Fixed Income Survey 2024-2025: Cautious optimism

Executive summary:

- Global rates caution: Rate cuts are widely expected, with the U.S. Fed and ECB both projected to lower rates significantly by 2025 amid concerns over potential recession or stagflation.

- Debt preferences: Managers are cautiously optimistic on Global Credit, favoring European credit over the U.S.; managers' expectations are for stability or slight tightening in Euro spreads vs potential widening in the U.S.

- Global Leveraged Credit: High-yield managers lean defensive amid economic uncertainties, expecting spreads to remain within a stable band; with a small subset expecting widening of spreads between 50-100 bps. Default rates are expected to stay reasonably contained inside of 5%.

- In Emerging Markets, Local Currency Debt stands out as attractive due to the relative cheapness of EM rates and the expectation of FX strengthening in EM. Managers expect EM Hard Currency performance to be driven by the policy rate in the U.S., while supported by inflows into the asset class.

- Municipal and Securitized strengths: Municipal bond spreads are expected to remain stable, with a moderate bias towards modest tightening, driven by solid fundamentals and demand outpacing supply, with high yield municipals projected to outperform corporate high yield. In Securitized credit, agency MBS garners broad support, while CMBS shows mixed appeal due to fundamental risks but offers compelling valuations.

- Currency outlook: The USD is expected to depreciate against major currencies like the EUR and GBP, while JPY is viewed as a strong performer. In EM currencies, the Brazilian Real is seen as the currency with the greatest value, with managers expressing bearish views on the CZK and the MXN

Global rates

- U.S. rate cuts of up to 200bps are anticipated by the end of 2025 but with significant further downside if recession risks materialize. U.S. yields are also expected to fall although to a lesser extent, resulting in a bull-steepening of the U.S. yield curve, while ECB cuts could drive significant Bund yield declines, leading to wider core-periphery spreads in Europe.

Economic concerns: Managers express long-term concerns over risks of global economic stagnation and mild recession, with inflation potentially leading to stagflation. Nearly half also see potential for significant repricing of risk assets, while political risks, such as new Trump presidency and geopolitical conflicts, have been seen as lesser threats.

Fed rate projections: As a result of the economic outlook, investors expect the U.S. Fed Fund rate to be cut by at least 150bps by the end of 2025 despite expectations for inflation to remain well above the 2% target. Most respondents expect U.S. inflation to average between 2-2.5% in 2025 and to remain above target over the long run. A significant share of respondents believe U.S. consumer prices could rise even faster at a pace of up to 3% next year. Risks for a steeper decline in rates are seen as significant, with the majority looking for an overall 200bps of cumulative rate cuts which could bring the Fed Funds rate to 3% by the end of Q3 2025, matching their estimates for the long-term equilibrium nominal R* rate. The room for rate cuts is considered as significantly larger in the case of a recession, with most respondents expecting the Fed Funds rate to be cut to as low as 1% in such an event, with estimates ranging between 0.5-1.5%.

Yield expectations: Managers largely expect the U.S. curve to continue to bull-steepen, with term premia seen as continuing to increase although at a relatively slow pace, with the majority expecting for the U.S. 10y-2y spread to rise to 50bps by the end of next year, but unlikely to exceed 100bps. U.S. 10y yields are expected to be trading between 3.25% and 3.75% at the end of 2025 although with substantial upside risks to as high as 4.50% due to potential challenges to U.S. fiscal and debt sustainability as well as international trade and the Fed's independence in the aftermath of the U.S. presidential vote. Nevertheless, no major impact on market volatility is foreseen for 2025 but duration positioning remains cautious and largely neutral despite a bias for being moderately overweight duration as most investors see room for further declines in yields from their current levels.

European rates: Investors seem to have a more bullish view with regard to European rates, with most respondents expecting the ECB to cut its official rates by between 150bps to 200bps, likely resulting in a significant decline in 10yrs Bund yields which are seen falling below 2.25% by the end of 2025. A significant portion of the managers even expect them to fall as low as 1.50%, leading to some core-periphery spread widening.

(Click image to enlarge)

Source: Russell Investments. As of 10/31/2024

Global credit

- Managers hold mixed views on Global Credit spreads, with expectations for broad stability. In the U.S., managers see stability of spreads, with a subset expecting moderate widening. In Europe, divided views between stability and moderate tightening. Europe is also seen as the most attractive region. Potential risks for Global Credit include deteriorating fundamentals if a hard landing of the U.S. economy were to materialize.

