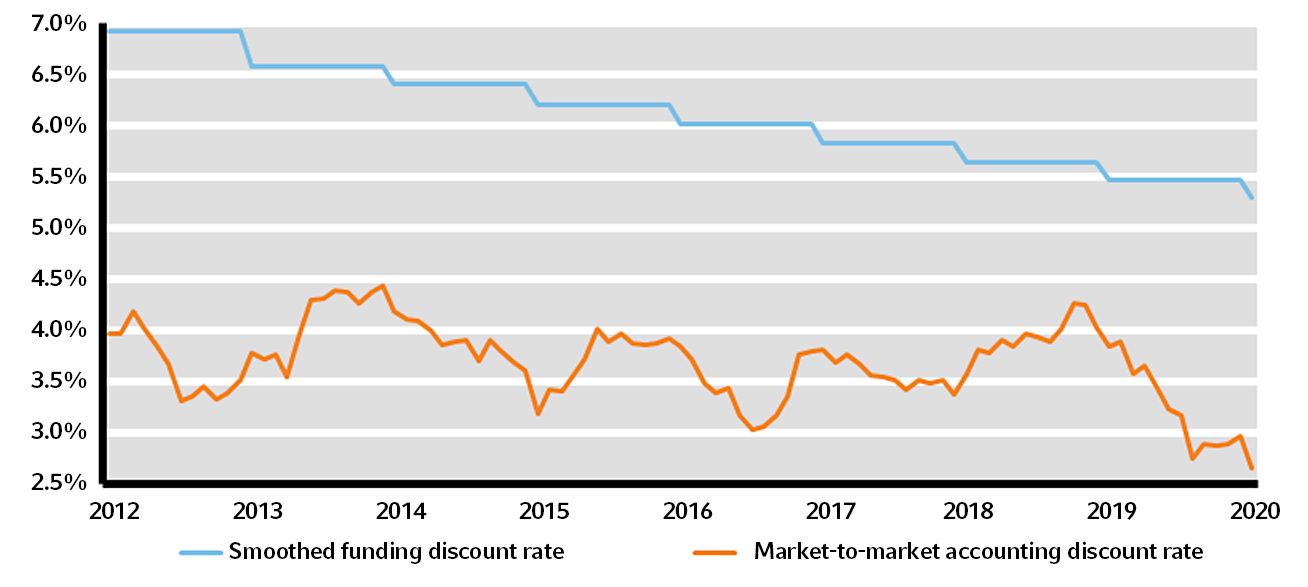

Sponsors are primarily concerned with corporate bond discount rates, as they are used in both funding and accounting calculations. However, since the introduction of pension funding stabilization¹ in 2012 , smoothing of discount rates over extended periods of time has become the norm for certain key funding measures. While providing sponsors with funding flexibility (albeit with corresponding PBGC penalties), funding stabilization has distinctly bifurcated corporate DB discount rates into two categories:

- Smoothed/funding discount rates

- These rates are used to determine contribution requirements and benefit restrictions.

- At present, they are based on a 90% corridor below the 25-year average of IRS discount rates.

- Currently, these rates are about 5.5% and decreasing each year in a predictable manner, as the 25-year average declines and future corridor expands.

- Marked-to-market/accounting discount rates

- These rates are used for balance sheet, pension expense and PBGC premium purposes.

- As there is no smoothing of these rate, they are subject to significant volatility over time.

- They are currently lower than 3% for many DB plans.

The following chart illustrates the pattern of these two discount rates over the last eight years, since funding stabilization was enacted.²

Funding and Accounting Discount Rates

Source: IRS, FTSE Pension Discount Curve

This chart makes clear the stark difference in predictability of the smoothed versus marked-to-market rates since 2012, but it also illustrates the large and persistent gap between the two measures. The average difference over this time horizon is about 240 bps and has ranged from 140 bps to 360 bps. While the smoothed rates have declined in a predictable fashion, marked-to-market rates have also declined—particularly over the last year.

Despite these lower rates, many sponsors may still claim to be fully funded, referring to their FTAP or AFTAP³ status, calculated by their actuary with smoothed discount rates. They often have no-or-negligible contribution requirements, and any PBGC premium may not receive attention, as it can be paid out of plan assets. But what would the equivalent funded status be using current marked-to-market rates? The difference can be significant.

Assuming for the moment that funding and accounting calculations use the same liability assumptions—except for the discount rate—let’s see how much lower a plan's funded status can be, moving from one measure to another, for various liability durations.

| Estimated underlying marked-to-market funded status | |||

| Funded status using smoothed rates | 8-year liability duration | 12-year liability duration | 16-year liability duration |

| 110% | 91% | 84% | 78% |

| 100% | 83% | 76% | 71% |

| 90% | 75% | 69% | 64% |

Source: Russell Investments, based on marked-to-market rates as of January 31, 2020

As you can see, the duration of the liabilities has a significant impact on the difference between the two measures. Note that if the accounting liabilities were to include future pay increases, the impact would be even more significant. It can be disheartening for a plan sponsor who is perceived to be 100% funded on one measure to really be as low as 70%. This has implications for PBGC premiums, additional filings and the effects of benefit payment drag.

Barring future changes to pension law, sponsors ought to be mindful of the coming phase-out of funding relief. With the ongoing decline in the 25-year average determined by the IRS, and the 90%/110% corridor expanding from 2021, the effects of funding relief will increasingly wear away. Contribution requirements will increase for many plans, bringing marked-to-market liabilities into economic reality.

As always, we stand prepared to help clients assess the associated implications for investment strategy and contribution policy into the future.