5 key ways advisers deliver value in the face of 2020's adversities

We believe advisers have never been more valuable than they are right now, in the midst of these challenging times.

Request your copy of the 2020 Value of an Adviser Report

For the past three years, we’ve created an annual report that holistically analyses the real value advisers deliver to their clients in their portfolios, in vital services advisers provide, and, right now in particular, in helping investors avoid behavioural mistakes.

This year, when a flock of black-swan events have flown overhead, the vital role advisers play should be more obviously valuable than ever. Volatility is back with a vengeance.

Economic hardships are piling up. And fight-or-flight tendencies are causing some investors to follow the herd into costly mistakes.

Dedicated advisers are not walking away from these challenges. Instead, we see many of them wading into the fray and working hard to keep their clients’ life savings intact. And as the volatility batters many investors’ savings, advisers may be challenged to articulate that the value they deliver goes over and beyond selecting and managing investments. That’s why it’s so important to provide a simple, easy-to-follow equation that shows the full value of an adviser’s services. It’s as easy as ABC, and then some:

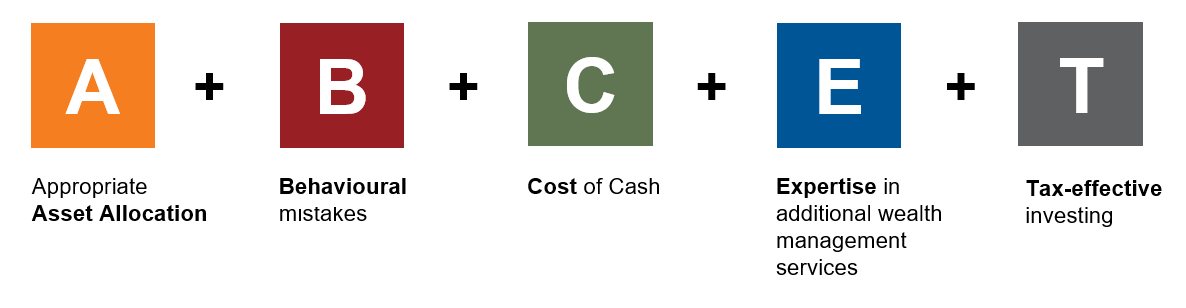

Value of an Adviser = A + B + C + E + T

A is for Appropriate Asset Allocation

It can be tempting for investors to build their own portfolios, but there are also risks. Investors could be making a fatal flaw in their portfolio design when it comes to setting an appropriate asset allocation to meet their investment objectives. Investors may not set the right investment strategy for their needs and they may lack the skills and/or time to research the many investment options available. There is also the added temptation to chase performance and over-react to market events.

In our recent research1, we surveyed over 3000 non-advised superannuation members. We found that 67% of these members didn’t know how their funds were invested or they relied upon the default option. Ultimately investing based on an asset allocation that has no reference to their personal circumstances.

The role of an adviser is to help their clients’ articulate life goals, translate this into investment objectives and design the best possible investment strategy and portfolio recommendations within a level of risk that is appropriate for the client. Helping the client understand the level of risk required and the implications of this risk is a critical ingredient in an advice conversation. Not taking sufficient risk can impact whether a goal is potentially achievable or not.

What is clear from our analysis is that financial advisers have the potential to add significant additional value to an investor’s portfolio over the long term by helping clients to work through their values, preferences and motivations from the outset. For investors who elect to proceed without advice, there can be a big price to pay for selecting the wrong asset allocation.

B is for Behavioural mistakes

Behavioural mistakes cost real money. We believe they are causing many investors to suffer significant long-term losses right now. This year in particular, we believe behaviour coaching is one of the most vital parts of the adviser job description. And when it comes to delivering value, avoiding behavioural mistakes may be the most significant contributor to total value.