Mixed views on global credit: Almost 50% of managers expect Global Credit spreads to remain within a narrow range (+/-10 bps). In the U.S., 38% anticipate moderate widening of spreads (10-30 bps), while 46% expect range bound spreads. Managers are slightly more optimistic in Europe, with 38% expecting moderate tightening (10-30 bps compression); however, 29% of managers expect to see some moderate widening in the year ahead. Only 25% of managers expect spreads in Europe to range bound.

12-month spread forecasts: The average expected spread level in 12 months is 94 bps for the U.S. and 110 bps for Europe. Managers are rather cautious, with 50% believing that current spreads only compensate "to some degree" for potential risks of deteriorating fundamentals, while about 38% think they "do not compensate" for potential risk of deteriorating fundamentals.

Sentiment and regional preferences: Reflecting their conservative outlook, 54% of managers expect corporate earnings to broadly align with market expectations in the year ahead. Nearly 70% of managers expect leverage of both U.S. and European companies to remain stable. From a return perspective, Europe is seen as the most attractive region, followed by the U.S. and the UK. In investment-grade (IG) sectors, Senior Financials are expected to perform best, followed by utilities, loss absorbing senior financials and subordinated financials. Conversely, cyclicals are expected to deliver the worst performance for the year ahead.

Asset class expectations: Managers expect IG Credit to deliver the best performance (over UST) in the year ahead, followed by non-agency MBS and High Yield. Cash is expected to deliver the worst performance. Despite conservative views, a subset of managers still maintain a relatively bullish market positioning, with 30% of them reporting a 1.05-1.15x beta overweight (OW) positioning while c.50% reported a risk positioning between 0.95-1.05x beta.

Political concerns: Managers seem little worried about the potential impact of a new Trump presidency, with concerns centered on a possible U.S. economic downturn, escalation of geopolitical risks, and a worsening fiscal deficit.

(Click image to enlarge)

Source: Russell Investments. As of 10/31/2024

Global leveraged credit

- A defensive stance prevails with stable spreads expected, though some anticipate widening due to economic concerns. Sector vulnerabilities are notable in Telecommunications and Automotive, with a total return outlook of 5–7% for the year ahead.

Market outlook and positioning: High-yield credit managers are adopting a cautious stance due to economic uncertainties, with many defensively positioning portfolios. While most expect spreads to remain within a stable band, some foresee moderate widening (50–100 bps), reflecting concerns over potential economic slowdown or increased credit risk, combined with the limited credit risk premia available.

