When it comes to ESG and performance, can you have your cake and eat it too?

Let’s cut to the conclusion: Does an ESG-related mandate require a performance hit? No.

It is the job of investment managers to understand all of the relevant data points for every security they buy and sell. In 2019 and beyond, including environmental, social and governance (ESG) data points in the investment process has become table-stakes. Even if a manager is not oriented toward ESG mandates, ESG data still has implications on the short- and long-term returns of an investable security. ESG data is significant when it comes to determining how a company impacts the planet. But ESG data is also significant when it comes to deciding if a stock will be performance-enhancing and risk-mitigating. In other words, to ensure the most complete analysis of return opportunities and potential risks, ESG should be understood by investment managers—we believe it is value-adding to a skillful investment process.

In most cases, there are two reasons investors care about ESG issues. An often-cited reason is values-based: The investor wants to include or exclude securities because of a specific values-based world view. The other reason is value based. Investors, seeking to generate excess returns, are looking at ESG issues for performance and risk-mitigation issues. A growth investor may see green energy as a growth opportunity or a restructured governance process as a way to realize a price correction.

These two factors—values and investment value—are different. But we believe both can be addressed at the same time and may, in fact, be complementary. Is this two-pronged approach harder than investing for just one goal or the other? Possibly.

Examining the universe of ESG managers

At Russell Investments, we’ve been researching investment managers for five decades. We currently monitor more than 13,000 manager products—an undeniably large universe. And out of all those managers, our research tends to find that approximately half have above-market ESG metrics and half do not. In particular, manager products with both above and below-market ESG metrics still have earned a hire ranking—no easy task. In other words, approximately half of our recommended managers are expected to deliver value AND exhibit holdings with above average metrics.

SO THEN, can we deliver an ESG mandate while delivering strong performance? We believe the answer is yes.

The energy sector as a proof point

A typical mandate we see from our investor clients is a desire to shrink the carbon footprint of their portfolio. But most of our clients also come to us because of our ability to build portfolios that are well-diversified and risk-managed. In most cases, exposure to the energy sector is still a key aspect to achieving those last two goals.

Depending on their assignment, our underlying equity managers have, as expected, positive and negative exposures to every sector. As part of their goals of portfolio performance and risk mitigation, we do not expect any extraordinary deviation in their active portfolios to energy relative to other sectors. But what happens when a low carbon mandate is applied to a portfolio? Will managers then be underweight energy, compared to other sectors? Not necessarily.

Why? Because energy is a large and complex market sector. And there are many available securities within that sector that can provide the desired sector exposure, while still aligning with an investor client’s low-carbon goals. It’s important that investors realize that not all energy companies are the same. For example, Norway’s Equinor, with Q3 2018 market cap of $78 billion, is expecting to invest 15-20% of capital expenditures (CAPEX) in new energy solutions by 2030, according to Luke Fletcher, senior analyst with CDP. In comparison, CDP reports the current industry average investment as only 1.3% of CAPEX.

How much of an exclusion is too much?

We believe there are available securities, even within the energy sector, that can help reach a goal of lower carbon exposure. And we believe there are managers in virtually every manager universe capable of delivering performance and achieving ESG metrics. But after managers choose their securities, we still need to put those managers together into a unified portfolio. We believe this combined portfolio requires nuanced control at the total portfolio level. A total-portfolio approach ensures an appropriate overall exposure to a sector like energy and considers the impact of negative screening at the portfolio level—not just at the manager level.

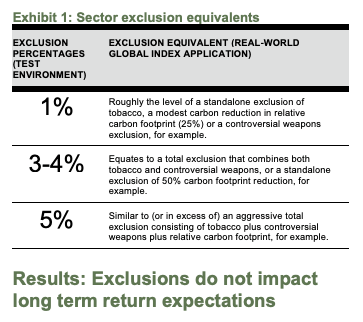

We have also done significant research on both the short-term and long-term impact of negatively screening out ESG hot-button exposures, such as tobacco, munitions, and others. Our research has shown that if investors are asking for just a small exclusion, like tobacco or cluster munitions—just one or two percent—then that still leaves skilled managers plenty of room to potentially build excess return. We would expect very little impact on excess returns, even in the short term.

But what if the investor also wants to screen out coal and divest from fossil fuels? What if the sum of total exclusions is as high as 5% or more? At this point, our research has shown some material deviations that are likely to be noticeable in the short term. At this point, short-term return expectations and tracking error become unreliable and unpredictable. For some investors, this unpredictability will be unacceptable.

However, our long-term return expectations—10-15 years or more—are still the same. This is a key strategic belief that is core to our investment approach, and we believe it is simply basic economics. Every investable company has the same basic challenges of supply and demand, cost structures, ROI, etc. Therefore, skilled managers should be able to find investment opportunities even when a small portion of the universe is unavailable. This results in our strategic belief that we do not believe any single sector outperforms over the long term.

Source: Russell Investments research

A sustainable approach to sustainable investing

It is vital to remember that not all investors have the patience—or even should have the patience—to take such a long-term approach. It depends greatly on their desired outcome and their appetite for peer-relative risk. How much deviation from peers are asset owners willing to sustain to reach their ESG goals? It is up to the investor and their partners to determine a sustainable level of predictability, even when it comes to responsible, sustainable investing. If an investor desires to exclude 7% of their portfolio, for the good of the planet, but then finds they can’t sustain the unpredictability that comes with such a large exclusion, then the ESG goals may be abandoned and no one wins.

Winning matters, both for ESG goals and performance goals. We believe both goals can be reached.