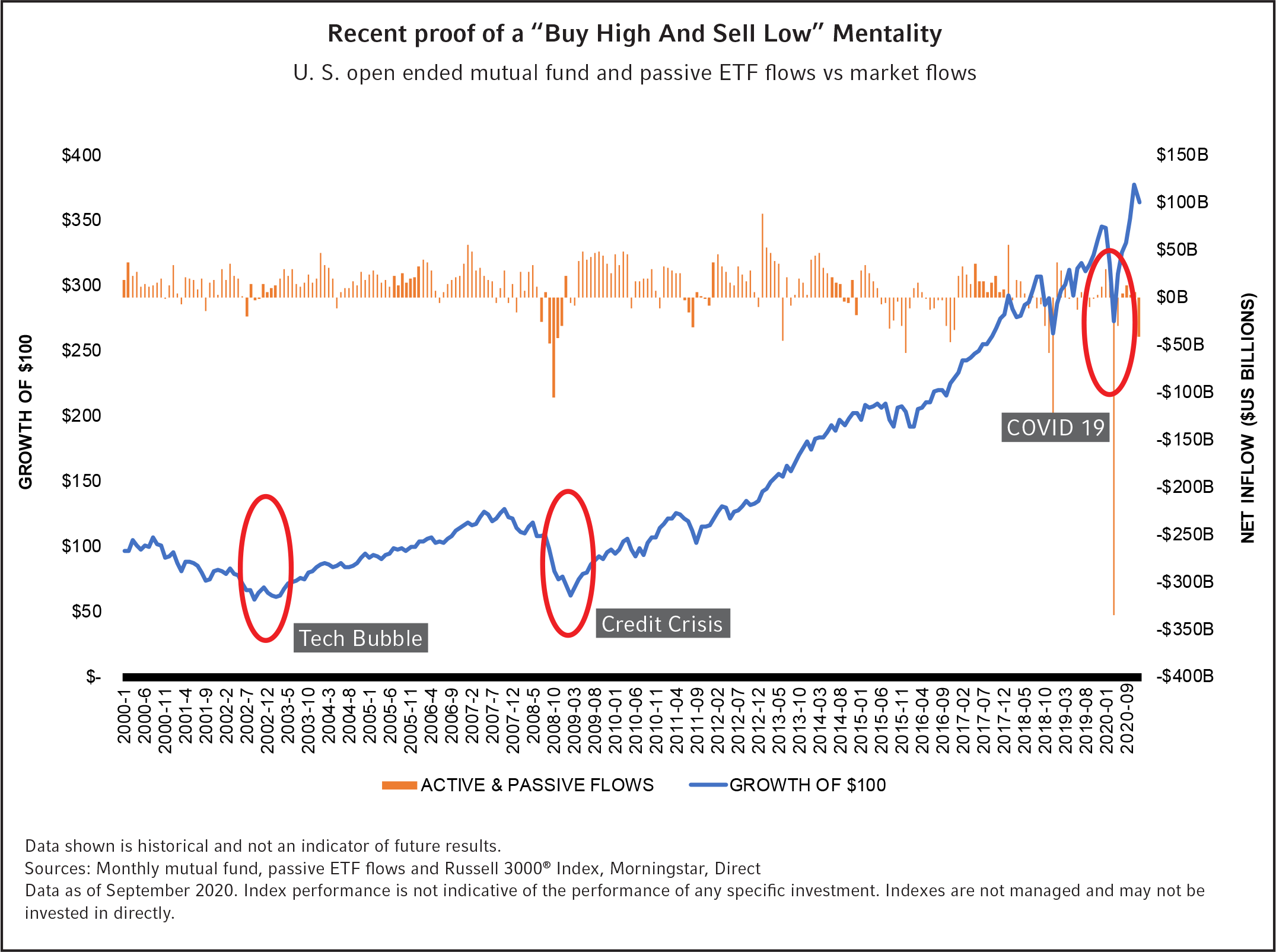

You’ve likely heard many comparisons between the current markets and the Global Financial Crisis in 2008-09, so keep this fact in mind: From January 2000 to September 2020, $100 constantly invested in the Russell 3000® Index more than tripled in value. And those who chose to stay in cash during that period missed a cumulative return of nearly 250%, based on the Russell 3000® Index. Left to their own devices, many investors buy high and sell low. Helping your clients avoid pulling out of markets at the wrong time and sticking to their long-term plan is one way that advisers provide substantial value.

