Intergenerational wealth: What and why

What is intergenerational wealth transfer?

A huge sum of wealth is transferred to beneficiaries every single year – whether in the form of inheritance after death, or via gift transfers. However, over the last few years, headlines about the inheritance wealth economy and the big generational wealth shift have appeared just about everywhere. This is the result of research released by a number of firms about exactly how much money is expected to be passed on over the upcoming three decades.1 And, it’s a lot more than we’ve seen before.

All reports have reached the same conclusion: we are on the brink of a vast shift in assets. By 2027, it is expected that wealth transfers will nearly double from the current level of £69 billion, to £115 billion every year.2 Coined as ‘the Great Wealth Transfer’ of the 21st century (GWT), it is expected to bring about a total overhaul to the way current financial advice practices work. Is your practice ready?

The two key drivers behind the Great Wealth Transfer

According to the King’s Court Trust, £5.5 trillion will move hands in the United Kingdom between 2017 and 2055, with this move set to peak in 2035.3 Why? Well, there are a number of contributory factors that account for this, the two key ones being:

1. Increased net worth: property, equity markets and defined benefit transfers

The total net wealth of private households in Great Britain was £14.6 trillion in April 2016 to March 2018, an increase of 13% in real terms from April 2014 to March 2016, mainly due to increases in private pension and net property wealth.

So, who benefitted from the increase in property prices and rising stock markets? Baby boomers (those now aged between 53 and 72), who were able to get on the property ladder in the 1980s and stay on it. Indeed, the Office for National Statistics claim that it is the greatest contributor to the change in UK net worth that we have ever seen.4 Thanks to this capital growth, property is expected to account for more than 70% of the wealth transferred over the coming years.

Furthermore, thanks to low interest rates and quantitative easing, fixed-term final salary pensions have soared in value, adding to the net worth of UK private households. Meanwhile, pension freedoms around Defined Benefit transfers have led to more and more people checking out of their final salary scheme and cashing in. And, as transfer rates have improved, the number of British citizens making the most of 2015’s pensions freedoms have increased. In total, according to the HM Revenue and Customs, £16 billion has been withdrawn. However, the Office for Budget Responsibility recently revised lower their previous drawdown estimation figures, showing that the rate of transfers is indeed slowing.5

2. Increased life expectancy

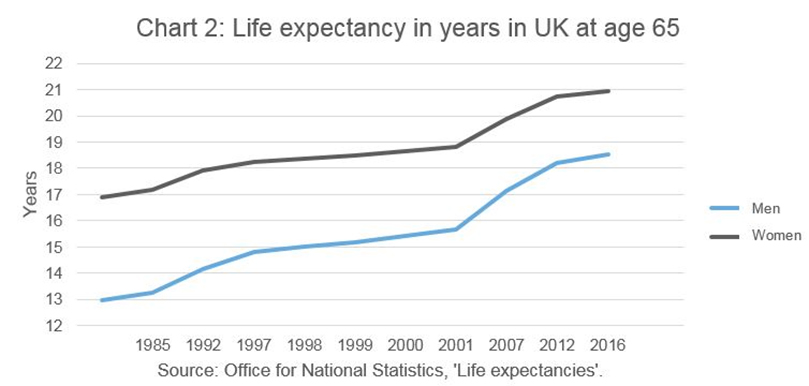

Like their net worth, the life expectancy of baby boomers has also increased. Thanks to a greater awareness of healthy living practices, medical advancements and improved assisted-living facilities, we are all living longer. Life expectancy in the UK at age 65 has significantly risen since 1984 – from 13.0 to 18.0 years for males and from 16.9 to 20.7 years for females (see below chart).

Living longer means that our senior community are holding onto their assets for longer - and reaping the rewards.

Intergenerational wealth: What are the opportunities for advisers?

Assets under management and firm-value have potential to grow

The race is on. A whopping £1 trillion will move hands between now and 2027.6 Spouses, children, grandchildren (and nominated persons) are going to receive large bulk sums, all in one go. With this change in asset ownership comes great opportunity for advisers: a new set of clients, a new set of objectives.

