B is for behavioural mistakes: How much value comes from prevention?

There are now so many stock-trading apps that you can find lists ranking the top ten. Investors now have the ability to buy and sell securities on the phone they keep in their pockets and purses. They can make big moves while they’re at the beach or on the train. Some folks champion that access. Not us.

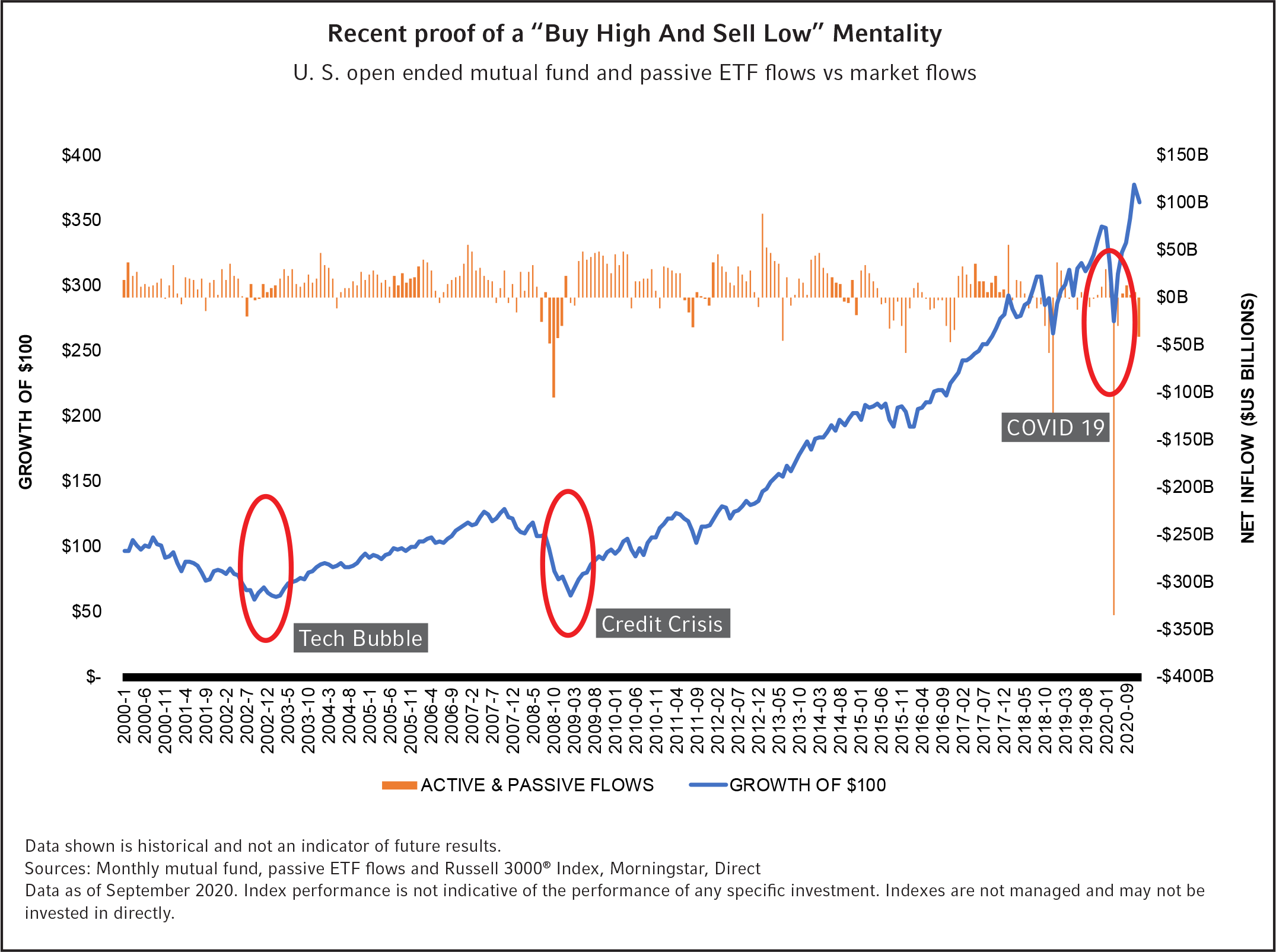

Imagine that your investors chose to pull out of the market on March 23 this year—when the S&P 500 closed at 2,237.40. They would have missed a three-day bounce up to 2,630.07— 17.6%. Think about that: just three days.

