5 key takeaways from RBA's pause on rate hikes

Yesterday, the Reserve Bank of Australia (RBA) left interest rates on hold at 3.6%. This comes after 10 months of consecutive interest rate increases. Economic growth continues to moderate in Australia, with consumer spending in February running at just over 2% on an annualised basis. The labour market, which has been a major focus for the RBA, is slowing and the forward-looking indicators for both supply and demand suggest that more easing in the unemployment rate is coming through the rest of this year. We believe we’ve seen the peak in interest rates in Australia, with the economy expected to slow further. The key risk to this view is a further pick up in wages growth, which we are closely monitoring.

1. Less need for further rate hikes

Monetary policy statements are very carefully parsed by economist and market watchers. Given this, small changes to the statement can be heavily scrutinised and analysed – which means that the Board are very mindful of the exact wording. There were some notable shifts in this month’s statement. When discussing the outlook for the cash rate, the RBA now expect that ‘some further tightening may well be needed’. This is a softer stance than last month, on both the likelihood of needing to raise rates more and the magnitude of the increase.

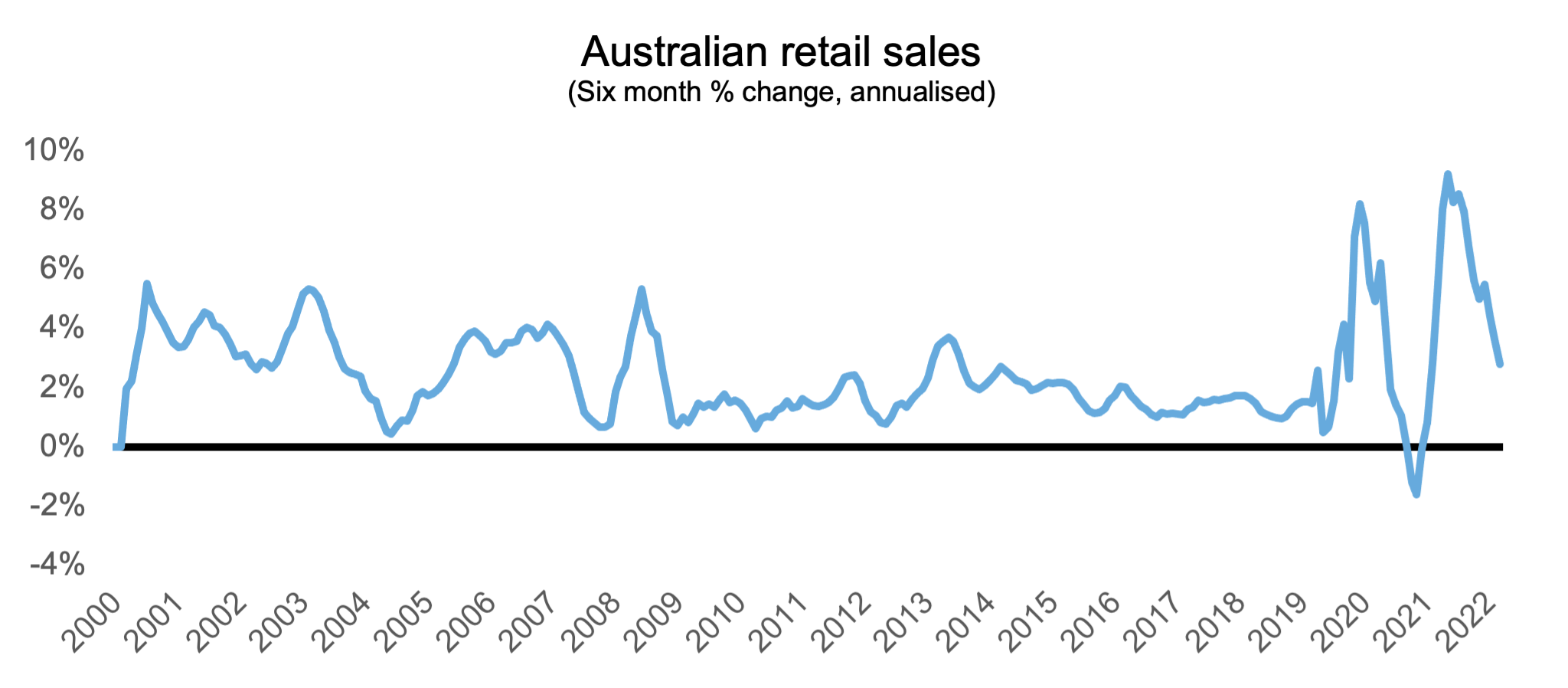

2. Consumer spending is softening

Retail sales in March came in close to consensus expectations but have notably slowed now as shown in the chart below. We have also seen anecdotes from Australian retailers about households tightening their belts, including Metcash (the owner of IGA) highlighting that consumers were moving to cheaper private-label goods and moving from fresh food to frozen.