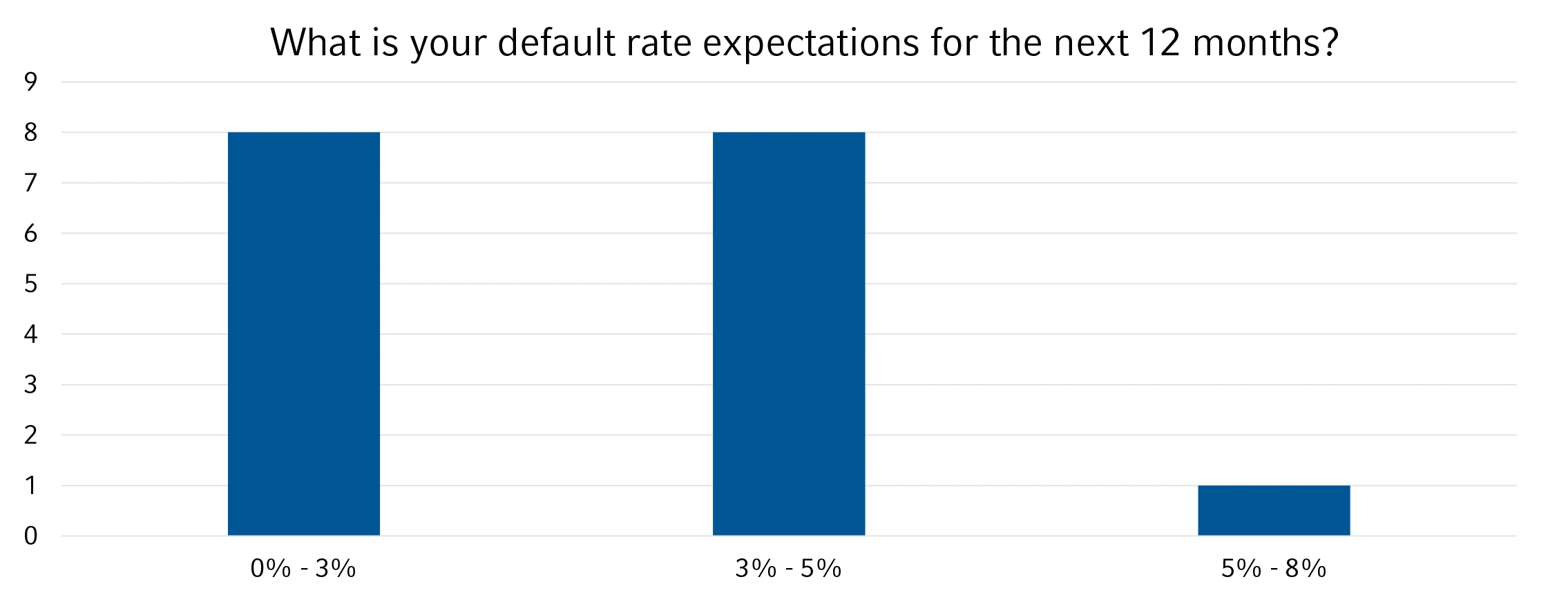

Credit fundamentals: Opinions are mixed on credit fundamentals, with many managers expecting stability due to moderate growth and solid corporate balance sheets. However, some managers predict a mixed environment with both improvement and deterioration across different segments, depending on factors like sector resilience, debt levels, and macroeconomic pressures. Default rates are expected to stay reasonably contained inside of 5%, over the next 12 months. This forecast is grounded in a broader expectation of economic resilience and that defaults will be manageable.

Regional insights: There is no broad consensus on specific opportunities within the global corporate credit landscape, indicating a lack of strong conviction on which asset class holds the best value. That said, U.S. credit markets are generally favored over those in Europe or emerging markets, likely due to the perceived stability and stronger relative economic fundamentals. Within the U.S. market, the B-rated segment is identified as offering the most relative value.

Sector insights: Sector-wise, Telecommunications and Automotive have emerged as the most concerning segments. The Telecom sector faces structural challenges from high capital expenditures, regulatory pressures, and technology shifts, while the Automotive sector is grappling with supply chain constraints, rising input costs, and the financial implications of transitioning to electric vehicles.

Return expectations: Managers project 5–7% returns over the next year, primarily from coupons, indicating limited potential for capital gains and suggesting a stable but challenging environment focused on income-driven returns.

(Click image to enlarge)

Source: Russell Investments. As of 10/31/2024

EM Local Currency

- For the year ahead, EM Local Currency Debt (both sovereign and corporate) is seen as more attractive than Hard Currency due to relative cheapness of local rates and the potential for FX strengthening, particularly in Latin America. Managers anticipate returns of 6–9% for the EM LC index in the year ahead while inflation risks are perceived as low.

Preference for local currency: When comparing sub-sectors within EMD, most managers consider Local Currency EMD to be more attractive than Hard Currency (Sovereign and Corporate) over the next 12- and 36-month horizon. This is supported by their views that EM local rates are relatively cheap and expect a moderate strengthening of EM FX

Regional and currency preferences: Managers prefer Latin American currencies (over the currencies in Asia and Eastern Europe), particularly the Brazilian real (BRL), which is seen as attractive (net of carry), followed by the Turkish lira (TRY), which offers a substantial carry of over 50%. The recent rate hike in Brazil has further increased its real rate advantage over peers.

Projected returns: Managers expect the Local Currency EMD index to yield a total return of 6% to 9% over the next 12 months. The majority of managers see lower inflation across EM countries which led them to forecast larger potential Total Return and contribution from local rates than FX in the next 12 months

Risks: The strongest perceived risk to Local EMD bonds is a strengthening of the USD, followed by U.S. election outcomes, rising U.S. Treasury rates, and geopolitical risks. Secondary risks include trade tensions, global inflation, and a potential U.S. recession. Most managers don't expect any countries to impose capital controls, though a few see a small chance in Egypt, China, and Turkey.