What prevented many investors from making a mistake that big? Their advisers.

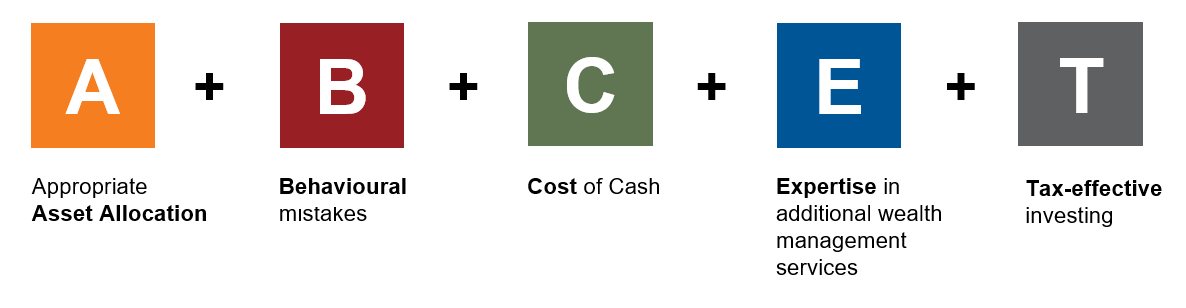

You’ve heard us say it before, but we’re saying it again: Russell Investments believes in the value of advisers. And we believe communicating that value to your clients is more important than ever. That’s why we propose this simple formula:

Value of an Adviser = A+B+C+E+T

Value

Let’s look at the behavioural mistakes that investors typically make and the value advisers provide in helping investors avoid those mistakes.

Check out the chart below. You’ve likely heard many comparisons between the current markets and the Global Financial Crisis in 2008-09, so keep this fact in mind: From January 2000 to September 2020, $100 constantly invested in the Russell 3000® Index more than tripled in value. And those who chose to stay in cash during that period missed a cumulative return of nearly 250%, based on the Russell 3000® Index. Left to their own devices, many investors buy high and sell low. Helping your clients avoid pulling out of markets at the wrong time and sticking to their long-term plan is one way that advisers provide substantial value.

Click image to enlarge

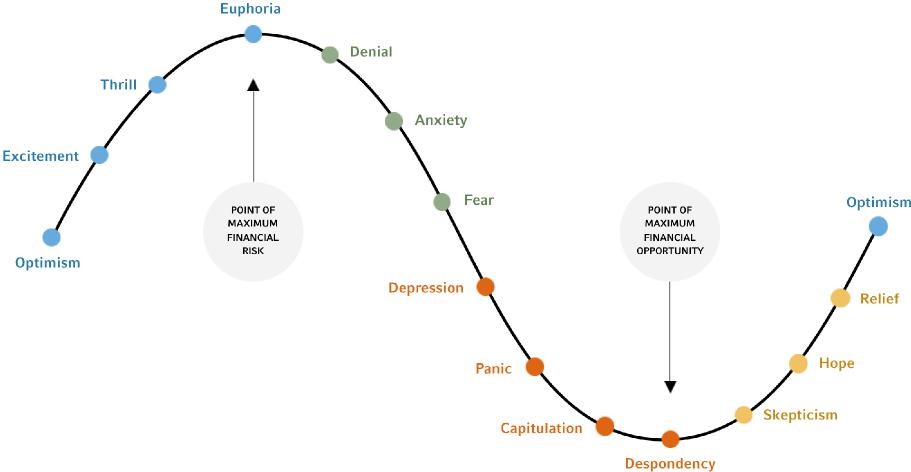

The cycle of market emotions

We all know that this year has been a wild ride so far, and we’ve heard from advisers that they’ve recently delivered more value in this area than they have for some time.

