Do you have your seatbelt on?

Would you drive a car that didn’t have seatbelts?

We may snap our seatbelts in place when we get in our car, without thinking much of it. But I was reminded of their utility a few years ago. During one of my monthly Montreal, QC – Loretto, PA road trips in the middle of the night, fuelled by too much coffee and not enough sleep, a deer ran out right in front of my car. Thankfully, I avoided a potential catastrophe and slammed on my brakes in time. But in that moment, I was incredibly grateful for my seatbelt and airbags.

Similarly, with investment grade1 government bonds, we might not think much about the role they play in our portfolios. We may even wonder why we bother paying for them when they’re not contributing to portfolio growth during rising markets. But when markets inevitably take an unexpected turn, we are quickly reminded just how essential they are. The market turmoil surrounding COVID–19 is one of the most recent examples.

We went from bond yields2 hitting an all–time low in 2020 to new fears that market interest rates will return to normal levels amid a reopening economy. As bond yields rise, bond prices decline, affecting the performance of portfolios that hold bonds.

This journey has led me to have more and more conversations with advisors questioning the need to own government bonds in their client portfolios.

Do we really need investment grade government bonds? Are they still an integral part of portfolio construction? Just like seat belts belong in a car, we believe investment grade government bonds play a key role in a portfolio.

Investment grade bonds are the seatbelts in your portfolio

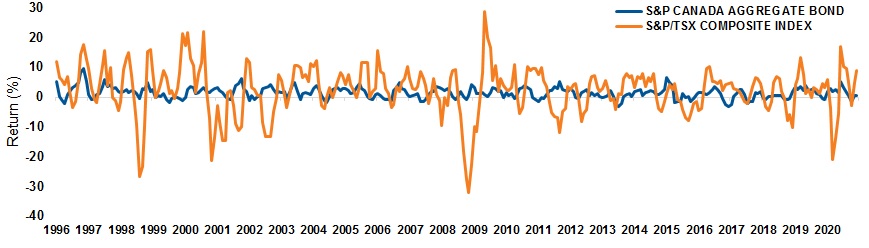

Investment grade government bonds offer diversification from equities because of their generally low correlation to equities, especially during market selloffs. As you can see in the chart below, core fixed income (represented by the S&P Canada Aggregate Bond Index) traditionally provides a much smoother ride than equities (represented by the S&P/TSX Composite Index).

Fixed Income and Equities Have Different patterns

Click image to enlarge

Source: Refinitiv DataStream, Morningstar Direct. As of December 31, 2020. Fixed Income is represented by S&P Canada Aggregate Bond Index, equities by S&P/TSX Composite Index. Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly.