EM Hard Currency

- There is an overall positive outlook together with attractive yields (~7.5% index yield). Top country preferences vary, with off-index overweight in EM corporates and caution in China due to economic concerns as main themes.

Key drivers and yield: Most EMD managers view Fed policy and changes in U.S. Treasury rates as the primary drivers of EMD Hard Currency performance, which is expected to deliver mid-single-digit returns over the next 12 months, supported by inflows into the asset class which had suffered outflows in the past few years. However, some managers continue to forecast challenging inflows. The index is yielding about 7.5%, indicating that carry is a significant component of the total return expectation.

Spread outlook: Managers anticipate spreads to remain range-bound (attractive relative to the global high yield market) with some managers expecting some modest tightening, supported by relatively healthy EM growth and low sovereign default expectations. The moderately positive outlook for the asset class follows positive returns of the index, posting 8.6% YTD and 18.6% for the past 12-months.

Allocations and portfolio strategy: Top country overweights vary, with Mexico, Argentina, Egypt, India, Peru, and Ivory Coast expected to outperform, while China remains a concern due to ongoing uncertainty surrounding its economic growth. Managers expressed their preference to allocate over 15% of risk to EM corporates, often as a proxy for sovereign exposure, whereas local currency bonds and currency allocations are small.

Securitized

- Managers generally maintain risk exposure in structured credit, particularly favoring Agency MBS due to cheap spreads; CMBS offers attractive valuations but carries fundamental risks, with mixed interest in higher-quality tranches or Single-Asset Single-Borrower (SASB) deals.

Risk appetite and positioning: At a high level, securitized credit specialist managers remain comfortable taking risk in structured credit assets, with approximately 87% of responses either maintaining their existing positions or adding to existing risk levels. Only two managers expressed that they would be reducing risk exposures in structured credit over the next 12 months

Sub-sector preferences: The manager specific preferences for sub-sectors were quite balanced, although BBB CLOs, Esoteric ABS, and housing related credit (legacy non-agency and credit risk transfer RMBS) appeared to be the favored segments based on manager rankings.

Agency and non-agency MBS outlook: The agency MBS sector drew unanimous support as every manager response suggested that they either already have a long mortgage basis position (long agency MBS vs Treasury) or will be initiating a position going forward - with the overwhelming majority already positioned in favor of agency MBS. Agency MBS spreads have remained cheap amidst a changing technical dynamic due to the Fed's wind down of its quantitative easing program. The non-agency RMBS segment appeared to be near consensus, with all but two respondents either comfortable that loss-adjusted yields and spreads will either show some degree of tightening or trade within a range-bound environment.

CMBS insights and challenges: CMBS continues to be the most topical segment as the sector offers by the far the most attractive valuations with widespread levels, but commensurate fundamental challenges as commercial real estate sectors like office, retail, lodging, and even multi-family have shown signs of stress and increasing delinquencies. Managers were split in their desire to take risk with about half of respondents taking no positions, while the other half were keen on valuations, but mostly in the higher quality tranches. Two managers recommend actively taking risk where they can conduct deep dive underwriting on more mezzanine type CMBS risk. The preferred habitat for CMBS risk-takers tilted in favor of SASB CMBS where it is typically considered easier to underwrite the collateral with accuracy compared to conduit CMBS or CRE CLOs. Still, five managers preferred conduit where the attractive valuations can make for ripe return potential for those specialists willing to do the deep dive credit work.

(Click image to enlarge)

Source: Russell Investments. As of 10/31/2024

Municipals

- Managers expect municipal spreads to remain stable, with a subset of managers expecting spread tightening as demand outweighs supply. Default rates are projected low, and municipal high yield is expected to outperform corporate high yield, buoyed by strong fundamentals.

Market sentiment: There is optimism among municipal fixed income managers, with 83% expecting municipal bond spreads to tighten modestly over the next 12 months. Nearly all managers anticipate municipal high yield to outperform corporate high yield.

Valuation and demand: Managers expect the 30-year triple-A municipal/treasury ratio to range between 80%-90%, below its long-term average of over 90%. Managers expect demand for municipals to continue to outstrip supply, creating an ongoing attractiveness in the muni/treasury ratios which is even more pronounced at shorter tenors along the curve.