Source: Australian Bureau of Statistics, 28 March 2023

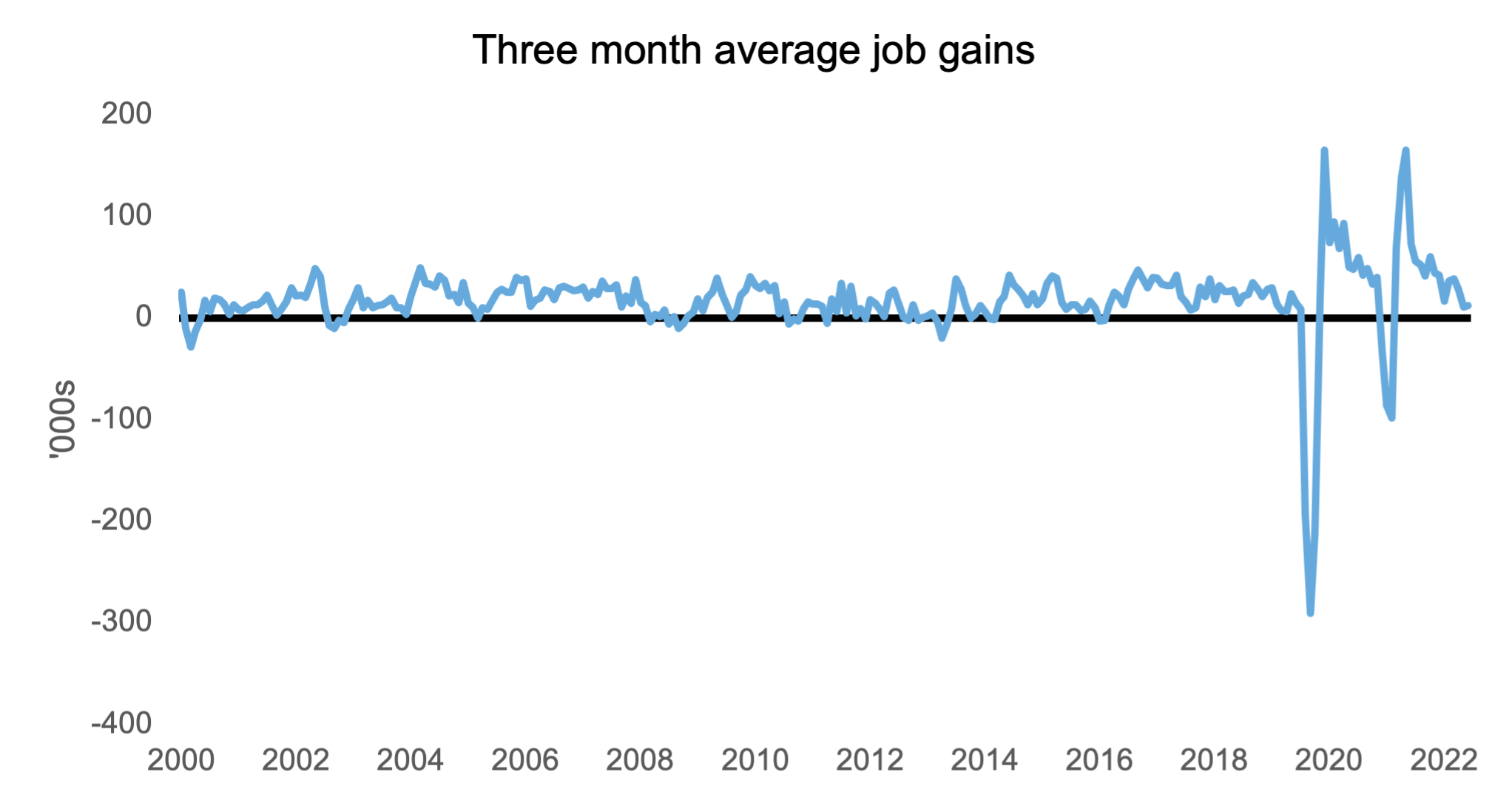

3. The labour market is cooling

After two months of negative jobs prints, Australia added close to 65K jobs in the month of February. Nevertheless, the 3 month average job gains has slowed dramatically. Forward looking indicators of labour demand continue to cool, while immigration continues to increase. This should put upward pressure on the unemployment rate and ease some pressure on wage growth. We are closely watching developments with the Fair Work Australia’s discussions around the minimum wage increase and the potential for a ruling for awards broader than the minimum wage.

Source: Refinitiv Datastream, 16th March 2023

4. Fixed rate mortgage roll-offs are starting to ramp up

April marks the beginning of a period in which a significant amount of fixed rate mortgages will roll off, significantly increasing mortgage payments for those households affected. Many households have built up significant buffers, however the RBA noted in its statement that some households are already feeling pain in their household finances. This dynamic is set to increase, as these mortgages reset and should keep the RBA on a cautious footing going ahead.

5. Recession risk is still relatively low in Australia, and Australian assets look more attractive than international

Whilst we expect the economy to slow, and there are risks of a sharper slowdown if households prove less resilient to the increase in mortgage payments, we believe that recession risk in Australia remains contained compared to other parts of the world. The RBA have brought interest rates into restrictive territory (i.e. to a level that is going to slow the economy), but they are not as restrictive as many other countries. Additionally, the return of immigration and tourism are a positive. We believe Australian equities look reasonably valued compared to global equities and maintain our belief that Australian fixed income offers attractive valuations.