Investors, like all humans, look for patterns, even when they shouldn’t. And sometimes, looking for patterns can get investors into trouble, especially when their pattern-chasing inclinations cause them to make the wrong decisions at the wrong times. They also tend to follow the herd. Left to their own devices, the investor herd, overall, is inclined to do precisely the wrong thing at exactly the wrong time. The herd tends to leave the market when it is down—meaning investors tend to sell low. And the herd tends to enter the market when it is up—meaning investors tend to buy high.

Obviously, this investor behaviour can hurt investor returns. Practically speaking, if an investor’s personal situation really hasn’t changed, then staying the course and riding through these periods of volatility is the logical course. But that is humanly hard. So what can a good adviser do, since we can’t control the markets? We can control—or at least help control—this very behaviour. So that, instead of opening a sharing trading account and pulling out of the market at precisely the wrong time, an investor will have a conversation with his or her adviser. And that conversation—just that simple conversation—could save them from making a costly mistake.

What do some of those adviser-client conversations about the emotions of investing look like? They are interactive, they are transparent. And yes, they’re often emotional. As an adviser, you can’t stop the wave, but you can teach your investors how to surf.

To help support those surfing lessons/conversations, especially in today’s virtual meeting setting, we recently launched a new piece of digital content on our website: The cycle of investor emotions. If you haven’t seen it yet—be sure to check it out!

With this interactive chart, advisers can illustrate for their clients that the very point where investors feel the most despondent—where they may have the highest desire to leave the market, may also be the point of maximum financial opportunity. It’s the adviser’s role to coach them through this cycle—and what a cycle it’s been in 2020. We believe having an accountability partner, like a skilled financial adviser, gives the investor a significantly better chance at making good decisions during periods of both emotional and market volatility.

Behavioural economics: Where finance and psychology meet

Behavioural economics is the academic body of work that recognises the difference between what human investors should do and what they actually do. This is where traditional finance and economics meet psychology.

Within the science of behavioural economics, there are over 200 identified biases that impact their money decisions1 Here are the five we consider to be the most common—and the most important for advisers to address.

- Loss aversion – Humans tend to prefer avoiding losses more than acquiring equivalent gains. In other words, the pain of loss is a more powerful force than the gratification of gain. This fear of loss may cause your investor clients to want to sell winning securities too early. And the fear of missing out may cause investors to hold onto losing securities too long.

- Over-confidence – Investors tend to over-estimate or exaggerate their ability and expertise. In other words, they tend to believe they are experts when they are not. Their belief in their ability to time the market, for example, may cause them to trade too often or at the precisely wrong time. Or their belief in their ability to identify opportunities may cause them to risk too much exposure on a perceived hot stock.

- Herding – Humans tend to mimic the actions of the larger group. When the herd tends to sell and pull out of the market, individual investors tend to join in, even if it means selling low. When humans tend to buy, individuals tend to jump on the bandwagon, even if it means buying high.

- Familiarity – Humans tend to prefer what is familiar or well-known. We see this in the way investors tend to overweight their portfolios toward their home countries, even when there might be a recommendation to diversify globally.

- Mental accounting – Investors tend to attach different values to money based on its source or location, or based on a gut feeling. This from-the-gut approach to investing may put investors at serious risk, and can cause them to avoid proven, sophisticated tools such as Monte Carlo simulations, multi-asset investing, or even basic diversification.

The bottom line

In the formula of adviser value, B is for the behavioural mistakes investors typically make. This value strikes a significant chord this year, when market volatility has been so stark. The good news is that you, the adviser, can have a huge impact on correcting investor behaviour. Doing so can have an equally huge impact on your clients’ investment outcomes. In fact, addressing the investment behaviour of your clients may be the greatest value you provide.To learn more about the 2020 Value of an Adviser Report, click here.

1 Source: Investments & Wealth Monitor, May/June 2017, p