Solid fundamentals: All managers foresee strong fundamentals, with investment-grade municipal default rates expected to stay between 0-3%. In high yield municipals, 78% of the managers prefer the lowest range, selecting 0-3% defaults and the remaining managers (22%) expecting between 3-6%. Key concerns include Fed policy and potential tax or regulatory changes, while municipal creditworthiness is seen as improving.

Top picks and themes: Managers highlight a diverse range of best ideas, including Puerto Rico (particularly the PREPA bonds), airports (Miami-Dade, JFK, and AMT airports), transit names (Port Authority of NY/NJ), education themes (Texas Permanent School Fund was mentioned three times), small non-rated high yield deals, private and workforce housing deals, and energy/power related deals (MEAG).

Source: Russell Investments. As of 10/31/2024

Currency

- USD depreciation is expected against the EUR and GBP by 2025, with JPY seen as a strong performer. EM currencies, especially the Brazilian Real, could appreciate vs the USD, though low-yielding currencies like CHF remain favored for funding trades.

USD depreciation expectations: Most respondents expect USD to depreciate slightly vs the EUR and GBP by the end of 2025, with the EUR/USD FX settling between 1.10-1.15, although with significant risks of bottoming at or below 1.05. GBP/USD FX is expected to trade within 1.30-1.35.

Bullish on JPY: Manager views on JPY are generally bullish despite denoting a major split among investors. A large share of respondents expect the JPY to appreciate to 125-130 vs the USD while identical shares were looking for a stabilization within 150-160. No manager expects the pair to trade above 160. Most of the managers therefore expect the JPY to be the best performing currency by the end of next year with the CHF widely expected to be the worst performer.

EM outlook: A weaker USD is expected to contribute to moderate appreciation of EM currencies, particularly the Brazilian Real, which is viewed as the most valuable currency (including carry). Conversely, bearish sentiments exist towards the Czech Koruna, Mexican Peso, and Chinese Yuan, the latter of which is expected to experience an orderly devaluation.

Currency positioning: In general, active currency exposures tend to be positively correlated to riskier assets, suggesting that currency positions are aimed at seeking value rather than being used as risk diversifiers, for which investors favor long USD as well as long JPY positions. FX rates continue to be seen as being mostly driven by expected changes in interest rates differentials, with low yielding currencies such as the CHF therefore likely to continue to be used as funding currencies.

(Click image to enlarge)

Source: Russell Investments. As of 10/31/2024

The bottom line

Our 2024-2025 Fixed Income survey reveals how managers remain cautiously optimistic with most of them anticipating U.S. rate cuts of up to 200bps by the end of 2025, with a soft landing as a base case scenario. Nonetheless, managers also remain vigilant of potential downside risks if a hard landing were to materialize or if inflation were to reaccelerate. Most managers have been positioned for a bull-steepening of the U.S. yield curve, and it'll be certainly interesting to see how managers reassess Term Premia and the potential implications for the U.S. deficit in the face of the new Trump's presidency. Sentiment in Europe remains mixed with managers expecting the ECB to cut rates by 150-200bps, likely leading to significant declines in Bund yields, but with wider core-periphery spreads

Managers' sentiment for Global Credit is rather mixed, with expectations for broad stability in the U.S. and moderate tightening in Europe. This indicates cautious optimism, with concerns over economic fundamentals and potential risks of a hard landing in the U.S.

In EM, Local Currency is seen as more attractive than Hard Currency due to the relative cheapness of local rates and the potential FX strengthening, particularly in Latin America. This preference highlights the search for higher yields and diversification benefits in EM assets. The sentiment is generally positive towards EM debt, with managers seeing opportunities for higher returns.

Managers seem to favor Agency MBS due to the relative cheapness in spreads and expect municipal spreads to tighten modestly. This suggests a preference for safer, income-generating assets amidst economic uncertainties. The sentiment here is conservative, with a focus on stability and income generation.

The sentiment in currencies reflects a mix of expectations and strategic positionings. There's a general expectation of depreciation of the USD against the EUR and GBP by 2025 while investors remain bullish on the JPY, despite differing views on its exact trajectory. A weaker USD is anticipated to boost EM currencies, especially the Brazilian Real, which remains as a favored currency. Low-yielding currencies like the CHF are expected to remain popular for funding trades due to their stability and low yields.

Overall, the sentiment captured by the Fixed Income survey seems to be of "cautious optimism." Managers are strategically positioning themselves to manage risks while seeking opportunities for growth and higher returns in various markets.