Higher the potential rewards, higher the risk

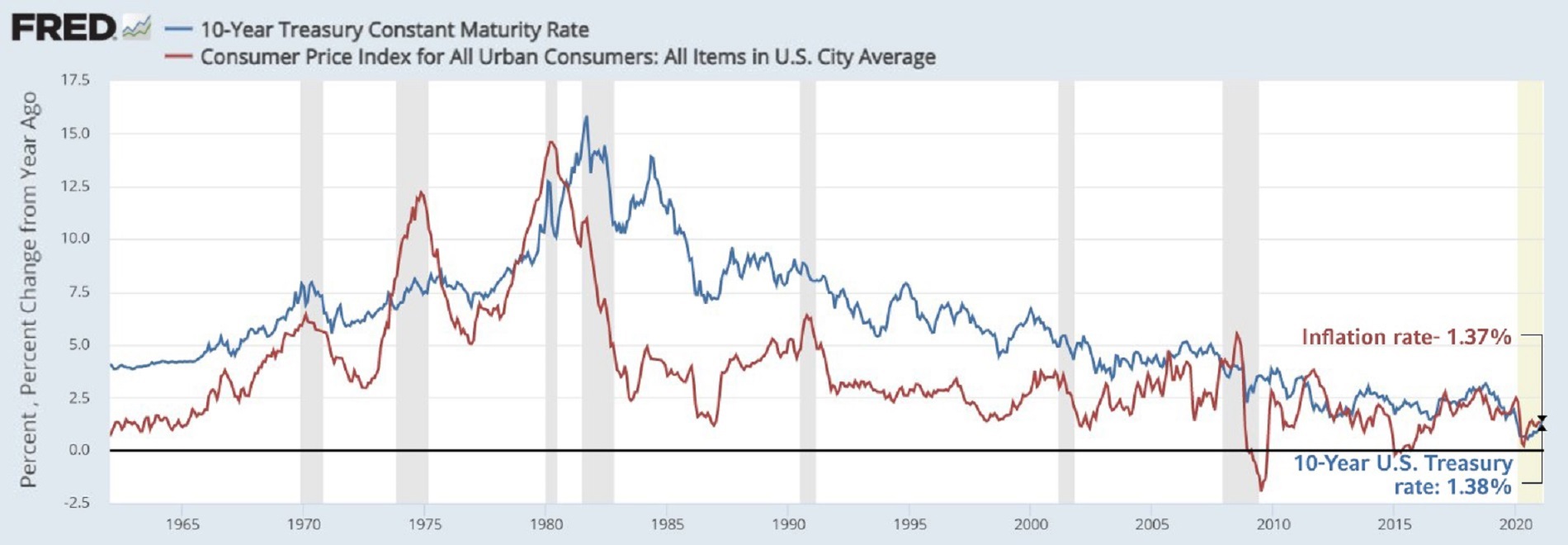

The first quarter of 2021 saw the 10–year U.S. Treasury bill interest rate trailing close to and at times below inflation (see chart below). To limit the potential erosion of purchasing power, diversification and active management in the bond space is now more important than ever before.

10-Year U.S. Treasury rate vs. inflation rate

Click image to enlarge

Source: Board of Governors of the Federal Reserve System (US), 10-Year Treasury Constant Maturity Rate [DGS10]; U.S. Bureau of Labor Statistics, Consumer Price Index for All Urban Consumers: All Items in U.S. City Average [CPIAUCSL]; retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org, February 24, 2021.

In the past, bonds played many roles in a portfolio: primarily, diversification, and the potential for capital preservation but they could also offer income. But when bond yields and interest rates started declining towards zero, investors had to find other solutions to bolster the income and performance of their portfolios. One way that advisors solved this issue was to allocate more of their fixed income exposure to corporate bonds and other higher yielding fixed income assets.

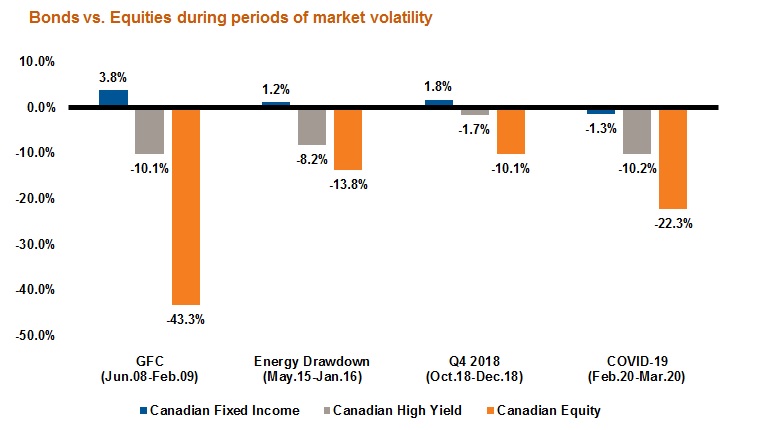

But with higher potential rewards come higher risks. As you can see in the chart below, core Canadian bonds can offer much needed diversification when compared to high yield bonds and equities during challenging market events.

Click image to enlarge

Source: Russell Investments. In CAD. Canadian Fixed Income: FTSE Canada Universe Bond Index; Canadian High Yield: FTSE Canada High Yield Bond Index; Canadian Equity: S&P/TSX Composite Index. Indexes are unmanaged and cannot be invested in directly. Past performance is not indicative of future results. GFC=Global Financial Crisis, Q4 2018 was worst quarterly loss since the GFC in 2008, on U.S.–China trade war, lower oil prices and rising interest rates.

Driving the portfolio for a smooth ride

Navigating market environments is becoming more challenging. Not only do we have to diversify across asset classes and geographies, we must now also look to diversify within asset classes to achieve our investment goals.

Depending on your goals, age, risk tolerance, and other factors, we believe that between 25–40% of your bond portfolio should be allocated to core government investment grade bonds. Other than cash, no other asset class has the potential to offer a hedge against equity market selloffs. Instead of focusing only on higher yielding, alternative bond solutions, complementing them with core government bonds can provide a smoother investment ride over longer periods of time.

The bottom line

Investment grade government bonds never seem essential, like seatbelts, until they are. If you wouldn’t buy a car without seatbelts, then you probably shouldn’t invest in a portfolio without considering investment grade government bonds.

Yields and returns might not be as attractive as they once were but remember: that was never the primary objective of the asset class. When it comes to capital preservation and diversification, these securities are unlikely to steer you in the wrong direction when it matters the most.

1 Investment grade is the highest rating given by agencies such as Standard & Poors and Fitch. The scales range from very low risk AAA to default D at the bottom. A bond with a rating of AAA to BBB–is considered investments grade.

2Yield is the income produced by an investment, such as interest or dividends. It is usually expressed as an annual percentage rate based on the investment’s cost or current market value.