According to the World Health Report by Capgemini, the impact of COVID-19 wiped out more than $18 trillion from markets globally over the course of February and March 2020, before recovering slightly in April. Based on analysis of various market and economic parameters, a quick estimate shows a decline of 6–8% in global wealth till the end of April 2020 (vs the end of 2019). Despite this, individuals are just entering the high net worth individual (HNWI) segment through wealth creation or inheritance. Our survey revealed that 64% of HNWIs under 40 are considering or plan to consider investment returns as their primary source of income within the next five years.

How do people plan to pass on their wealth?

More than 60% of people plan to pass their entire wealth upon death. Though this may seem understandable (due to many holding onto their assets to sustain their lifestyle, or due to the taboo subjects that are money and death), limiting one’s wealth to full transition on death may actually not be the most sensible thing to do. In fact, the inheritance tax burden alone should warrant some pre-death distribution.

Intergenerational wealth: Risks for advisers

As with any great change to the status quo, there are risks and considerations to be managed, along with regulatory requirements. Over the next few decades, adviser client banks will change significantly and so will client risk profiles. In addition, as clients age and approach the end of life, the number of so-called 'vulnerable clients' will increase, bringing with them a whole host of new needs and challenges. Critically, many benefactors haven’t fully thought about, or made thorough plans, for even the most basic transference of wealth. Only 26% of people have a full strategy in place to transfer their wealth to the next generation, while 1 in 3 indicate they have done nothing at all to prepare for passing on wealth to the next generation.7

Action for advisers: 360° engagement

By the same token, advisers need to consider how aligned their existing clients’ investment propositions are with their future clients. Take a 360° approach. Engaging with inheritors today will give them (and you) a much-needed head start – may that be ‘the Sandwich Generation’ (those who support both their children and their parents) or the younger generations (those between 18-35). Future clients will have different objectives, such as university funds or house deposits. The best way to get ahead is to encourage benefactors to engage with the family as a whole, and plan for how these objectives can be satisfied now, rather than on death.

Asset and client retention

Current client retention rates following asset-transition after death are disappointing and indicate that soon-to-be inheritors are unlikely to stick with the same adviser as their parents/grandparents. Indeed, According to Victor Preisser, co-founder of the Institute for Preparing Heirs.8

“Over 90% of heirs promptly change advisers when they receive their inheritances, and 70% of families lose control of their assets when an estate is transitioned to the next generation”

Action for advisers: Re-address client segmentation plans

This shift in assets is being seen by many advisers in their client banks. It can either be viewed as an opportunity to attract new clients and retain existing ones; or, it could be a risk if there is no strategy to capitalise on this trend.

The bottom line

At Russell Investments, we know that just around the corner, the Great Wealth Transfer will bring about great change. But it isn’t too late. As advisers prepare for client reviews, cash flow modelling can often be a timely and tedious task. Our efficient cash flow modelling tool is one of the few tools that can be used in under five minutes, enabling advisers to save a significant amount of time to prioritise and customise their client’s needs. Explore our range of exclusive adviser tools here.

1 Royal Bank of Canada, 2017; The Kings Court Trust, 2017; Accenture,

2016.

2 Kings Court trust, ‘Passing on the Pounds – The rise of the UK’s inheritance economy’. 2017, p. 3.

3 Resolution Foundation, Intergenerational Commission. ‘The Million dollar be-question’. 2017, p. 4.

4 The Office for National Statistics, ‘The UK national balance sheet: 2017 estimates’. 2017.

5 Office for Budget Responsibility, November 2017, p.120.

6 Kings Court trust, ‘Passing on the Pounds – The rise of the UK’s inheritance economy’. 2017, p. 10.

7 Royal Bank of Canada, ‘Wealth Transfer Report 2017’. 2017, p. 3.

8 http://www.wealthmanagement.com/data-amp-tools/retaining-heirs-wealthy-clients