Old vs New? Building a modern advice business.

The COVID-19 pandemic has had wide reaching impacts on our communities and our economy. Whilst our experience in Australia has been favourable compared to many other countries – it has still left an impact on individuals, including their sense of financial security.

Recent research by the Financial Planning Association (FPA) found that 6 months into the COVID-19 pandemic, less than half of Australians feel that they were in control of their financial position. The top three drivers of financial concerns included depletion of savings, job security and erosion of super1.

As a result of the pandemic and structural shifts in the industry, many advisers recognise an opportunity. Core Data reported that over 40% of adviser anticipate that demand for financial advice will increase going forward2.

However, while you may be thinking 'How do I to capitalise on this opportunity?’, you will need to consider how to balance this with your current operations and challenges such as the costs to service a client, compliance obligations and education requirements.

We believe it requires optimism about the future. Having a clear strategy, laser like focus on what you can control and actions you can take and working with the right team to help you get there.

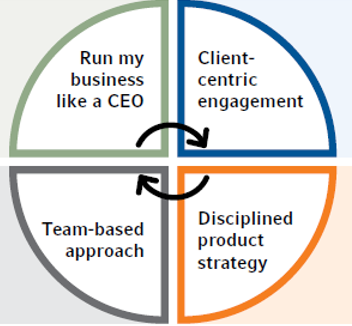

As we work with advice business leaders across Australia and around the world, we believe there four key drivers of potential future success:

- Running your business like a CEO,

- Client-centric engagement,

- Disciplined product strategy, and

- Team-based approach.

Four key drivers of potential future success

Think like a CEO

Advisers who adopt a CEO mindset have the ability to simultaneously focus on growth while also being realistic about the current market opportunities and challenges. To help manage this, they develop a strategic plan that defines their proposition to a clearly defined target market and a branding, marketing and client acquisition strategy to drive growth. They are also intentional in how they allocate their resources and time with an eye to maximising growth potential and seeking to manage risk, as well as continuously build their own competency, skill set and areas of expertise. And that’s just the beginning.

We believe great CEOs anticipate challenges before they happen. That means having a plan for market related events vs reacting to them when they occur.

Client-centric engagement

A second key driver for future success for an advice business is having client-centric engagement. It focuses on delivering the best possible experience for clients—and ensuring you know them well enough to be able to confidently and truly act in their best interest. Client centricity is how great advisers get to the top of their profession and stay there.

After all, this business is about helping people. Building your business around core client propositions should include:

- A clear understanding of your ideal client and anticipating their needs

- Articulating, and tangibly demonstrating your value to clients

- Using discovery and rediscovery of clients to ensure alignment between their goals and their plan and portfolio

- Delivering a systematised yet personalised client review process.

Disciplined product strategy

We often are asked by advisers ‘How do I balance my time between seeking new growth opportunities and maintaining existing client arrangements? We would suggest conducting a Time and Capacity analysis – which identifies where are you spending your time. Is your time spent delivering value to your clients or in your business?

For example, building or using a paper-based model portfolio may make an adviser feel like they are delivering something unique to a client. But does the client understand, let alone value the time spent on portfolio research and monitoring, implementation and reporting? Would they prefer more personal engagement, a deeper understanding of their changing needs or even other services to improve their financial security?

Sometimes an adviser is unable to name some of products used in their business and with clients. Let’s think through these implications:

- If annual due diligence (at least!) is undertaken on each of these products, calculate the number of hours required to maintaining this inventory.

- If regular due diligence is not undertaken, consider what level of risk you are exposing your clients and your business to?

Evaluate where you clients’ assets are invested. We have seen examples of businesses with a fraction of client assets spread across a long list of investment products. Often a number of products were used for only a single client. Consider the inefficiency—and also the risk—inherent in these imbalances in the products your clients may hold.

Other advisers may have an in-house model portfolio that they use, as a guide across their clients. While the intention is to build consistency, consider the potential risk of clients having different portfolios because of portfolio or rebalancing drift, timing changes of portfolio changes, effective communication, and documentation of these changes. Be mindful of any potential conflicts that may arise.

We have worked with financial advisers to use Managed Accounts to reduce the number of products requiring due diligence while, simplifying the investment governance required and increasing the level of discipline. This ensures that all clients’ portfolios are managed equitably and fairly while reducing the due diligence and oversight obligations. Having a disciplined product strategy can provide operational leverage, giving back valuable time to spend with existing clients and prospects.

Team-based approach

An essential element of delivering financial advice is the ability to build scale in your process. While technology is improving scalability to a certain extent, the ability to have an aligned, high performing team can build quality and scalable efficiencies across multiple parts of your business.

Building a high performing team includes the ability to attract and retain talent, provide role clarity and individual accountability in a positive and supportive culture.

A focus on alignment allows every team member to play a role not only in the client experience they deliver on, but how that translates in the eyes of your licensee or ASIC. Strong team dynamics and role clarity also show up for clients very authentically. It means every interaction with them feels intentional and customised for their goals, circumstances, and preferences. It reminds them that you are there not only recommending portfolios and products, but you are also their behavioural coach, guarding them from the very real human emotions that can jeopardise the health of the wealth. For your licensee or ASIC, it shows you have a workflow and a process in place as a team to address client concerns and needs.

The bottom line

Advisers who see now as an opportunity to assess the health and growth potential of their business by voluntarily and whole-heartedly delving into the hard questions are likely to set themselves apart in the future.

We believe that we are facing a new dawn for advisers, with a unique opportunity to move on from the past and develop a roadmap for future growth and success. Reach out to your Russell Investments regional team to discuss resources available to help you set your strategy, goals and action plans – we can help guide and be your accountability coach It’s how we’ve partnered with some of the most successful advisers for the past 20 years. That’s simply how passionate we are about helping advisers build and grow their business.

1 Money & Life Tracker – COVID edition Oct 2020

2 CoreData industry insights video for 2020