C is for cost of cash

An investor’s attitude to cash can often be an interesting insight not only in their investment preferences but also their investing confidence. For many, cash can provide a sense of security and familiarity. It largely behaves as we expect it to, it doesn’t surprise investors on the upside, but more importantly it doesn’t surprise investors on the downside.

However, there can be a cost to holding too much cash – known by portfolio managers as cash drag. Portfolio Managers are very careful with the amount of cash they hold in a portfolio. While it can cushion potential portfolio losses, it can limit the overall performance and investors could miss out on potential portfolio growth. Sacrificing that portfolio growth today, could mean less assets in the future and therefore less spending power over the longer term, particularly in retirement. Advisers can assist clients in investing in a well-diversified portfolio that seeks to balance the needs of liquidity and targeting growth within the risk levels appropriate to the client.

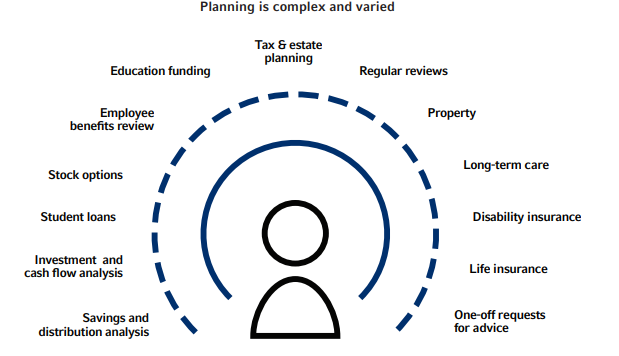

E is for Expertise in additional wealth management services

By this point in 2020’s volatile markets, you’ve probably heard a financial expert say how important it is to stick to your long-term investment strategy. The sound financial planning that advisers provide is designed for times just like this. And we believe it has never been more valuable.

As obvious as this sounds, it’s worth stating that financial advisers add value by doing the hard work of shepherding a strategy from origination to outcome, through all kinds of market events—even global pandemics. Are your clients aware of that value? They should be.

And what about the additional wealth management services you and your team offer? We believe advisers and their staff consistently underestimate the value of these services—insurance needs, custom requests and questions—they may provide their clients. These additional services can quickly consume 20, 50 or 100 hours each year. Make sure your clients consider what those professional hours are worth.

T is for Tax Effective Investing

Tax is often considered the realm of the accounting profession. However, an adviser can also provide expertise on managing and optimising investment tax for their clients. The concept of investment tax isn’t just limited to what goes into your tax return. Investment tax can have an impact on the asset value or portfolio return, even though it may not always be seen. As a result, it can be difficult for retail investors to know how to be tax effective in their portfolios. By lowering the tax on a clients’ investments you may help them reach their financial goals sooner. Adviser play an important role in this tax journey for their clients’, helping them navigate key components when it comes to tax-efficient strategies.

Advisers can assist in the management and optimisation of investment tax in a number of ways, including structural tax strategies, managing client driven trading, and portfolio recommendations that are trading and tax aware for clients.

The bottom Line

Market volatility, economic downturns and uncertainty make today’s investing environment one of the most challenging of our lifetimes. At Russell Investments, we believe the role advisers play has never been more vital. When else have investors had a greater need of a counsellor and guide to help them navigate these issues? This annual Value of an Adviser Report quantifies that dedication and the resulting benefit.

Advisers, we believe in your value. We see the advantages you create for your clients. We know the commitment you bring to your relationships. So stand tall. You’ve never mattered more.

To learn more about the 2020 Value of an Adviser Report click here.

1 Russell Investments – Member research 2020